According to data compiled by the Gasgoo Automotive Research Institute, in 2025, China's automotive industry is undergoing a critical shift from electrification to intelligence. From LiDAR, forward-facing cameras, and driving-dedicated ADAS to APA solution and HD maps, installation data across ADAS sub-segments reveal a clear industry landscape: China's local suppliers are rising strongly, top-tier companies are increasingly concentrated, autonomous control capabilities are steadily improving, while international giants face new challenges in technology iteration and ecosystem competition.

These data not only provide a direct view of market shares but also reflect the strong momentum of China's automotive industry in core technology localization, widespread adoption of high-end configurations, and the practical deployment of intelligent driving-assist scenarios, offering a valuable reference point for anticipating future industry trends.

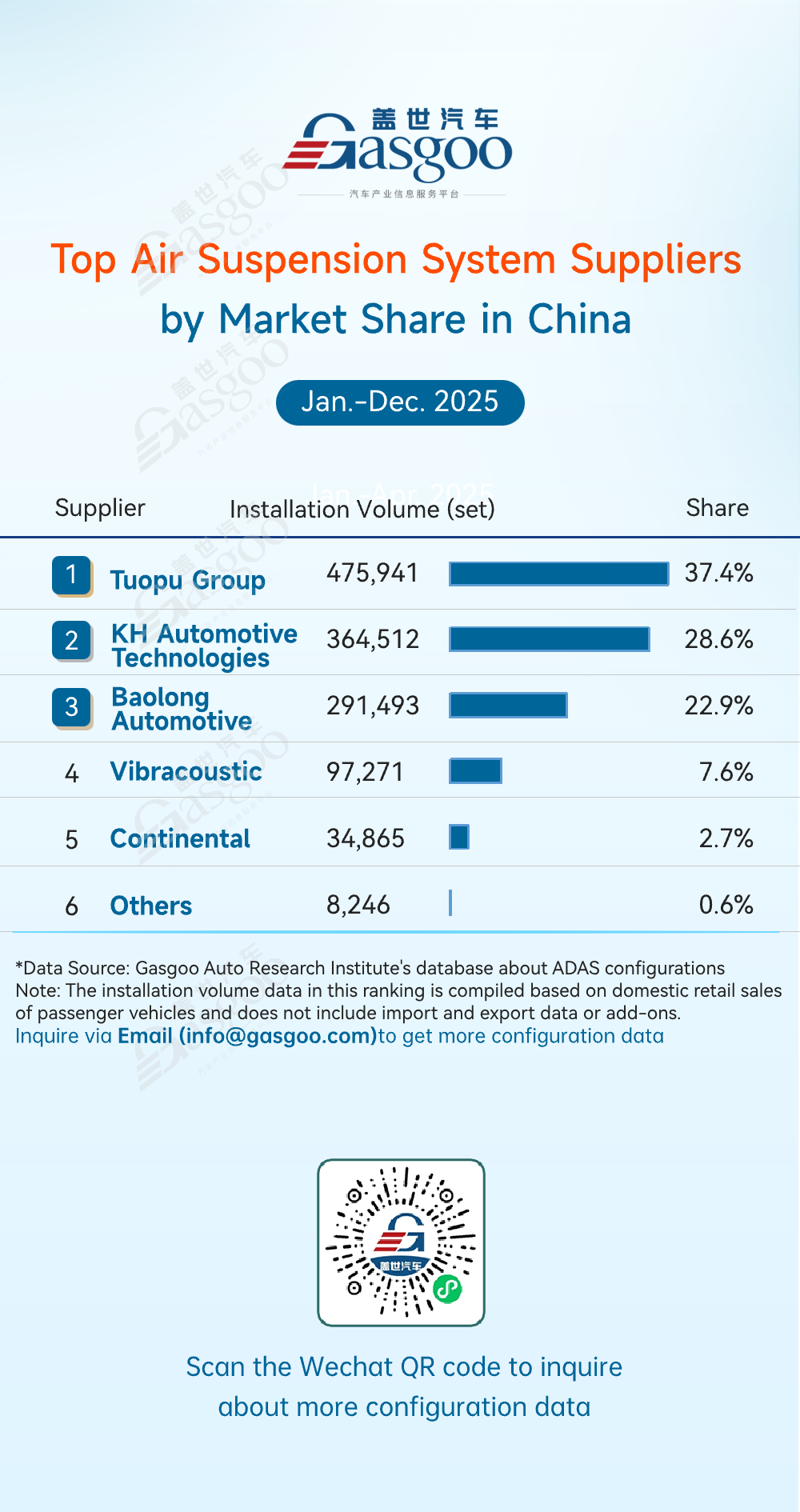

Top air suspension system suppliers

Tuopu Group: 475,941 sets installed, 37.4% market share

KH Automotive Technologies: 364,512 sets installed, 28.6% market share

Baolong Automotive: 291,493 sets installed, 22.9% market share

Vibracoustic: 97,271 sets installed, 7.6% market share

Continental: 34,865 sets installed, 2.7% market share

Others: 8,246 sets installed, 0.6% market share

In 2025, China's air suspension market was dominated by China's local players, with top suppliers highly concentrated and technologically advanced. Tuopu Group led the pack with 37.4% share (475,941 sets), followed by KH Automotive Technologies and Baolong Automotive, together capturing nearly 90% of the market. Local firms' advantages in cost, technology, and responsiveness drove this trend, while international suppliers like Vibracoustic and Continental held under 11%, underscoring the strength of China's domestic supply chain.

Top LiDAR suppliers

Huawei Technologies: 1,406,294 units installed, 41.5% market share

Hesai Technology: 1,143,162 units installed, 33.8% market share

RoboSense: 575,661 units installed, 17.0% market share

Seyond: 259,335 units installed, 7.7% market share

Others: 1,376 units installed

In 2025, China's LiDAR market was highly concentrated and led by domestic players, confirming strong growth in the sector. Huawei Technologies topped the market with 41.5% share (1,406,294 units), leveraging superior sensing accuracy, cost efficiency, and automotive-grade reliability to become the preferred choice for many high-level ADAS programs. Hesai Technology followed closely with 33.8% share.

