Gasgoo Munich- China's power battery industry showed clear signs of seasonal adjustment in February 2026, as the Chinese New Year holiday dampened short-term production and sales activity. Despite the monthly slowdown, the sector continued to exhibit structural improvements, with growth drivers gradually shifting toward overseas markets and energy storage applications.

Data released by the China Automotive Battery Innovation Alliance indicates that while production and sales of power and energy storage batteries declined from the previous month, both indicators still maintained double-digit year-on-year growth. Exports of power batteries and the rapid expansion of the energy storage segment have emerged as the primary forces driving industry momentum.

At the same time, domestic battery installations in new energy vehicles declined compared with a year earlier, highlighting a period of market realignment in which technology pathways and competitive positions are increasingly diverging. The industry is gradually shifting from a phase of rapid capacity expansion toward one focused on efficiency, technological advancement, and higher-quality growth.

Energy storage and overseas demand are now acting as the two main engines behind the sector's evolving growth model.

In February, the industry demonstrated resilience despite a complicated market backdrop. A surge in energy storage battery demand, coupled with strong export growth for power batteries, continued to reshape the sources of industry expansion.

Total production of power and energy storage batteries reached 141.6 GWh in February, representing a 15.7% decline from the previous month but still a robust 41.3% surge year on year., according to data from the China Automotive Power Battery Industry Innovation Alliance (CAPBIIA). For the first two months of 2026, cumulative output climbed to 309.7 GWh, up 48.8% compared with the same period last year.

From a technology perspective, lithium iron phosphate (LFP) batteries continued to dominate production. In February, LFP output totaled 114.6 GWh, accounting for roughly 80.9% of total production and rising 41.7% year on year, supported by their cost advantages and strong safety profile in both EV and energy storage applications. Batteries using ternary materials, often favored in higher-end electric vehicles for their energy density, reached 26.9 GWh in output, representing about 19% of the total and increasing 39.7% year on year.

Changes in the sales mix further highlight shifting industry dynamics. Combined sales of power and energy storage batteries totaled 113.2 GWh in February, down 23.9% from the previous month but up 25.7% year on year. Energy storage batteries stood out as the fastest-growing segment, with February sales reaching 38.6 GWh—an increase of 67.3% from a year earlier. During the first two months of the year, energy storage battery sales surged to 84.8 GWh, more than doubling compared with the same period in 2025. The segment accounted for 32.4% of total battery sales, a rise of 8.6 percentage points year on year, reflecting accelerating deployment of renewable energy storage systems globally as well as increasing integration of wind, solar, and storage projects in China.

Exports also played a pivotal role in sustaining industry growth. In February, China exported a combined 23.9 GWh of power and energy storage batteries, up 13.2% year on year and representing about 20.6% of total monthly sales.

Of those, power battery exports reached 16.9 GWh last month, rising 31.9% from a year earlier.Its cumulative exports for January and February totaled 34.6 GWh, up 44.6% year on year.

Meanwhile, although energy storage battery exports declined 15.5% year on year in February, they grew 9.3% compared with the previous month, suggesting signs of a gradual recovery in overseas storage demand.

At the same time, the competitive landscape within China's power battery market is becoming increasingly differentiated, with technology alignment and application-specific solutions emerging as key competitive factors.

Domestic power battery installations declined year on year in February, yet the data also revealed intensifying competition among leading manufacturers and stronger momentum among second-tier suppliers. As the market matures, companies are increasingly focusing on aligning specific battery technologies with targeted vehicle segments and use cases.

Battery installations in China's new energy vehicles totaled 26.3 GWh in February, representing a 37.4% decline from January and a 24.6% drop compared with the same month last year. For the January–February period, installations reached 68.3 GWh, down 7.2% year on year, largely reflecting slower vehicle production during the Chinese New Year holiday period.

In terms of technology adoption, LFP batteries continued to dominate installations, reaching 20.6 GWh in February and accounting for 78.3% of the total, though this figure represented a year-on-year decline of 27.5%. Ternary batteries recorded installations of 5.7 GWh, representing 21.7% of the total and falling 11.4% year on year. Despite the decline, ternary batteries remain essential in premium passenger vehicles due to their higher energy density, with installations for the first two months of the year still showing a slight increase compared with the same period in 2025.

