According to Gasgoo Automotive Research Institute, as automotive intelligence and electrification continue to accelerate, the smart cockpit is shifting from "feature upgrades" to "experience reconfiguration," becoming a key lever for vehicle differentiation. From smart speech solution to AR-HUD, in-vehicle human–machine interaction is evolving rapidly, driving fast changes across the hardware and software supply chain. Meanwhile, stronger in-house development capabilities among automakers and the accelerated entry of cross-industry tech players are further intensifying competition in the smart cockpit market.

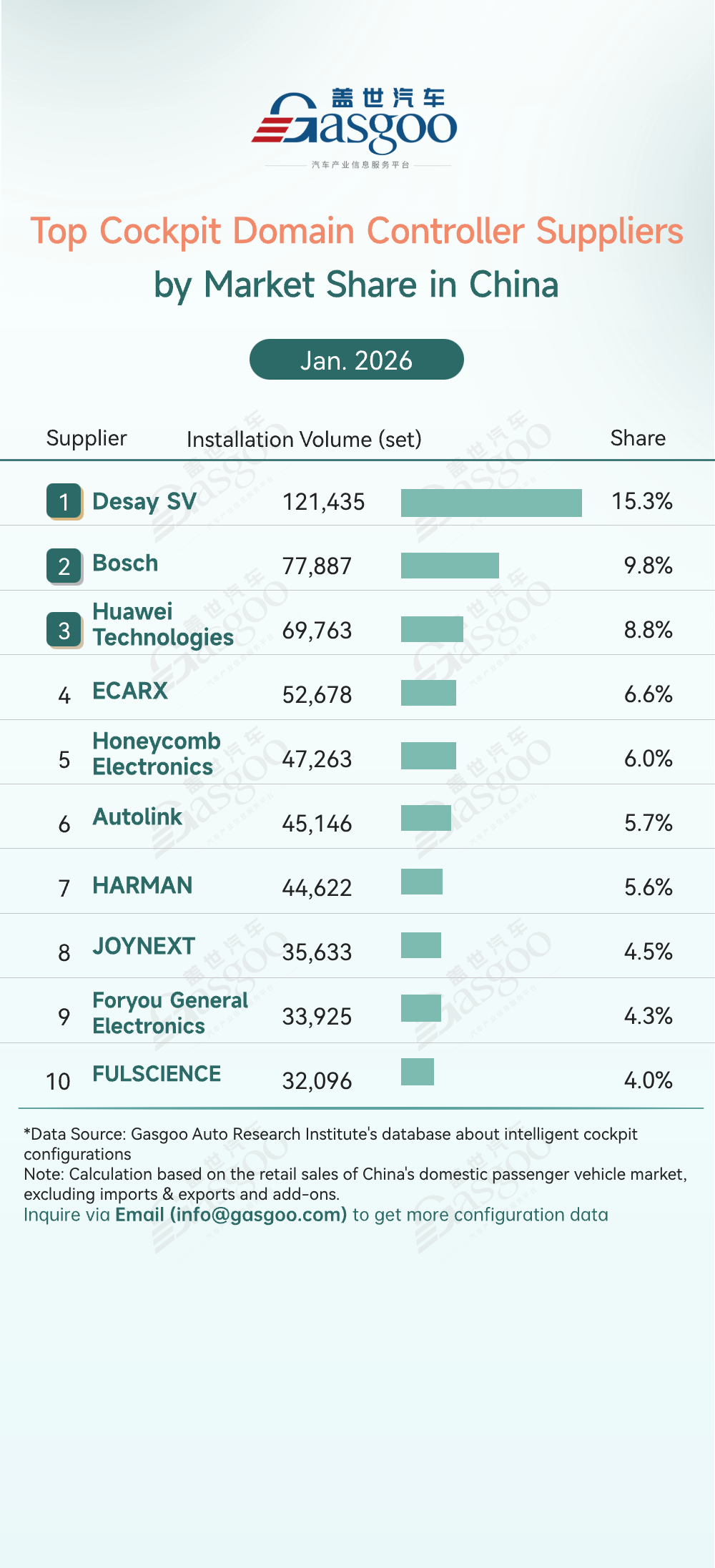

Top cockpit domain controller suppliers

Desay SV: 1,562,992 sets installed, 16.1% market share

Bosch: 778,887 sets installed, 9.8% market share

Huawei Technologies: 697,763 sets installed, 8.8% market share

ECARX: 526,678 sets installed, 6.6% market share

Honeycomb Electronics: 472,663 sets installed, 6.0% market share

Autolink: 451,466 sets installed, 5.7% market share