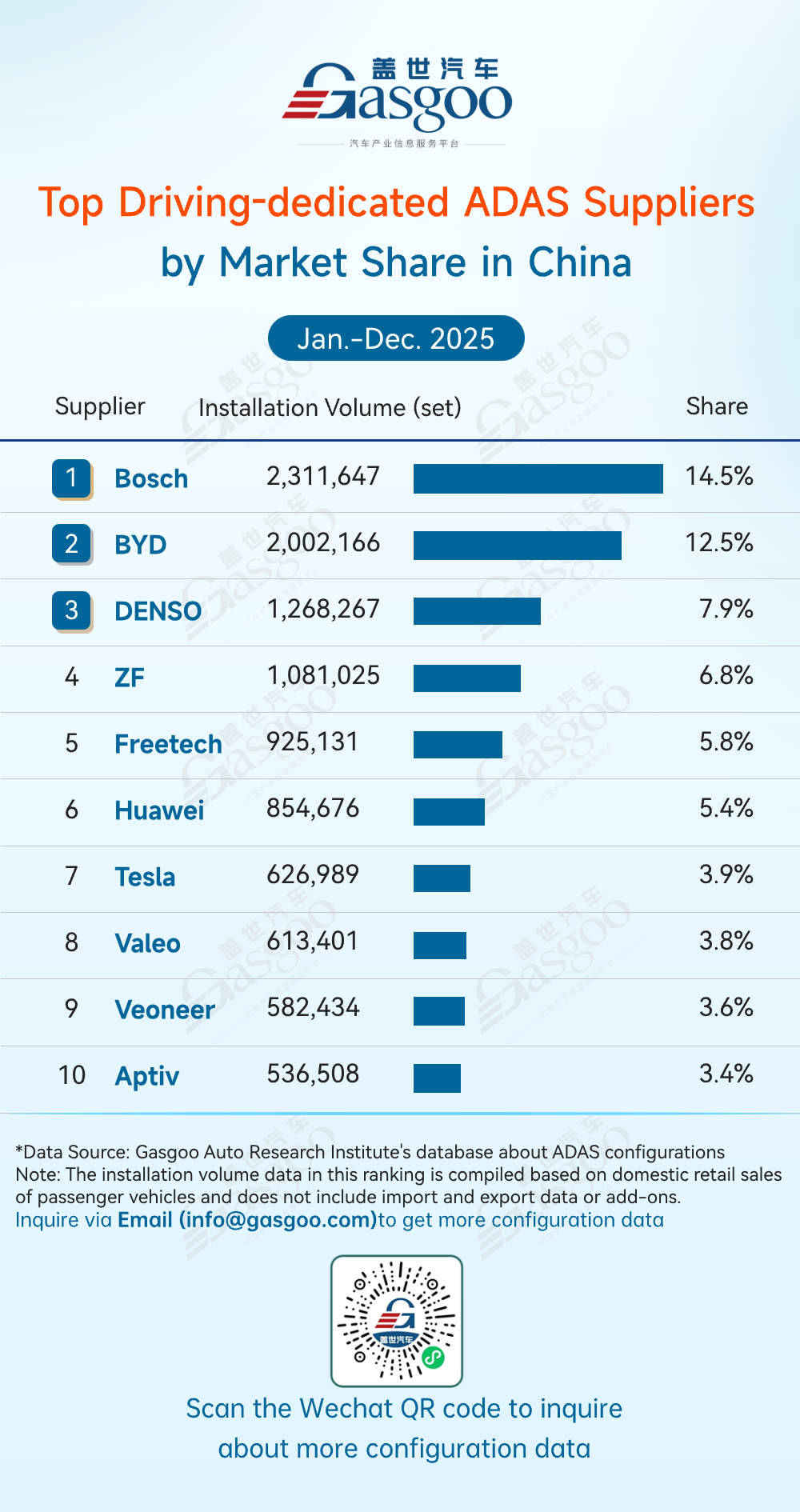

Top driving-dedicated ADAS suppliers

Bosch: 2,311,647 sets installed, 14.5% market share

BYD: 2,002,166 sets installed, 12.5% market share

DENSO: 1,268,267 sets installed, 7.9% market share

ZF: 1,081,025 sets installed, 6.8% market share

Freetech: 925,131 sets installed, 5.8% market share

Huawei: 854,676 sets installed, 5.4% market share

Tesla: 626,989 sets installed, 3.9% market share

Valeo: 613,401 sets installed, 3.8% market share

Veoneer: 582,434 sets installed, 3.6% market share

Aptiv: 536,508 sets installed, 3.4% market share

From January to December 2025, China's driving-dedicated ADAS market showed a pattern of international leaders, accelerating China's local catch-up, and rising local shares. Bosch led with 14.5% share (2,311,647 sets), mainly via front-view integrated solutions. BYD followed closely with 12.5% share (2,002,166 sets), highlighting the strength of vertical integration and confirming the trend of growing Chinese share. Local players such as Freetech and Huawei Technologies ranked among the top suppliers, leveraging algorithm innovation and cost control to become core choices for multiple OEMs, creating differentiated competition with global giants like Bosch, DENSO, and ZF.