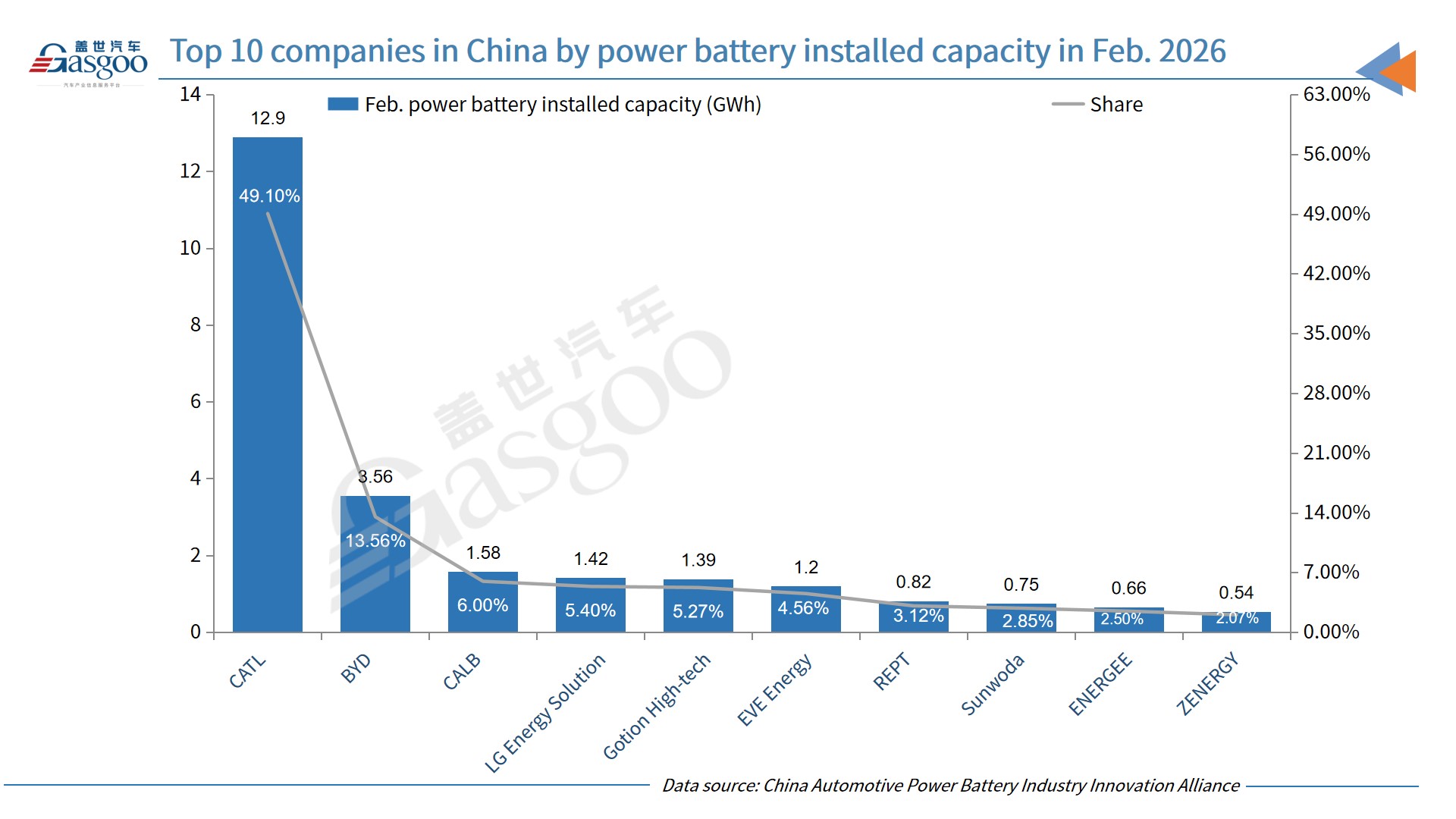

The competitive structure of the market continues to be shaped by dominant leaders and a growing group of challengers. CATL maintained its top position in February with 12.9 GWh of installed batteries, capturing 49.1% of the market. BYD ranked second with 3.56 GWh and a 13.56% share. However, both companies saw their market shares decline slightly compared with the previous month.

Meanwhile, second-tier battery manufacturers have been gaining ground. CALB recorded installations of 1.58 GWh in February, accounting for 6% of the market and increasing its share from the previous month by 0.72 percentage points. LG Energy Solution also expanded its presence, reaching 1.42 GWh in installations and raising its market share to 5.4%, supported by its strength in ternary battery technology. Other players such as Gotion High-Tech, Sunwoda, and REPT BATTERO also reported year-on-year gains in market share during the first two months of the year, suggesting a gradual diversification of the industry landscape.

