Gasgoo Munich-Data from Gasgoo Automotive Research Institute indicates that China's passenger vehicle core components market remained steady through the first two months of 2026, with competitive landscapes varying across different segments. A clear pattern has emerged in air suspension, LiDAR, high-definition (HD) mapping, and HD positioning, where local companies now dominate. Top vendors hold absolute sway thanks to advantages in technology, production capacity, and cost. Conversely, driving ADAS, front-view cameras, and automated parking remain led by international giants, though domestic players are breaking through faster and gaining market share, signaling strong potential.

This landscape underscores a pivotal shift as China's auto industry enters a critical phase of deep integration between electrification and intelligence. The core components supply chain is accelerating toward self-reliance and technological autonomy. The rise of local suppliers alongside sustained efforts by global heavyweights is driving tech iteration and industrial upgrades. This not only solidifies the supply chain foundation for high-level intelligent connectivity in domestic passenger vehicles but also provides crucial data to understand the competitive dynamics and future trajectory of China's auto parts industry.

Air Suspension Supplier Installation Volume Rankings

Tuopu Group. From January to February 2026, air suspension installations in China's passenger vehicle market reached 75,362 units, securing a 34.1% market share.

KH Automotive Technologies. Installations totaled 71,017 units, representing a 32.1% market share.

Baolong Tech. With 58,779 units installed, the company captured 26.6% of the market.

Vibracoustic. Installations reached 7,124 units, accounting for 3.2% of the market.

AUMOVIO. The company recorded 5,680 units installed, holding a 2.6% share.

Others. Combined installations for other suppliers stood at 3,005 units, representing a 1.4% share.

From January to February 2026, China's air suspension market remained highly concentrated, with domestic brands continuing their ascent. Tuopu Group solidified its position as the industry leader with 75,362 units installed and a 34.1% share, leveraging its scaled production capabilities and integrated solutions. KH Automotive Technologies and Baolong Tech followed with 71,017 and 58,779 units respectively, claiming 32.1% and 26.6% market shares. Together, these three players command over 92% of the market, defining a stable hierarchy that dominates the domestic supply chain.

In contrast, suppliers like Vibracoustic and AUMOVIO hold smaller slices of the domestic pie, with 7,124 and 5,680 units respectively—combining for just a 5.8% share. Other suppliers collectively managed only 3,005 units, representing a mere 1.4%, making a breakout difficult. Overall, the localization trend in air suspension deepened through the first two months of 2026. Local firms, armed with cost controls, rapid response times, and fast tech iteration, are squeezing the space for foreign and smaller players, leaving the industry highly concentrated.