HARMAN: 446,226 sets installed, 5.6% market share

Joynext: 356,633 sets installed, 4.5% market share

Foryou General Electronics: 339,255 sets installed, 4.3% market share

FULSCIENCE: 320,966 sets installed, 4.0% market share

In January 2026, Desay SV led the cockpit domain controller market with 121,435 sets installed (15.3% share), clearly ahead of other suppliers. Bosch (77,887 sets, 9.8%) and Huawei Technologies (69,763 sets, 8.8%) ranked second and third, forming the leading tier with a notable gap. Mid-tier suppliers such as ECARX, Honeycomb Electronics, Autolink, and HARMAN held relatively balanced shares of 4.5%–6.6%, reflecting ongoing competition. Meanwhile, JOYNEXT, Foryou General Electronics, and FULSCIENCE each recorded less than 5%, indicating a moderately concentrated market where leading players maintain clear advantages.

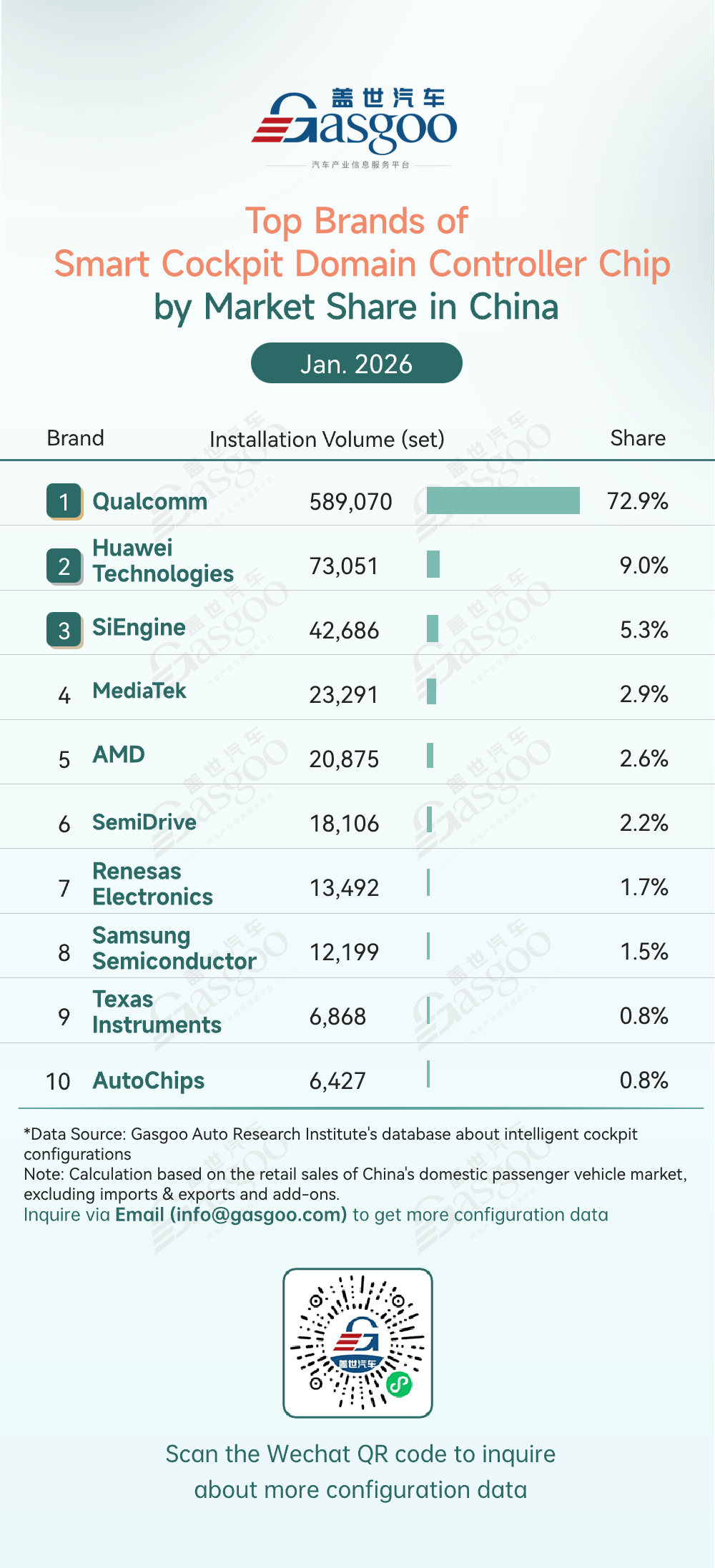

Top brands of smart cockpit domain controller chip

Qualcomm: 589,070 units installed, 72.9% market share.