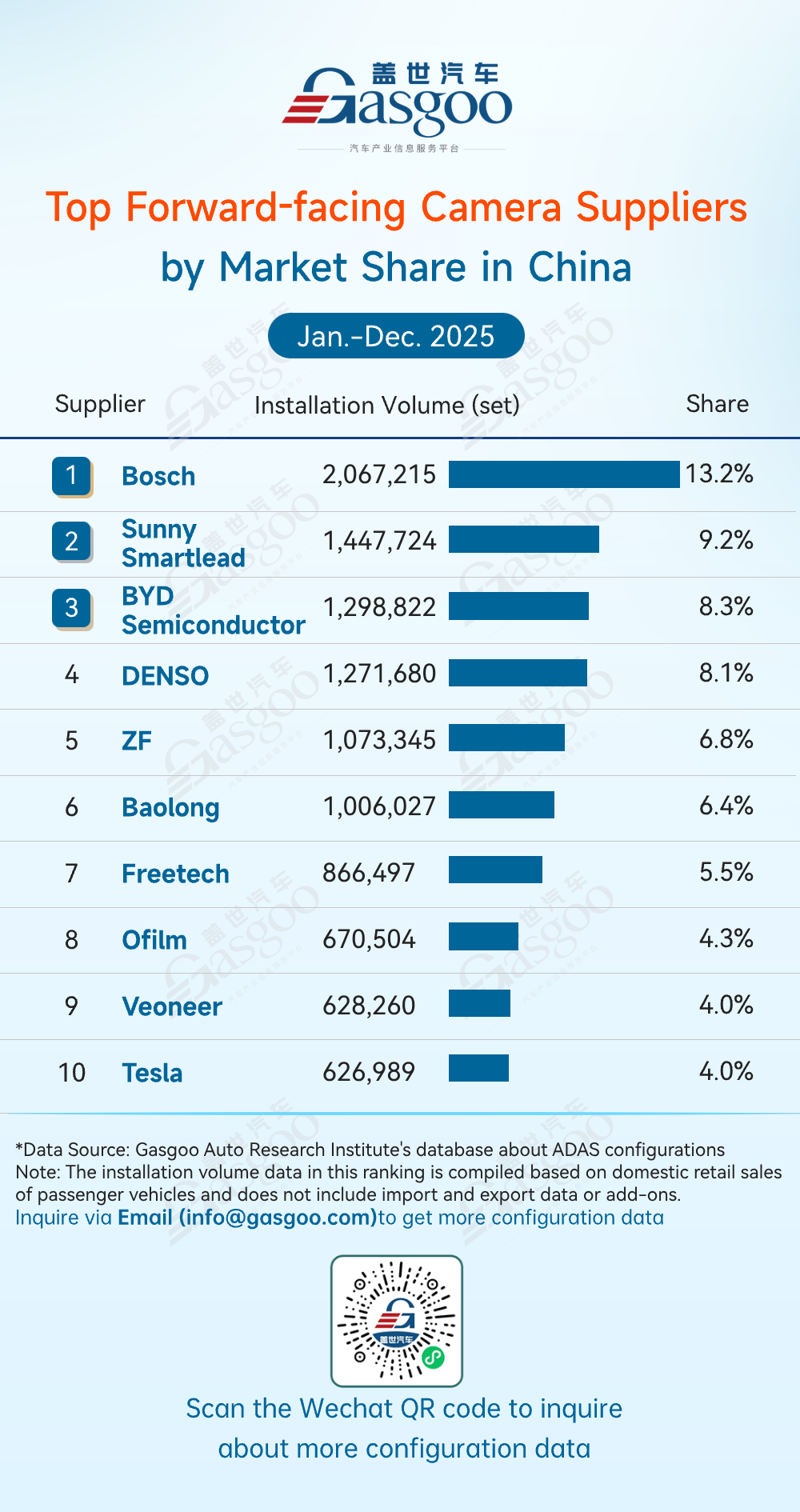

Top forward-facing camera suppliers

Bosch: 2,067,215 sets installed, 13.2% market share

Sunny Smartlead: 1,447,724 sets installed, 9.2% market share

BYD Semiconductor: 1,298,822 sets installed, 8.3% market share

DENSO: 1,271,680 sets installed, 8.1% market share

ZF: 1,073,345 sets installed, 6.8% market share

Baolong: 1,006,027 sets installed, 6.4% market share

Freetech: 866,497 sets installed, 5.5% market share

Ofilm: 670,504 sets installed, 4.3% market share

Veoneer: 628,260 sets installed, 4.0% market share

Tesla: 626,989 sets installed, 4.0% market share

From Jan.–Dec. 2025, China's forward-facing camera market was led by Bosch (13.2%, 2,067,215 sets). China's local players such as Sunny Smartlead and BYD Semiconductor followed closely, showing strong technology and production capabilities. Other local suppliers—Baolong Automotive, Freetech, and Ofilm—leveraged cost, algorithm, and application advantages to compete with international giants. Tesla also contributed to industry tech upgrades with its unique visual perception approach.