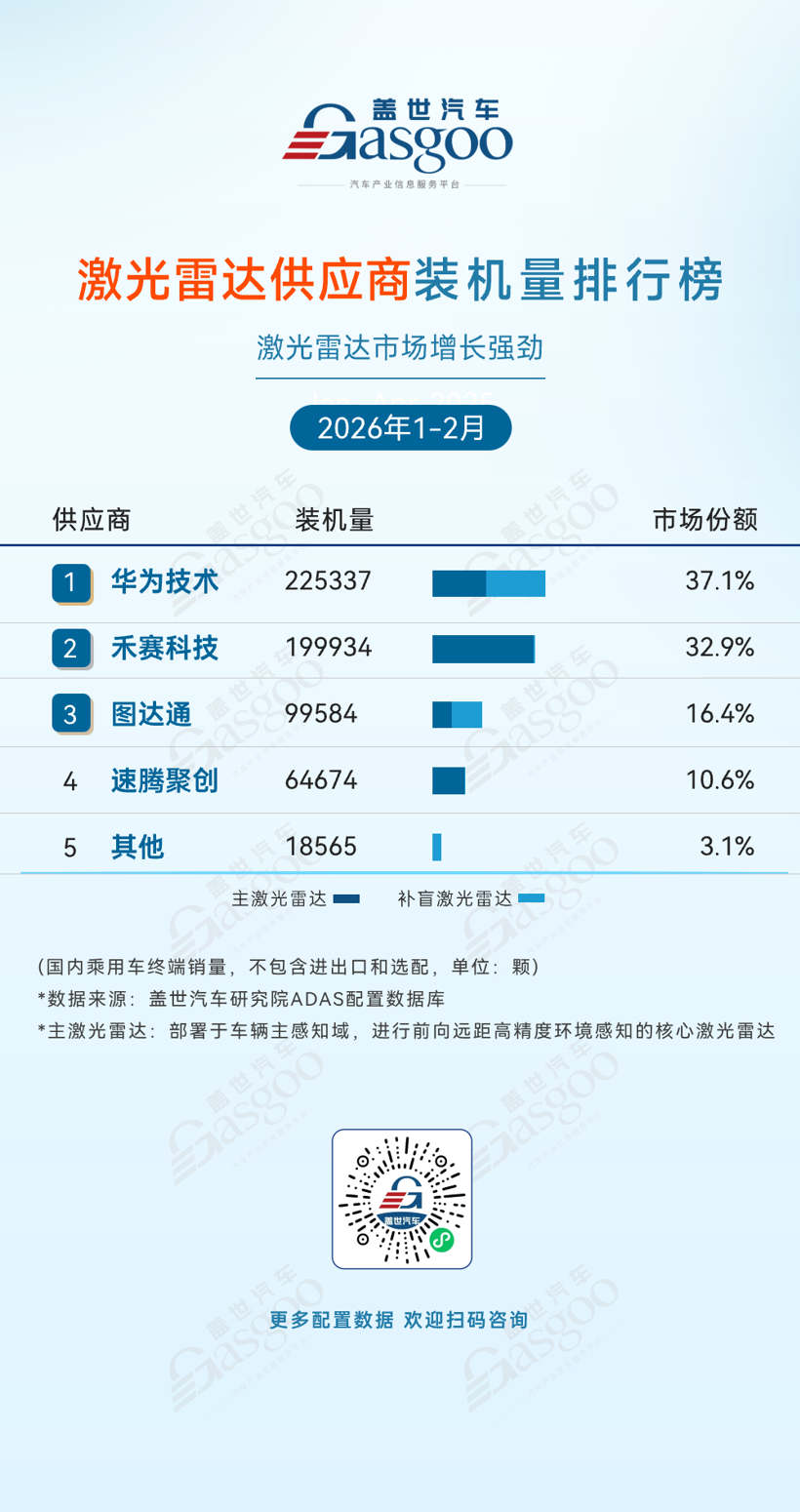

LiDAR Supplier Installation Volume Rankings

Huawei Technologies. Installations hit 225,337 units, grabbing a 37.1% market share.

Hesai Technology. The company posted 199,934 units installed, securing a 32.9% share.

Seyond. Installations reached 99,584 units, accounting for 16.4% of the market.

RoboSense. With 64,674 units installed, the firm held a 10.6% share.

Others. Other suppliers recorded 18,565 units installed, representing a 3.1% share.

China's LiDAR market saw robust growth in the first two months of 2026, maintaining a pattern where local players lead a highly concentrated field. Huawei Technologies held the top spot with a 37.1% share and 225,337 units installed, favored by automakers for its precision, cost control, and automotive-grade reliability. Hesai Technology followed closely with a 32.9% share. Together, these two local giants control 70% of the market, setting the competitive tone.

Seyond and RoboSense took third and fourth with 16.4% and 10.6% respectively, rounding out the core domestic supplier matrix. Notably, both Huawei and Seyond are leveraging a dual strategy of main and blind-spot LiDAR to expand their footprint. Domestic firms are consolidating their dominance through tech upgrades and capacity advantages, driving higher penetration rates for LiDAR in smart vehicles.

Driving ADAS Supplier Installation Volume Rankings

Bosch. Installations totaled 274,026 units, capturing a 13.9% market share.

Denso. The company recorded 204,643 units installed, representing a 10.4% share.

ZF. Installations reached 182,726 units, good for a 9.3% share.

Freetech. With 131,873 units installed, the company held a 6.7% share.

Valeo. Installations stood at 117,831 units, accounting for 6.0% of the market.

Huawei. The tech giant posted 109,275 units installed, securing a 5.5% share.

BYD. Installations reached 106,288 units, representing a 5.4% share.

Aptiv. The company recorded 73,752 units installed, holding a 3.7% share.

Jingwei Hirain. Installations totaled 62,633 units, with a 3.2% market share.

Momenta. With 59,395 units installed, the firm captured a 3.0% share.

From January to February 2026, the driving ADAS market remained a domain led by international giants, though domestic suppliers continued to chip away at their share. Bosch stayed in first with a 13.9% share and 274,026 units, its proven reliability keeping it a top choice for many automakers. Denso and ZF followed with 10.4% and 9.3% respectively, joining Bosch in the top tier.

Domestic players like Freetech, Huawei, and BYD crashed the upper ranks: Freetech took fourth with 6.7%, while Huawei and BYD landed in sixth and seventh with 5.5% and 5.4% respectively. Local suppliers Jingwei Hirain and Momenta also broke into the top ten with 3.2% and 3.0% shares, highlighting the strength of domestic firms in algorithm iteration, vertical integration, and market responsiveness. Through differentiated strategies, local suppliers are steadily gaining share, pushing the ADAS supply chain toward greater autonomy and self-reliance.

Front-view Camera Supplier Installation Volume Rankings

Bosch. Installations reached 275,060 units, commanding a 14.9% market share.

Denso. The company recorded 204,842 units installed, representing an 11.1% share.

ZF. With 183,813 units installed, the firm held a 10.0% share.

Sunny Smartlead. Installations totaled 180,520 units, good for a 9.8% share.

Freetech. The company posted 116,496 units installed, securing a 6.3% share.

Valeo. Installations stood at 116,020 units, accounting for 6.3% of the market.

O-film. With 98,120 units installed, the company held a 5.3% share.