Huawei Technologies: 73,051 units installed, 9.0% market share.

SiEngine: 42,686 units installed, 5.3% market share.

MediaTek: 23,291 units installed, 2.9% market share.

AMD: 20,875 units installed, 2.6% market share.

SemiDrive: 18,106 units installed, 2.2% market share.

Renesas Electronics: 13,492 units installed, 1.7% market share.

Samsung Semiconductor: 12,199 units installed, 1.5% market share.

Texas Instruments: 6,868 units installed, 0.8% market share.

AutoChips: 6,427 units installed, 0.8% market share.

In January 2026, the cockpit domain controller chip market showed a clear pattern of high concentration at the top. Qualcomm led the pack by a wide margin with 589,070 units installed (72.9% share), forming a dominant "single-leader" structure. In the second tier, Huawei Technologies and SiEngine ranked second and third with shares of 9.0% and 5.3%, respectively, as domestic chipmakers accelerated large-scale adoption in vehicles. Meanwhile, suppliers such as MediaTek, AMD, and SemiDrive held shares in the 2%–3% range, competing in a crowded mid-tier, while Renesas Electronics, Samsung Semiconductor, Texas Instruments, and AutoChips also secured top-ten positions.

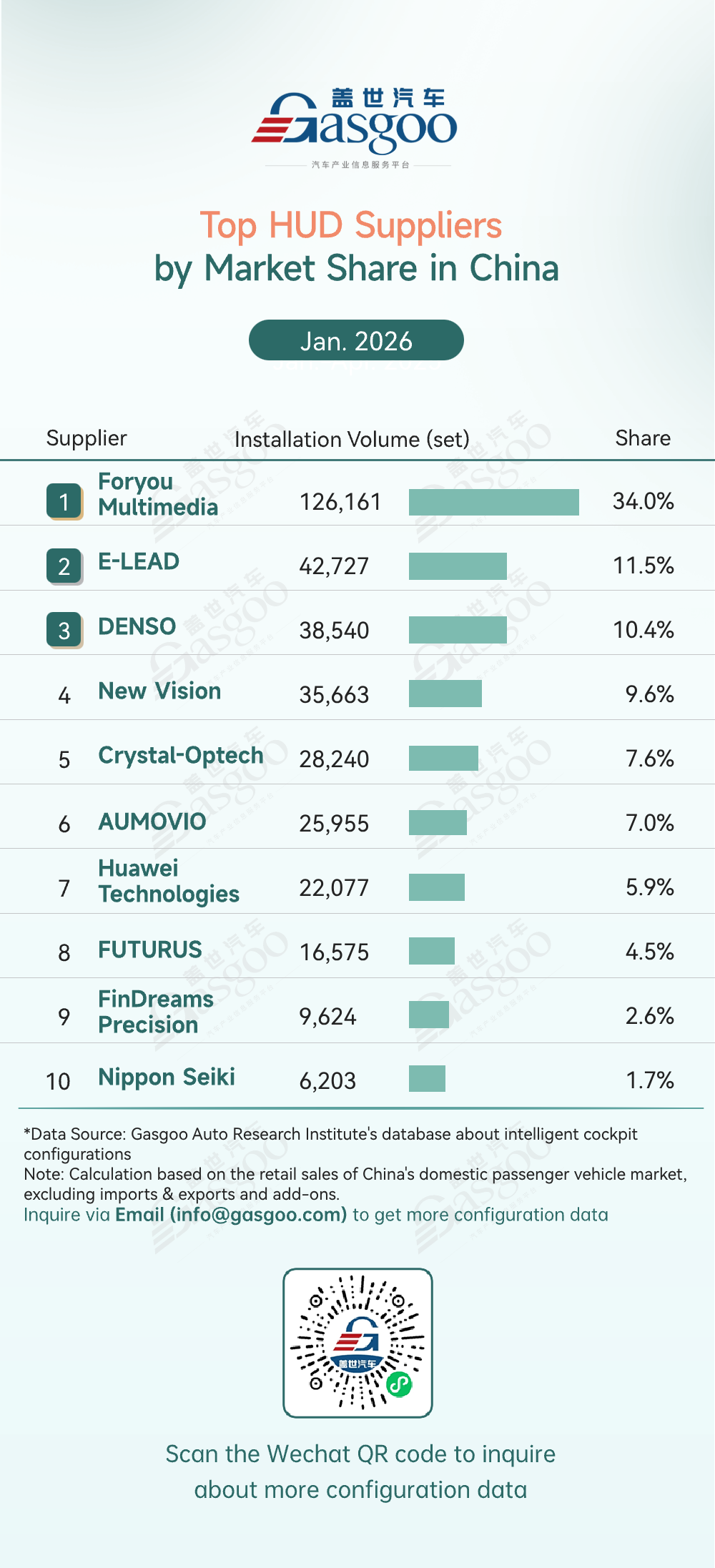

Top HUD suppliers