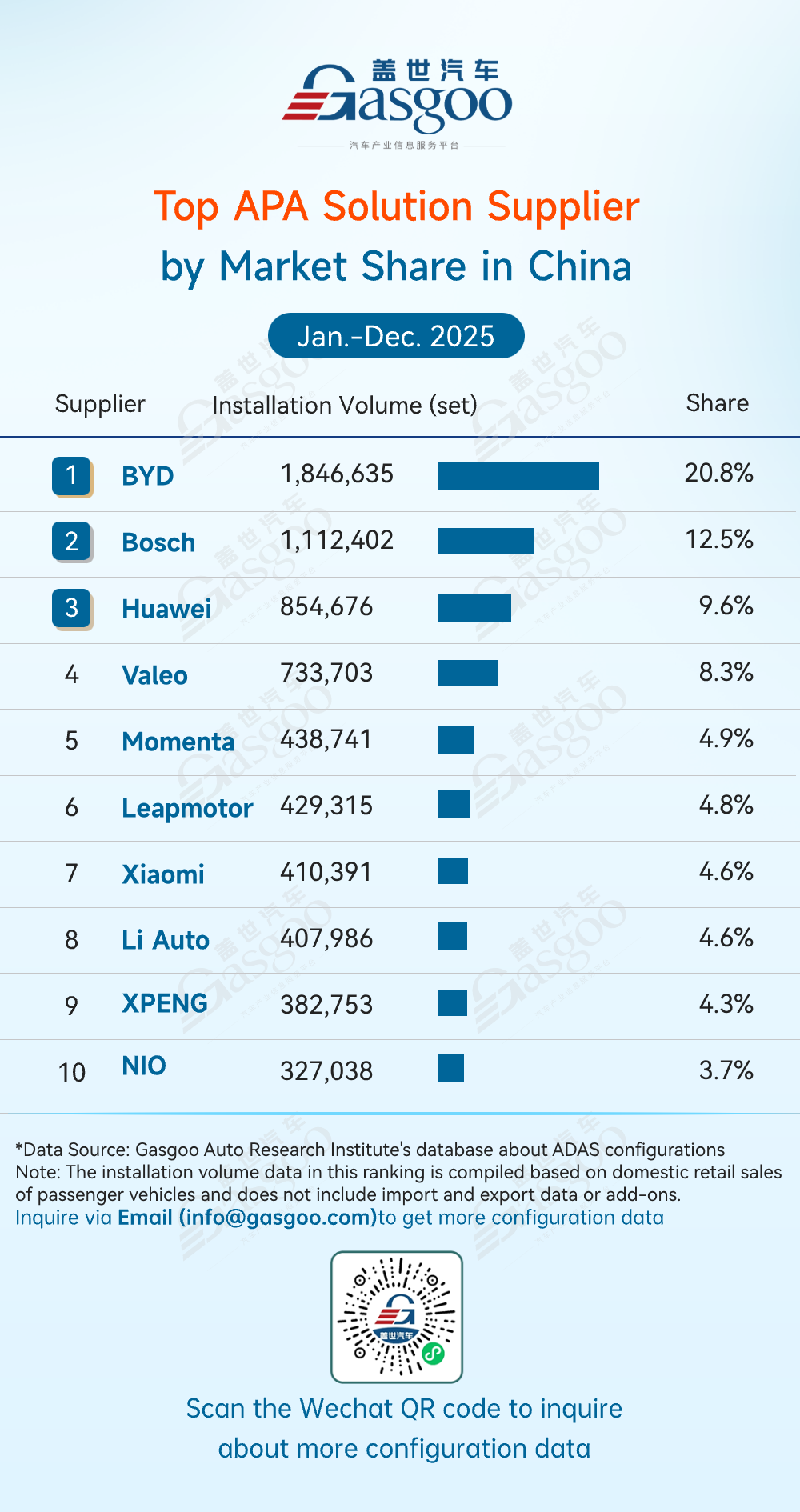

Top APA solution suppliers

BYD: 1,846,635 sets installed, 20.8% market share

Bosch: 1,112,402 sets installed, 12.5% market share

Huawei: 854,676 sets installed, 9.6% market share

Valeo: 733,703 sets installed, 8.3% market share

Momenta: 438,741 sets installed, 4.9% market share

Leapmotor: 429,315 sets installed, 4.8% market share

Xiaomi: 410,391 sets installed, 4.6% market share

Li Auto: 407,986 sets installed, 4.6% market share

XPENG: 382,753 sets installed, 4.3% market share

NIO: 327,038 sets installed, 3.7% market share

From Jan.–Dec. 2025, China's APA solution market was clearly dominated by China's local OEMs, with local suppliers gaining share. BYD ranked first at 20.8% (1,846,635 sets), leveraging its in-house APA system and strong vertical integration. Global suppliers such as Bosch and Valeo maintained solid positions, but the market remained highly concentrated: the top three players—BYD, Bosch, and Huawei—accounted for over 40% combined. Competition is shifting from basic functionality to broader scenario coverage, user experience optimization, and faster algorithm iteration, with domestic players accelerating breakthroughs in both technology autonomy and ecosystem development.

Top HD map suppliers

AutoNavi: 1,329,230 sets installed, 51.1% market share

Langge Technology: 351,491 sets installed, 13.5% market share

Tencent: 327,038 sets installed, 12.6% market share

NavInfo: 152,377 sets installed, 5.9% market share

Others: 438,727 sets installed, 16.9% market share

From Jan.–Dec. 2025, China's HD map market was highly concentrated and dominated by domestic players. AutoNavi led with a 51.1% share (1,329,230 sets), supported by strong data accuracy, update frequency, and automotive-grade integration capabilities, making it a core partner for advanced ADAS programs. Langge Technology, Tencent, and NavInfo followed, forming differentiated competition alongside the market leader. "Others" accounted for 16.9%, indicating remaining long-tail opportunities. Overall, leading firms continue to consolidate advantages through sustained R&D investment, while the rise of China's suppliers strengthens China's ADAS ecosystem and technological self-reliance.