Veoneer. Installations reached 78,867 units, representing a 4.3% share.

BYD Semiconductor. The firm recorded 76,103 units installed, capturing a 4.1% share.

Aptiv. Installations totaled 74,491 units, with a 4.0% market share.

In the first two months of 2026, the front-view camera market followed a similar script: international leaders at the front, domestic firms rising fast. Bosch led with a 14.9% share and 275,060 units, its deep tech reserves and global reach keeping it the industry benchmark. Denso and ZF followed with 11.1% and 10.0% respectively. Together with Bosch, this trio controls 36.0% of the market.

Sunny Smartlead took fourth with a 9.8% share, emerging as the leader among domestic brands and showcasing breakthroughs in optical perception and capacity. Freetech, O-film, and BYD Semiconductor also secured spots in the top ten with 6.3%, 5.3%, and 4.1% shares respectively. Leveraging cost efficiency, algorithm updates, and scenario adaptability, these firms have become core choices for many automakers, challenging the established order. Domestic suppliers are steadily boosting their influence in high-end perception hardware.

Automated Parking Assist (APA) Supplier Installation Volume Rankings

Bosch. Installations totaled 191,276 units, capturing an 18.8% market share.

Huawei. The company recorded 109,275 units installed, representing a 10.7% share.

BYD. With 107,473 units installed, the firm held a 10.5% share.

Valeo. Installations reached 68,271 units, good for a 6.7% share.

Xiaomi. The company posted 59,341 units installed, securing a 5.8% share.

Momenta. Installations stood at 57,475 units, accounting for 5.6% of the market.

Li Auto. With 53,450 units installed, the company held a 5.2% share.

NIO. Installations totaled 50,707 units, representing a 5.0% share.

AFARIg. The firm recorded 37,738 units installed, capturing a 3.7% share.

Leapmotor. Installations reached 37,150 units, with a 3.6% market share.

From January to February 2026, the APA market saw international giants lead, but domestic players continued their steady climb. Bosch held the top spot with 191,276 units and an 18.8% share. Huawei and BYD followed closely with 10.7% and 10.5% respectively, signaling the strong competitiveness of local firms in intelligent parking.

Xiaomi, Momenta, Li Auto, NIO, Qianxi, and Leapmotor also made the list, leveraging advantages in algorithms, scenario coverage, and user experience to challenge giants like Bosch and Valeo. Competition in APA has shifted from mere functionality to a comprehensive battle over scenario coverage, user experience, and algorithm iteration. The rise of domestic firms is driving new breakthroughs in technical autonomy and ecosystem building.

High-Definition Map Supplier Installation Volume Rankings

Amap. Installations reached 149,509 units, commanding a 43.8% market share.

Tencent. The company recorded 50,707 units installed, representing a 14.9% share.

Langge Technology. With 50,284 units installed, the firm held a 14.7% share.

NavInfo. Installations totaled 30,759 units, good for a 9.0% share.

Others. Combined installations for other suppliers stood at 60,116 units, holding a 17.6% share.

In the first two months of 2026, China's HD map market remained dominated by local players, with Amap continuing to lead. Amap controlled 43.8% of the market with 149,509 units installed, favored for its data precision, update frequency, and automotive-grade compatibility. Tencent, Langge Technology, and NavInfo followed in second through fourth with 14.9%, 14.7%, and 9.0% shares respectively, engaging in differentiated competition. Other suppliers collectively held 17.6%, indicating there is still room for smaller players in the market's long tail.

High-Precision Positioning Supplier Installation Volume Rankings

Ascent. Installations totaled 209,118 units, capturing a 31.7% market share.

Huawei. The company recorded 109,167 units installed, representing a 16.6% share.

Huace Navigation. With 59,342 units installed, the firm held a 9.0% share.

MCT. Installations reached 45,012 units, accounting for 6.8% of the market.

GEESPACE. The company posted 43,760 units installed, securing a 6.6% share.

Others. Combined installations for other suppliers stood at 192,947 units, holding a 29.3% share.

From January to February 2026, the high-precision positioning market accelerated the adoption of integrated solutions, with local firms firmly in charge. Ascent led with a 31.7% share and 209,118 units, demonstrating scale and deep customer coverage in automotive-grade positioning. Huawei, Huace Navigation, MCT, and GEESPACE followed, carving out niches in various scenarios with strengths in fusion algorithms, multi-source perception, and reliability. Other suppliers held a combined 29.3%, suggesting the market retains a diverse supply structure that leaves room for new entrants and specialized tech routes.

Ultimately, the battle in high-precision positioning has moved beyond simple accuracy contests to a complex mix of multi-source fusion, scenario adaptation, and ecosystem building. Local leaders are pushing the industry toward new breakthroughs in technical autonomy and practical application.

![[Gasgoo Express] Ford and Geely Reach Agreement; Antolin Secures US Court Bankruptcy Protection](https://gascloud.gasgoo.com/production/2026/07/a3c8220e-382e-456f-a768-77cad93f17f1-1784991559.png)