Foryou Multimedia: 126,161 sets installed, 34.0% market share.

E-LEAD: 42,727 sets installed, 11.5% market share.

DENSO: 38,540 sets installed, 10.4% market share.

New Vision: 35,663 sets installed, 9.6% market share.

Crystal-Optech: 28,240 sets installed, 7.6% market share.

AUMOVIO: 25,955 sets installed, 7.0% market share.

Huawei Technologies: 22,077 sets installed, 5.9% market share.

FUTURUS: 16,575 sets installed, 4.5% market share.

FinDreams Precision: 9,624 sets installed, 2.6% market share.

Nippon Seiki: 6,203 sets installed, 1.7% market share.

From the HUD supplier installation rankings (Jan. 2026), the market showed relatively high concentration at the top, with intense competition in the second tier. Foryou Multimedia ranked first with 126,161 sets installed (34.0% share), maintaining a clear lead and demonstrating strong large-scale supply capabilities. In the second tier, E-LEAD, DENSO, and New Vision each held around 10% share, with similar installation volumes and close competition. Meanwhile, Crystal-Optech and AUMOVIO were positioned in the mid-tier with shares of about 7%. Suppliers such as Huawei Technologies and FUTURUS are also accelerating their strategic expansion in intelligent and AR-HUD products, further strengthening their market presence.