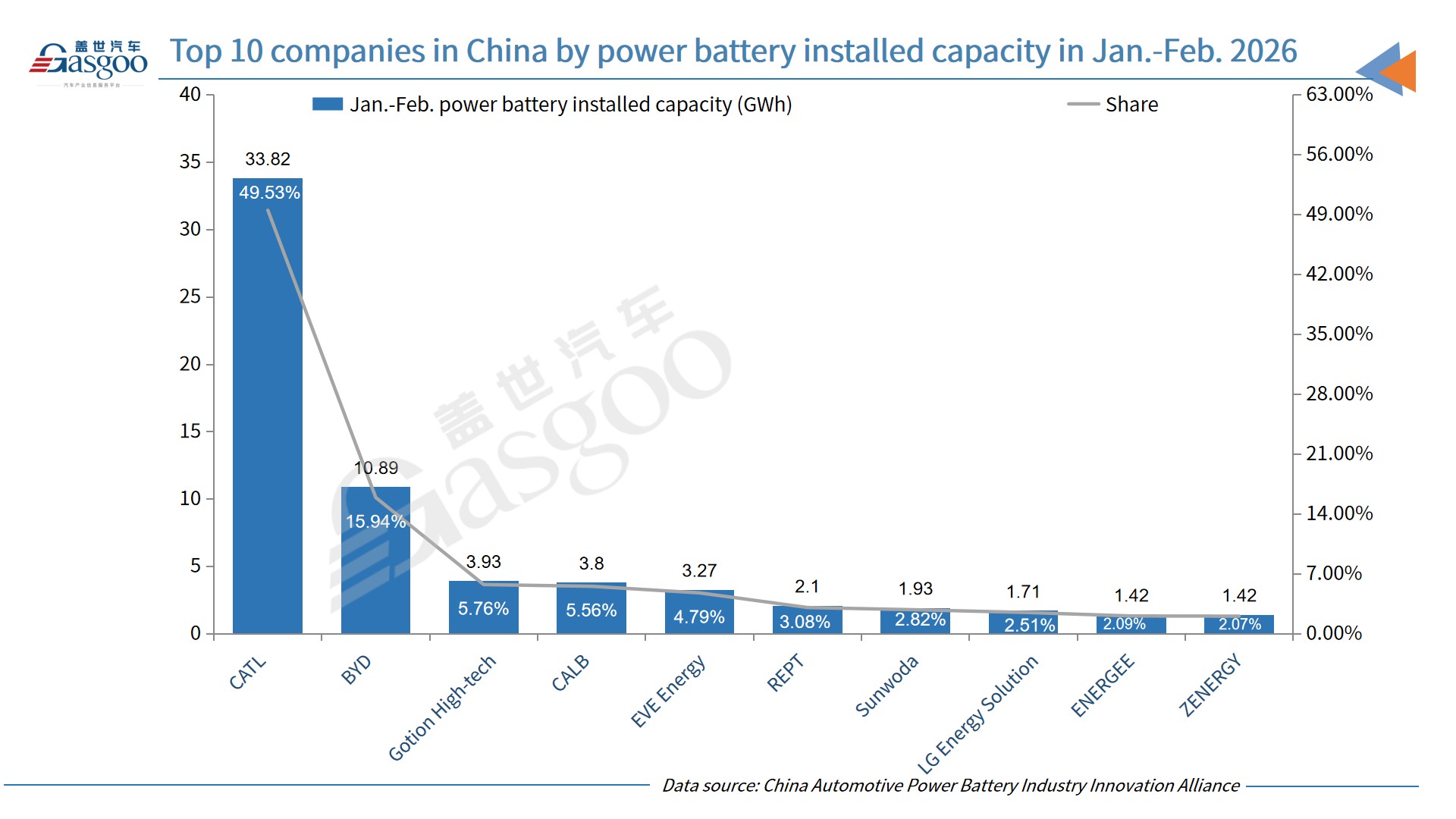

Looking at the first two months of 2026, a total of 35 battery manufacturers supplied installed capacity for China's NEV market, six fewer than during the same period last year. Despite the smaller number of participating suppliers, market concentration remained strikingly high.

Image source: CATL

Combined installations by the two largest battery producers reached 44.7 GWh during the January–February period, capturing 65.4% of the market. The five biggest suppliers collectively accounted for 55.7 GWh, or 81.5% of total installations, while the top ten companies delivered 64.3 GWh, representing 94.1% of the market. Although this share slipped slightly—down 0.9 percentage points from a year earlier—the data still underscores the overwhelming dominance of leading battery manufacturers in China's rapidly evolving electric vehicle industry.

Application patterns across vehicle segments are also evolving. Battery installations in battery electric passenger vehicles accounted for 58.8% of the total in February, remaining the largest application despite a year-on-year decline. Full-electric trucks showed particularly strong growth, representing 24.6% of installations and rising 5.8% from a year earlier, while cumulative installations in this segment grew more than 20% during the first two months of the year. Plug-in hybrid trucks and specialized commercial vehicles emerged as new growth areas, posting triple-digit year-on-year growth rates in February and underscoring the accelerating electrification of commercial transport.

Another notable trend is the rapid rise in average battery capacity per vehicle. In February, new energy vehicles in China carried an average battery pack of 75.9 kWh, up 52.6% year on year. Battery electric passenger cars averaged 68.6 kWh per vehicle, reflecting a 28.5% increase and highlighting growing consumer demand for longer driving range.

Taken together, the data suggests that China's power battery sector is undergoing a period of structural transformation in 2026. Rapid expansion in energy storage and steady growth in export markets are providing new engines of industry growth, while short-term fluctuations in domestic EV installations are pushing companies to accelerate innovation and refine technology deployment across different use cases.

As LFP batteries continue improving in energy density and ternary batteries maintain their role in premium vehicles, and as emerging applications such as energy storage and electrified commercial transport expand further, competition within the battery industry is expected to increasingly hinge on technological capability, cost control, and the ability to tailor products to specific mobility and energy scenarios rather than simply on scale alone.