Gasgoo Munich- 2025 has been anything but easy for foreign Tier 1 suppliers.

Annual reports are riddled with references to "declines" and "adjustments," while behind the scenes, companies are busy spinning off businesses, cutting jobs, and shifting R&D eastward. The days of steady growth fueled by brand premiums and China market dividends are fading, squeezed by the rise of local supply chains and the extreme compression of vehicle costs.

Yet, declaring that foreign Tier 1s are in crisis based solely on profit dips at a few firms would be premature. A closer look reveals that beneath the surface of industry-wide pressure, these players are demonstrating significant operational resilience and the tangible results of their transformation.

2025 Performance: The Pressure Is Real, but So Is the Resilience

Foreign Tier 1s certainly felt the squeeze in 2025. But a closer read of the financials reveals a narrative beyond the pressure: while some stumbled, others thrived. Legacy businesses contracted, but new ventures sprinted ahead.

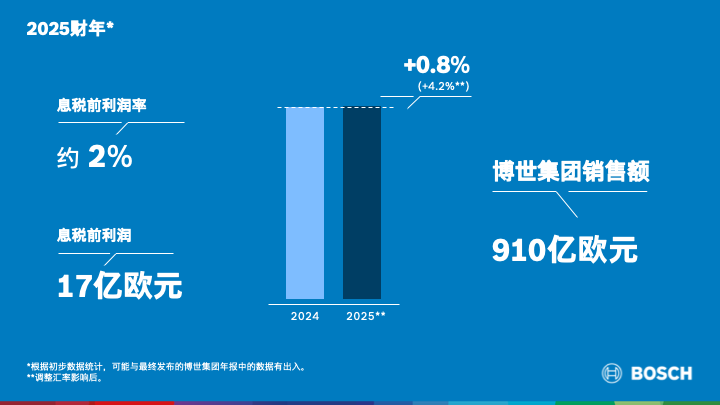

Bosch Group's sales edged up to 91 billion euros, yet its EBIT margin hovered around just 2%—down from 3.5% in 2024. Chairman Stefan Hartung described 2025 as a "difficult year," attributing the strain to a sluggish macroeconomy, intensifying competition, rising tariff costs, and heavy provisions booked for structural adjustments.

Image Source: Bosch

Magna's sales slipped 2% to $42 billion in 2025, but adjusted EBIT reached $2.4 billion, lifting margins by 20 basis points. Schaeffler posted sales of 23.49 billion euros—a 0.6% decline on a constant-currency basis against pro forma figures—while adjusted EBIT climbed 11.1% to 936 million euros.