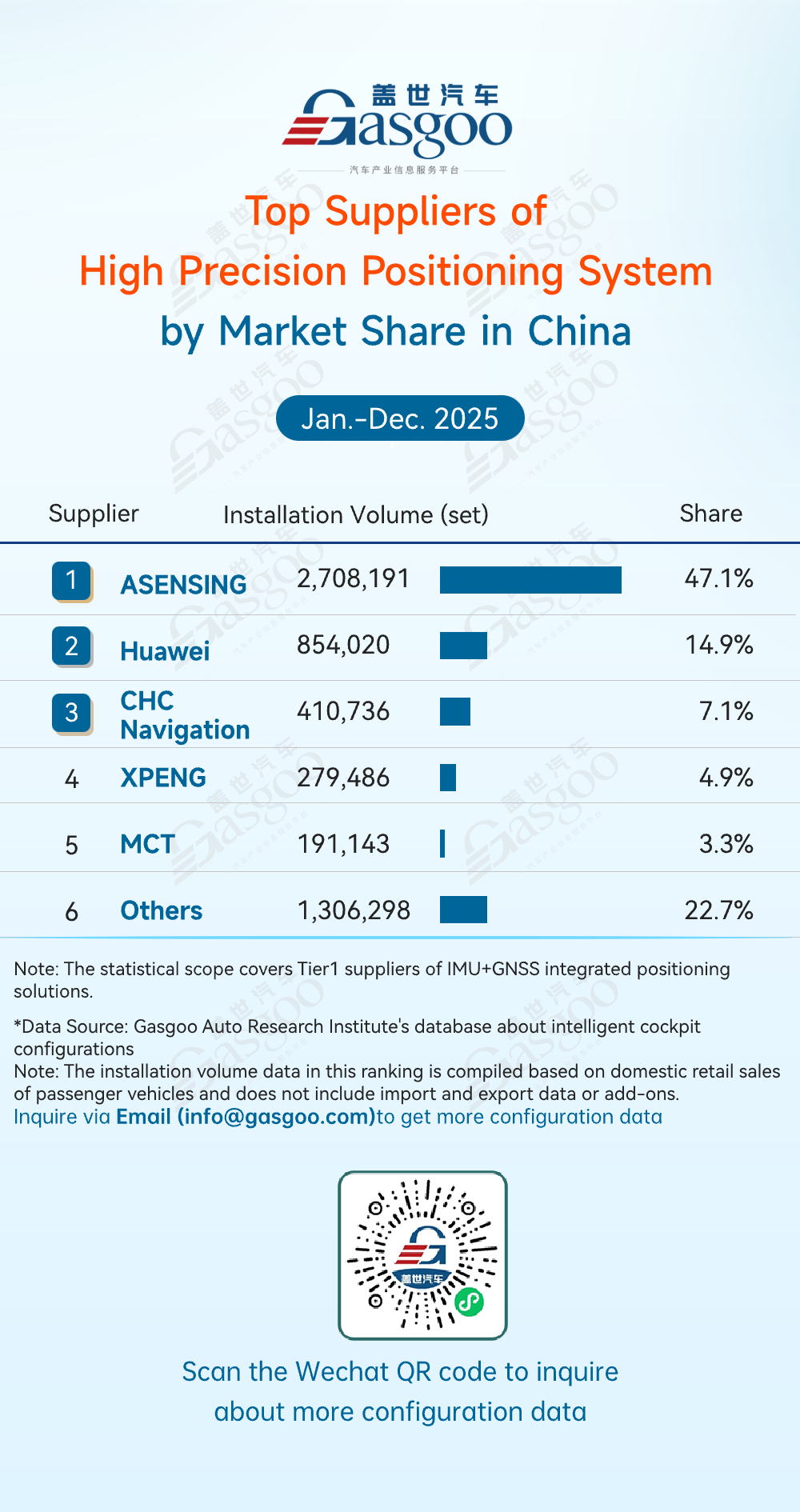

Top suppliers of high precision positioning system

ASENSING: 2,708,191 sets installed, 47.1% market share

Huawei: 854,020 sets installed, 14.9% market share

CHC Navigation: 410,736 sets installed, 7.1% market share

XPENG: 279,486 sets installed, 4.9% market share

MCT: 191,143 sets installed, 3.3% market share

Others: 1,306,298 sets installed, 22.7% market share

From Jan.–Dec. 2025, the high precision positioning market showed a clear leader with diversified participation. ASENSING ranked first with a 47.1% share (2,708,191 sets), reflecting its strong scale advantage and deep penetration in automotive-grade positioning solutions. Huawei, CHC Navigation, XPENG, and MCT followed, building differentiated positions across various application scenarios. Meanwhile, "Others" accounted for 22.7% of the market, indicating a still-diversified supply structure and room for new entrants and alternative technology routes.