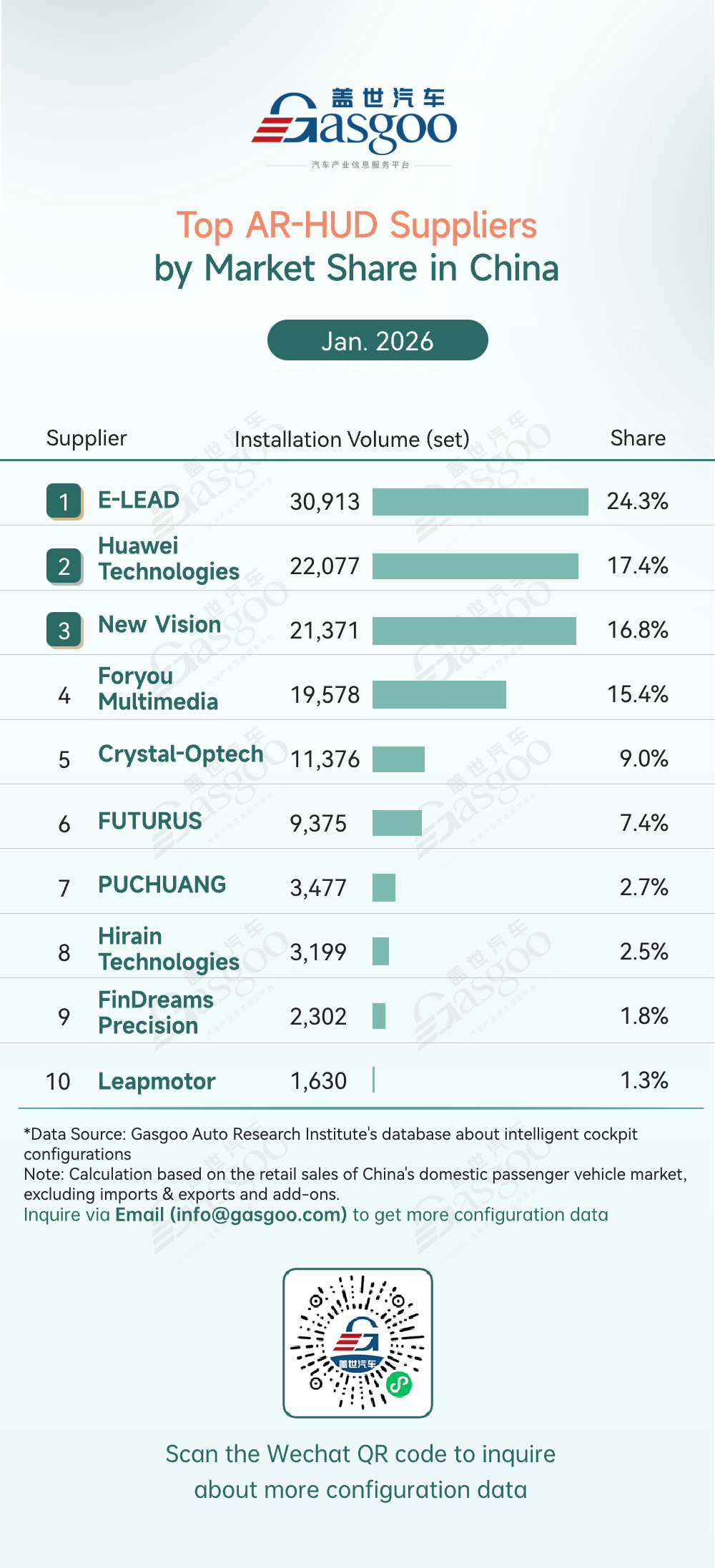

Top AR-HUD suppliers

E-LEAD: 30,913 sets installed, 24.3% market share.

Huawei Technologies: 22,077 sets installed, 17.4% market share.

New Vision: 21,371 sets installed, 16.8% market share.

Foryou Multimedia: 19,578 sets installed, 15.4% market share.

Crystal-Optech: 11,376 sets installed, 9.0% market share.

FUTURUS: 9,375 sets installed, 7.4% market share.

PUCHUANG: 3,477 sets installed, 2.7% market share.

Hirain Technologies: 3,199 sets installed, 2.5% market share.

FinDreams Precision: 2,302 sets installed, 1.8% market share.

Leapmotor: 1,630 sets installed, 1.3% market share.

In January 2026, the AR-HUD market showed a multi-player competitive landscape with relatively fragmented concentration. E-LEAD ranked first with 30,913 sets installed (24.3% share), but its lead was not significant. Huawei Technologies and New Vision followed closely with shares of 17.4% and 16.8%, respectively, reflecting intense competition among leading players. Foryou Multimedia and Crystal-Optech formed the second tier, each holding market shares between 9% and 15%. Other suppliers such as PUCHUANG, Hirain Technologies, FinDreams Precision, and Leapmotor also entered the top ten, mainly driven by project-based supply or in-house deployment.