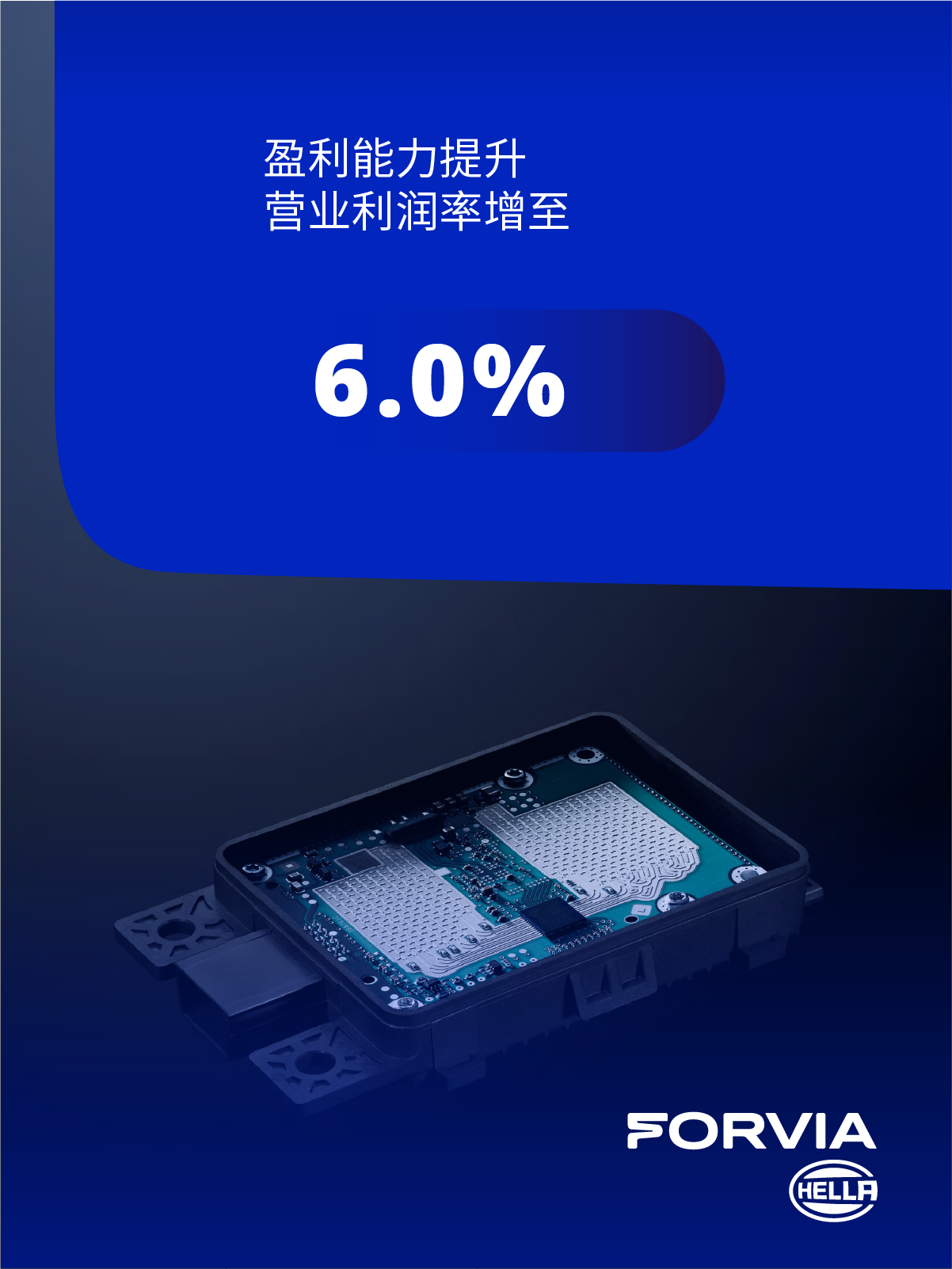

Valeo generated 20.9 billion euros in sales, with net profit jumping 23% to 200 million euros. Autoliv saw net sales rise from $10.39 billion to $10.82 billion, driving operating profit up 11.1% to $1.09 billion; its adjusted operating margin gained 60 basis points to hit 10.3%. OPmobility's revenue edged up 1.7% to 11.54 billion euros, stripping out currency effects, while operating profit grew 11.4% to 490 million euros. FORVIA HELLA reported currency-adjusted sales of 8 billion euros, flat year-over-year, with the operating margin expanding to 6%.

Image Source: FORVIA HELLA

These figures make one thing clear: despite broad headwinds, foreign Tier 1s retain deep reserves and operational grit. Even those missing profit targets held their revenue ground, defending turf in a volatile market—and holding the line is itself a form of resilience. More importantly, a significant number of players grew profits or improved margins under pressure, validating their ability to withstand stress and execute their turnarounds.

Structurally, the "China dividend" is normalizing—but that isn't necessarily bad. As one industry insider told Gasgoo: "Previously, high margins at these firms relied heavily on China's contribution. If a Tier 1's global average margin was 5% to 7%, China would often deliver 10% or more."

Yet, as local Chinese players surge in electronic architecture, automotive electronics, and software, competition has intensified. The fat profit margins foreign Tier 1s once enjoyed in China are being squeezed out.

In terms of business mix, electrification and smart technologies are emerging as new growth engines. In 2025, Schaeffler's e-mobility division grew 7% to 5.02 billion euros, securing 15.5 billion euros in new orders (8.8 billion for hybrids, 2 billion for pure electric drives). FORVIA HELLA's electronics division posted sales of 3.4 billion euros, up 4.5%, with the operating margin rising to 7.8%. Valeo's order book swelled 38% to 24.6 billion euros—accelerating to 47% in the second half—as it solidified its lead in software-defined vehicles and driver assistance. BorgWarner saw revenue from light-vehicle electrification products climb roughly 23%.

The data suggests that while the growing pains of transition are real, new businesses are already carrying half the load, building momentum for future growth.

