China PV Market: An expected bounce but a still weak market

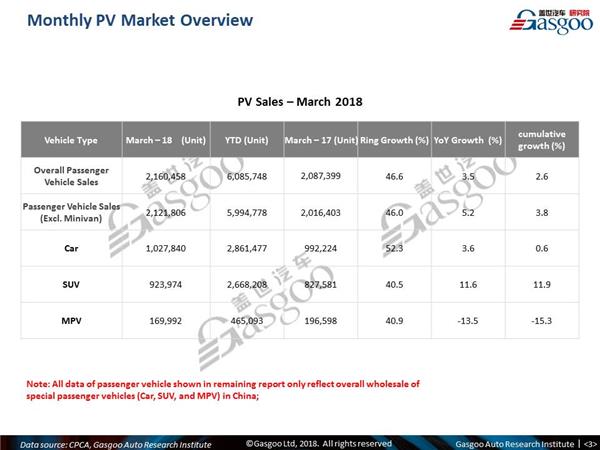

Shanghai (Gasgoo)- In March 2018, China’s Passenger Vehicle (PV) sales increased by 4.9% year-on-year (YoY) to 2.19 million units and 45.9% from 1.45 million in February. YTD PV sales increase to 5.99 mn units from 5.78 million of the same period last year.

The timing of the Chinese New Year holiday caused distortion that wholesale volume in February declined sharply, but the wholesale bounced as expected in the following month. Many people believe that it will be a better year than 2017 in which growth rate approached 2.5% in the end if they simply read the wholesale data of this Q1. However, the market is still destocking and the situation is still tough if we compare wholesale data with production and retail data. We foresee the process will last to April or even May.

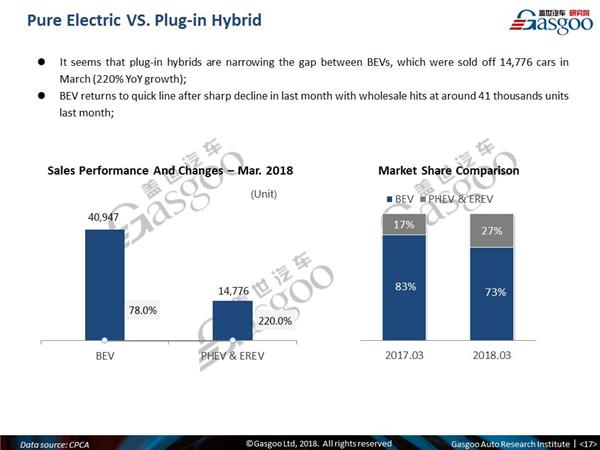

Different from the traditional PV segment, China’s New-Energy PV still keeps fast paces in both sales and production. In March, the wholesale of NEV (PV) reached more than 56 thousandunits, increasing by 102.1% YoY. The finalization of temporary subsidy policy may spur the OEMs to increase sales and production plans in next few months like Q4 of 2017. We are happy to see plug-in hybrids maintain strong momentum in sales and private acceptance, but PHEVs still cannot immediately shake the leader position of all electric cars in China market. On the other hand, A00 consolidates its market share in BEV sector from 54% in March 2017 to 68% in March 2018. It seems that the market is turning to usual pattern and will continue in a period of time.

On 10 April, President Xi sent out an exciting message to global auto industry that China will progressively eliminate the restrictions on local venture’s equity ratio of foreign automakers and is ready to appreciably cut tariffs on imported vehicles when he was giving a speech in Boao Forum for Asia (BFA). According to government’s timing plan, China will waive the restrictions on NEVs and special-use vehicles in this year, on commercial vehicles in 2020, and on traditional passenger vehicles in 2022. It is also seen as a gift to most global automakers who have been looking forward to it for many years. For China, the new policy is to attract extensive introductions and localizations of cutting-edge automotive technologies and manufacturing processes, especially in fields of C.A.S.E (connected, autonomous, shared, and electrified). For these foreign companies, the policy encourages them to bring more investments and engagements on R&D and manufacturing in a more fair environment. The essence of the restrictions is to result in a win-win mode. However, it still cannot totally remove worries of those foreign automakers because they are concerned about many problems, such as how to manage relationships with governments, how to prevent hostile overtakes of China giants, and if the government will set intangible limits in other processes.

We think that the open policy will furtherly spur the possibilities of cooperation that produce all-electric vehicles and will provide more choices for these global automakers when they select a new partner. The potential JV like SAIC-Audi and Great Wall-BMW will also be pushed in spotlight timely as the policy issue. However, we are not optimistic that those foreign giants will build relationships with startups because they are not powerful in eyes of global companies but it is a trend that some state-owned auto companies are getting much more involved in the businesses of these startups.

Tesla is another policy beneficiary that would be able to produce EV cars independently in China if Sino-US trade conflicts won’t be upgraded. But, at present, Elon Musk is more hoping that the tariffs cut can be taken into effect as soon as possible.

Divorce between current JV partners after 2022 seems not easy. A natural advantage of local partners is that they have dependable governmental backgrounds and can handle complicated government relationships. If the foreign companies recklessly shake off their current local friends, they will have to spend much more on managing governmental relationships and will meet intangible difficulties in situations. During the period of time (by 2022), we cannot ignore the ascent of power of Chinese auto companies. Local giants like SAIC, Changan, Geely, Greatwall, DFAC, BAIC, and GAC have advantages of capital, supply chains, and labor resources which allow them negotiate equally on the table. For those tiny local OEMs, we consider that they will transform themselves to be a role as manufacturer.

Although the government opens China market to global deeply, they are targeting to deepen cooperation through removal of restrictions on foreign equity ratio. It is undoubted that the new round of cooperation will push the development of EV sector to a higher level. The balance of game will partly restructure the PV market in the long run because some JV relationships have been unbreakable after decades.

To get full China PV market report, please click here.

Gasgoo not only offers timely news and profound insight about China auto industry, but also help with business connection and expansion for suppliers and purchasers via multiple channels and methods. Buyer service:buyer-support@gasgoo.comSeller Service:seller-support@gasgoo.com