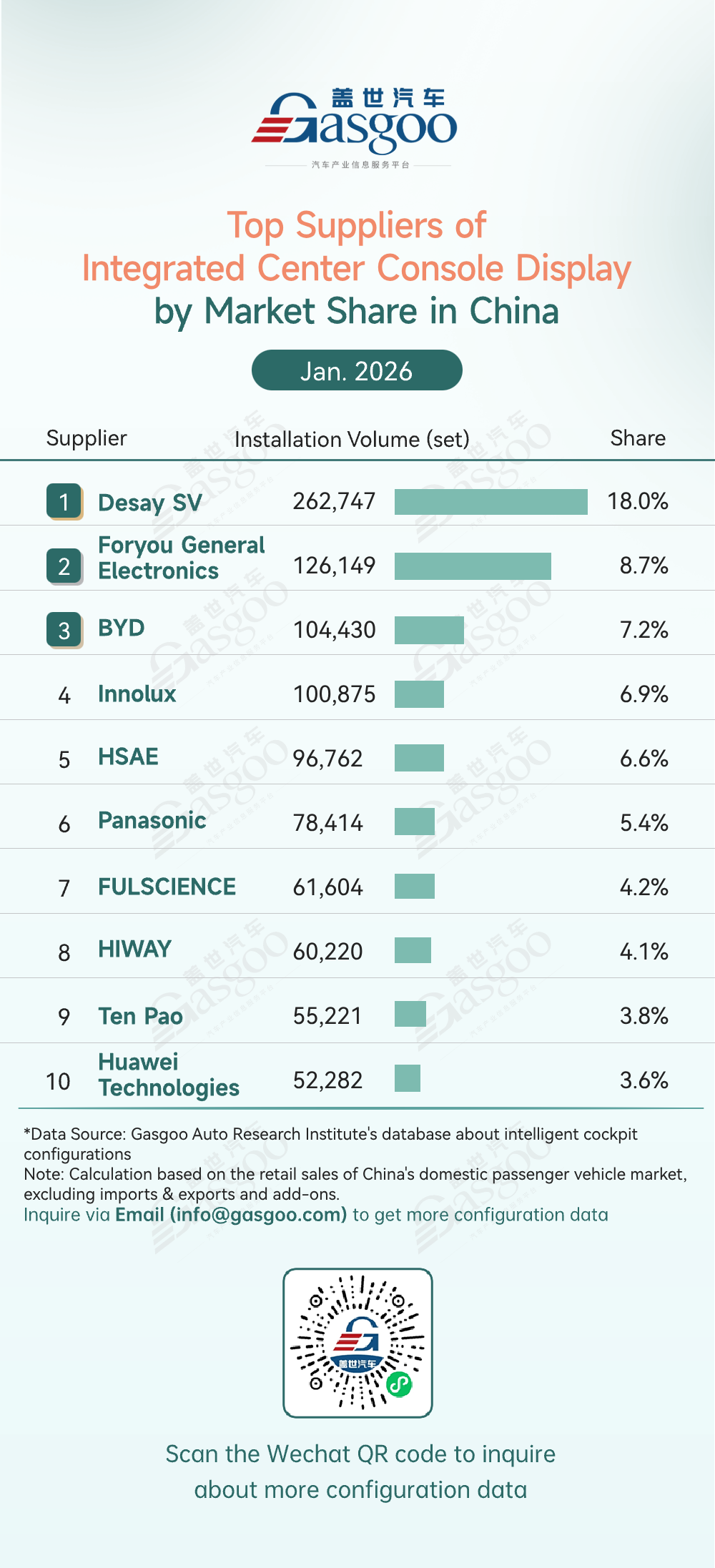

Top suppliers of integrated center console display

Desay SV: 262,747 sets installed, 18.0% market share.

Foryou General Electronics: 126,149 sets installed, 8.7% market share.

BYD: 104,430 sets installed, 7.2% market share.

Innolux: 100,875 sets installed, 6.9% market share.

HSAE: 96,762 sets installed, 6.6% market share.

Panasonic: 78,414 sets installed, 5.4% market share.

FULSCIENCE: 61,604 sets installed, 4.2% market share.

HIWAY: 60,220 sets installed, 4.1% market share.

Ten Pao: 55,221 sets installed, 3.8% market share.

Huawei Technologies: 52,282 sets installed, 3.6% market share.

From the central display integration supplier installation rankings (Jan. 2026), the market showed a pattern of a leading top player with overall fragmented competition. Desay SV ranked first with 262,747 sets installed (18.0% share), demonstrating a clear scale advantage but not an absolute monopoly. In the second tier, Foryou General Electronics, BYD, and Innolux held shares between 7% and 9%, with similar installation volumes, reflecting tight competition. HSAE and Panasonic formed the mid-tier, each maintaining 5%–7% market share, while FULSCIENCE, HIWAY, and Ten Pao hovered around 4%. Huawei Technologies entered the top ten with a 3.6% share, indicating its continued expansion in the smart cockpit sector.