Thus, 2025 for foreign Tier 1s is better viewed not as a decline, but as a healthy reset of profit and business structures. The pain is unavoidable, but the foundation remains, and fresh growth has already taken root.

Beneath the Surface: They Are Clearer-Eyed Than Imagined

If financial reports are the "face," strategic adjustments are the "body." And the body of foreign Tier 1s is far more solid than many assume.

In reality, strategic shifts didn't start in 2025. Facing waves of electrification and intelligence in recent years, these giants have long pursued a deep, adaptive restructuring. The 2025 financial results are simply the concentrated manifestation of those moves. The core of this adjustment can be summed up in three words: spin-offs, cost-cutting, and focus.

First is the spin-off—a strategic choice already underway or completed by several parts giants.

SKF is accelerating the divestment of its automotive business. By November 2025, it had transferred 50% of automotive sales, 70% of automotive bearing staff, and 70% of production channels. The plan is to list the auto unit under the SKF Vertevo brand in the fourth quarter of 2026, allowing the parent company to focus on high-margin industrial sectors like wind power and aviation.

Image Source: SKF

Aptiv has finalized the spin-off of its legacy Electrical Distribution System (EDS) business, planning to list it independently as Versigent in April 2026. Continental Group not only made its automotive parts business independent as "AUMOVIO" to focus on emerging areas like E/E architecture, but also sold ContiTech's OEM Solutions business. It is now pushing to sell ContiTech entirely (expected in 2026), ultimately transforming into a specialized enterprise anchored by its Continental tire brand.

Why are some giants slimming down? Zhou Xiaoying, CEO and Editor-in-Chief of Gasgoo, offers a sharp insight: "The business splits by international parts giants are essentially about realigning organizational structures with the pace of technology and the logic of competition amid the waves of electrification and intelligence."

She points out that today's parts giants often juggle three completely different business logics within one company: traditional manufacturing, which emphasizes scale and stable delivery; capital-intensive electrification with clear paths; and highly uncertain, long-cycle intelligent software businesses. "When technology, products, and business lines are already on different tracks—facing distinct ecosystems, competitive rhythms, and resource requirements—trying to carry them all with a single organizational structure makes conflict almost inevitable."

Spin-offs aren't a sign of weakness. They are about matching specialized businesses with specialized organizations, curing the resource drain and slow decision-making of big-company disease, all to run faster.

Next comes layoffs and the shedding of inefficient businesses—an active choice for "lean operations." By the end of 2025, Bosch Group's global workforce had shrunk by roughly 5,400 year-on-year, with about 6,500 cuts in Germany alone. In September 2025, Bosch announced an additional 13,000 job cuts in its automotive division, a process set to continue through 2030 and primarily affecting German staff.

One industry insider admitted frankly: "Right now, foreign Tier 1s are mainly cutting jobs in Europe and the U.S." Behind this lies a shift in the global auto industry's center of gravity: traditional markets in the West are flat and overcapacity-ridden, while the Asia-Pacific region—led by China—holds massive growth potential. Resources must be reallocated. Layoffs are not a retreat; they are a move to shift resources where the hope is.

Finally, and most importantly, there is a sustained tilt of R&D resources toward China. China is upgrading from a "profit center" for foreign Tier 1s to an "R&D center" and even an "innovation hub." The aforementioned insider noted that whether these firms have the boldness to place significant R&D and innovation resources in China will determine their future competitive standing.

Actions over the past two years suggest top players are answering "yes." By the end of 2025, Bosch employed roughly 57,000 people in China, with many core electrification and intelligence projects developed there—sometimes under a "developed in China, shared globally" model. Bosch Commercial Vehicles is progressing with a light e-drive base in Nanchang and a new steering plant in Jinan, while Bosch Comfort Tech is building a global R&D center in Wuxi and a high-end compressor base in Guangzhou. ZF has localized cutting-edge technologies like steer-by-wire and rear-wheel steering in China to deeply fit local market demands.

Schaeffler's push goes even deeper. While aggressively localizing existing businesses, it established an embodied intelligent robotics company in China. The goal is for revenue from high-growth fields like humanoid robots to account for 10% of total group revenue by 2035.

Image Source: Schaeffler

This posture of "voting with real money" speaks volumes about confidence in the China market and signals where the fulcrum of future growth lies.