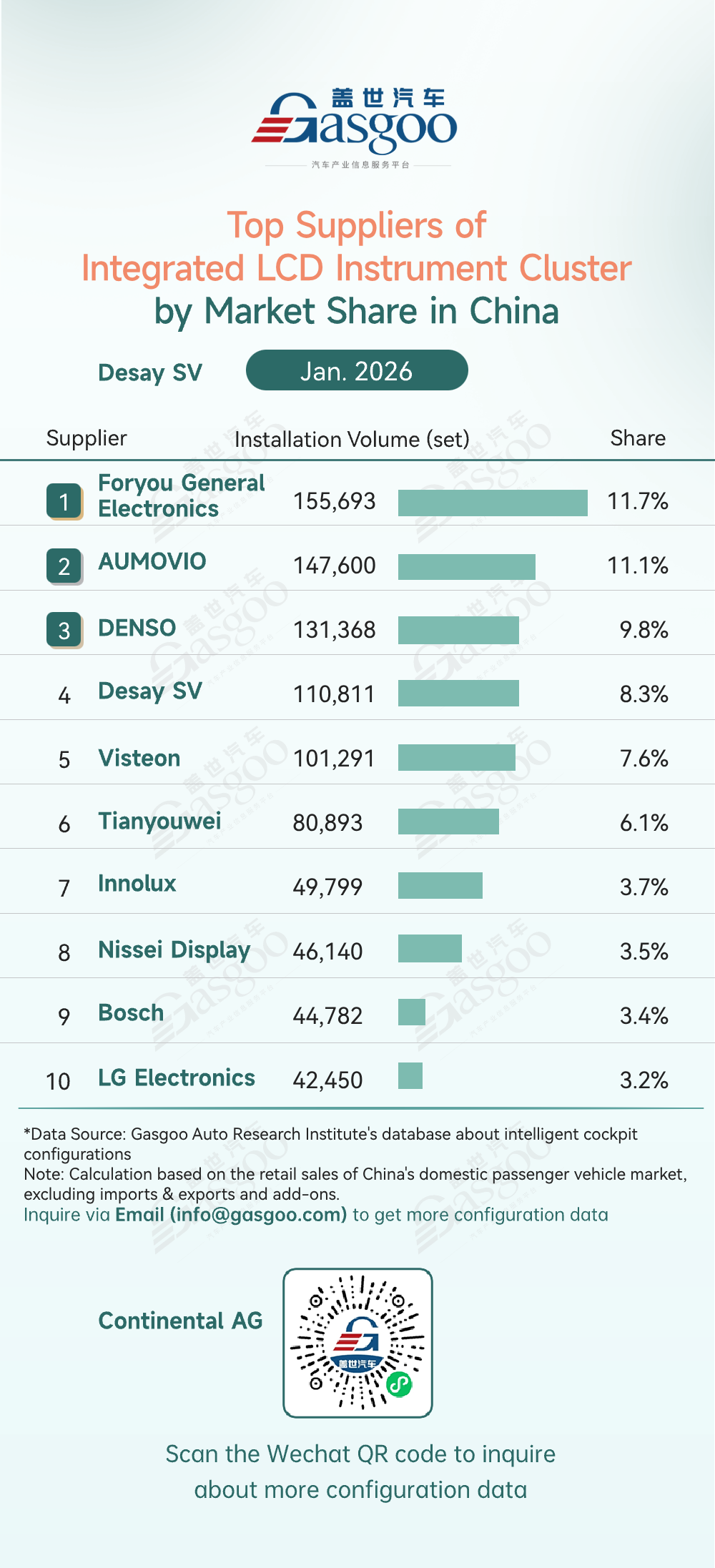

Top suppliers of integrated LCD instrument cluster

Foryou General Electronics: 155,693 sets installed, 11.7% market share

AUMOVIO: 147,600 sets installed, 11.1% market share

DENSO: 131,368 sets installed, 9.8% market share

Desay SV: 110,811 sets installed, 8.3% market share

Visteon: 101,291 sets installed, 7.6% market share

Tianyouwei: 80,893 sets installed, 6.1% market share

Innolux: 49,799 sets installed, 3.7% market share

Nissei Display: 46,140 seits installed, 3.5% market share

Bosch: 44,782 sets installed, 3.4% market share

LG Electronics: 42,450 sets installed, 3.2% market share

In January 2026, the LCD instrument panel integration market showed a close top tier and overall dispersed competition. Foryou General Electronics led the pack with 155,693 sets (11.7%), followed by AUMOVIO (11.1%) and DENSO (9.8%), with limited gaps among them. Desay SV and Visteon held 7%–8%, Tianyouwei 6.1%, while Innolux, Nissei Display, Bosch, and LG Electronics each stayed below 4%. As full-LCD panels penetrate further and cockpit integration advances, supplier scale and tech collaboration will increasingly shape the market.