2026: They Still Have Cards to Play

Standing at the threshold of 2026, foreign Tier 1s face a complex situation, but it is far from hopeless. On the contrary, they still hold plenty of cards.

Looking at corporate forecasts, while caution is widespread, most companies have set clear growth targets—often accompanied by optimistic signals.

Bosch projects global economic growth of 2.3% in 2026, with auto industry competition and price pressures intensifying further; the full impact of 2025 tariffs will hit for the first time. The company expects to hit its 7% margin target no earlier than 2027. Schaeffler is similarly cautious, forecasting 2026 sales of 22.5 billion to 24.5 billion euros—a year-on-year range of -4.3% to +4.3% on a constant-currency basis. It also anticipates an EBIT margin, excluding special items, of 3.5% to 5.5%.

Valeo has set a target to lift its 2026 operating margin to 4.7%-5.3%, with free cash flow exceeding 400 million euros; its latest innovations in software-defined vehicles and driver assistance will roll out with new model launches. Magna expects sales of $41.9 billion to $43.5 billion and free cash flow of $1.6 billion to $1.8 billion, with capital spending remaining below historical levels.

Visteon forecasts net sales of $3.63 billion to $3.83 billion and adjusted EBITDA of $455 million to $495 million, while raising its quarterly dividend by 36%. FORVIA HELLA expects sales of 7.4 billion to 7.9 billion euros, an operating margin of 5.4% to 6.0%, and net cash flow of at least 1.8% of sales. ON Semiconductor anticipates a gross margin of 37.4% to 39.4% for the first quarter of 2026.

Image Source: Visteon

OPmobility has set a 2026 goal to "comprehensively improve operating profit, net income, free cash flow, and net debt metrics compared to 2025." Gestamp stated it will continue to consolidate its financial position and strengthen its balance sheet, aiming to surpass current EBITDA margins.

These targets suggest that companies' internal views are far less pessimistic than outsiders might assume. Most still believe they can maintain stability—or even grow—amid the adjustments.

In terms of growth drivers, China remains a critical foundation, and those deeply rooted there will benefit first.

On one hand, companies that have completed the "R&D localization" upgrade are poised to seize a new round of structural opportunities in China. Bosch's new plants in Nanchang and Jinan are proceeding as planned, and its Wuxi R&D center is doubling down; the company plans to increase investment in autonomous driving and chassis in China through 2026 and explore robotics. ZF plans to achieve mass production of brake-by-wire technology in China in the second half of 2026. Valeo's battery cooling plates will enter mass production in 2026 to meet core NEV market demands, having secured major orders from leading Chinese startups. These layouts will gradually translate into market advantages in 2026, helping deep-rooted players navigate the cycle.

On the other hand, intensifying local competition has brought pressure, but it has also forced foreign Tier 1s to become more flexible and grounded. They have learned to bind themselves more tightly to the Chinese supply chain, respond faster to market demands, and define products closer to local users. This "forced evolution" may not be a bad thing in the long run; it could become the nutrient that sustains their global competitiveness.

Regarding risks, transition costs and the external environment are certainly tests, but they are not insurmountable. Bosch has devised a "combination punch" to lift margins, centering on "cost reduction and efficiency" and "innovation layout." This involves comprehensively optimizing material costs and deepening AI use to boost production efficiency, while continuously refining supply chains and production processes. OPmobility's localized industrial layout has already effectively mitigated the impact of tariffs.

These are "known unknowns," and companies are actively responding through spin-offs for efficiency, localization for cost reduction, and technological premiums—not by waiting passively.

All things considered, 2026 is more likely to be a "year of divergence" than a "year of collapse" for foreign Tier 1s. Leading companies that quickly reshaped their organizations, secured core technologies, and rooted themselves deeply in China are expected to hold their ground while moving toward "steady growth and profit restoration." Those slow to transform, wavering in strategy, or late to adjust their global layouts may face a longer period of adjustment pain.

But this is the normal logic of market competition—some fall behind, others lead, and survival of the fittest never stops.

![[Gasgoo Express] Ford and Geely Reach Agreement; Antolin Secures US Court Bankruptcy Protection](https://gascloud.gasgoo.com/production/2026/07/a3c8220e-382e-456f-a768-77cad93f17f1-1784991559.png)