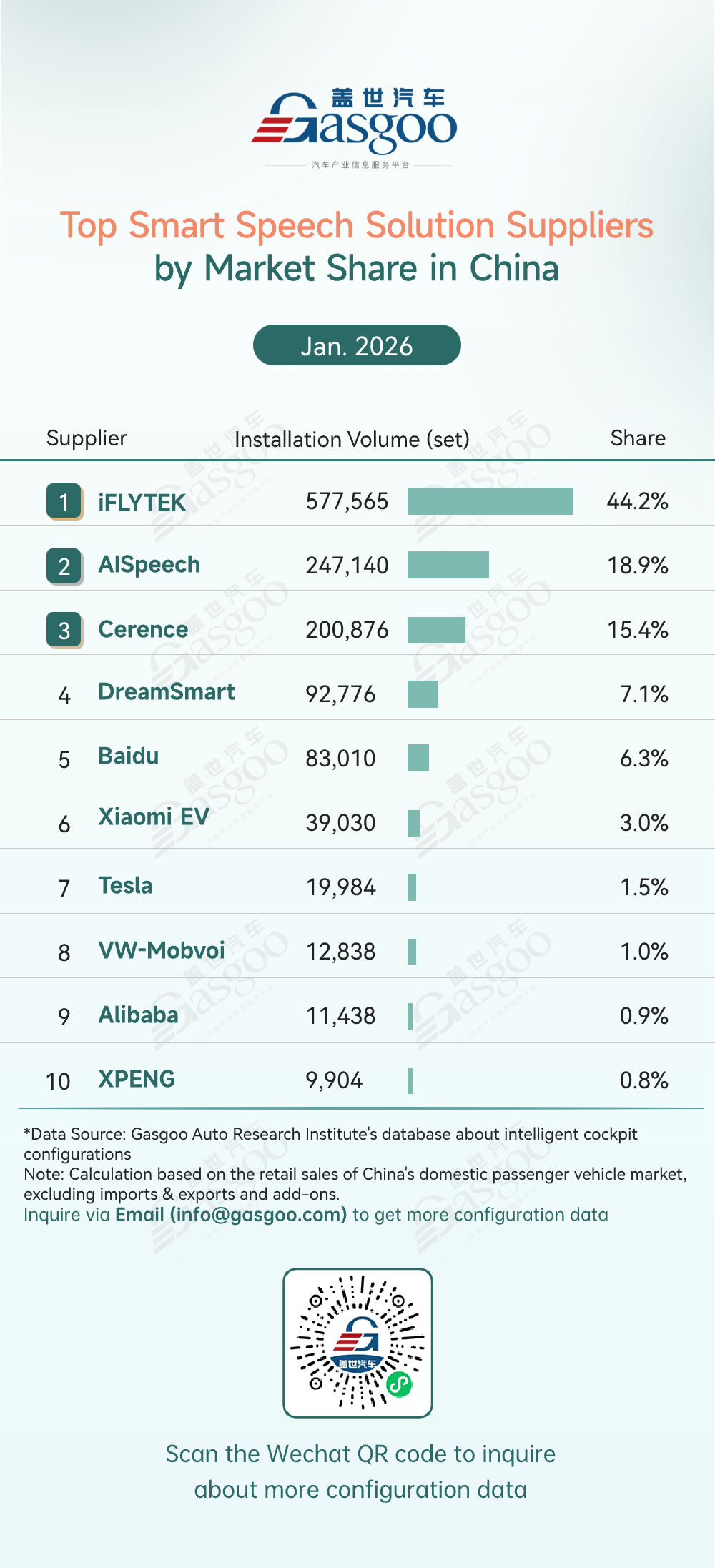

Top smart speech solution suppliers

iFLYTEK: 577,565 sets installed, 44.2% market share

AISpeech: 247,140 sets installed, 18.9% market share

Cerence: 200,876 sets installed, 15.4% market share

DreamSmart: 92,776 sets installed, 7.1% market share

Baidu: 83,010 sets installed, 6.3% market share

Xiaomi EV: 39,030 sets installed, 3.0% market share

Tesla: 19,984 sets installed, 1.5% market share

VW-Mobvoi: 12,838 sets installed, 1.0% market share

Alibaba: 11,438 sets installed, 0.9% market share

XPENG: 9,904 sets installed, 0.8% market share

In January 2026, the smart speech solution supplier market showed high concentration at the top, with a clear advantage for the leading tier. iFLYTEK took the lead with 577,565 sets installed (44.2% share), reflecting its strong capabilities in voice algorithms, customer coverage, and large-scale deployment. The second tier was led by AISpeech and Cerence, holding 18.9% and 15.4% respectively, forming the core competitive group. DreamSmart and Baidu maintained a stable position with 6%–7% shares. In the tail segment, Tesla, VW-Mobvoi, Alibaba, and XPENG each held less than 2%, mainly supporting self-developed or project-specific solutions.