According to data compiled by the Gasgoo Automotive Research Institute, in 2025, China's NEV electrification core segments entered large-scale adoption with rising market concentration. Companies' self-supply, third-party support, and integration approaches show clear differences, providing key insights into the industry's competitive landscape and technology trends.

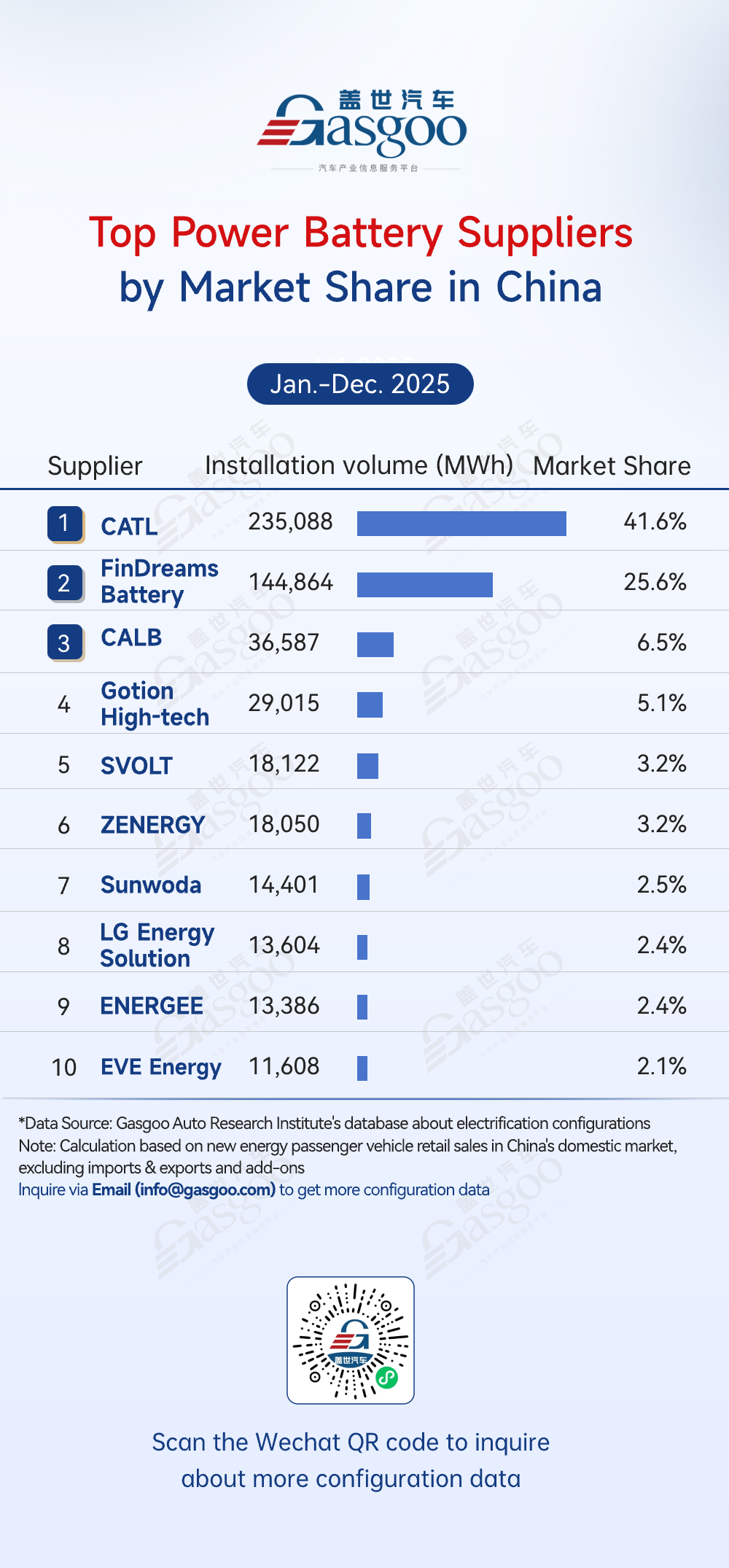

Top power battery suppliers

CATL: 235,088 MWh installed, 41.6% market share

FinDreams Battery: 144,864 MWh installed, 25.6% market share

CALB: 36,587 MWh installed, 6.5% market share

Gotion High-tech: 29,015 MWh installed, 5.1% market share

SVOLT: 18,122 MWh installed, 3.2% market share

ZENERGY: 18,050 MWh installed, 3.2% market share

Sunwoda: 14,401 MWh installed, 2.5% market share

LG Energy Solution: 13,604 MWh installed, 2.4% market share

ENERGEE: 13,386 MWh installed, 2.4% market share

EVE Energy: 11,608 MWh installed, 2.1% market share

From January to December 2025, China's power battery market was highly concentrated and dominated by a dual-oligopoly. The top 5 suppliers accounted for 82% of installations. CATL led the pack with 41.6% (235,088 MWh), supported by its scale, technology, and global capabilities. FinDreams Battery followed with 25.6% (144,864 MWh), leveraging its vertical integration with BYD. Other local players like CALB, Gotion High-tech, and SVOLT competed behind them, while global suppliers such as LG Energy Solution saw their share shrink, underscoring the local supply chain's cost and responsiveness advantages.

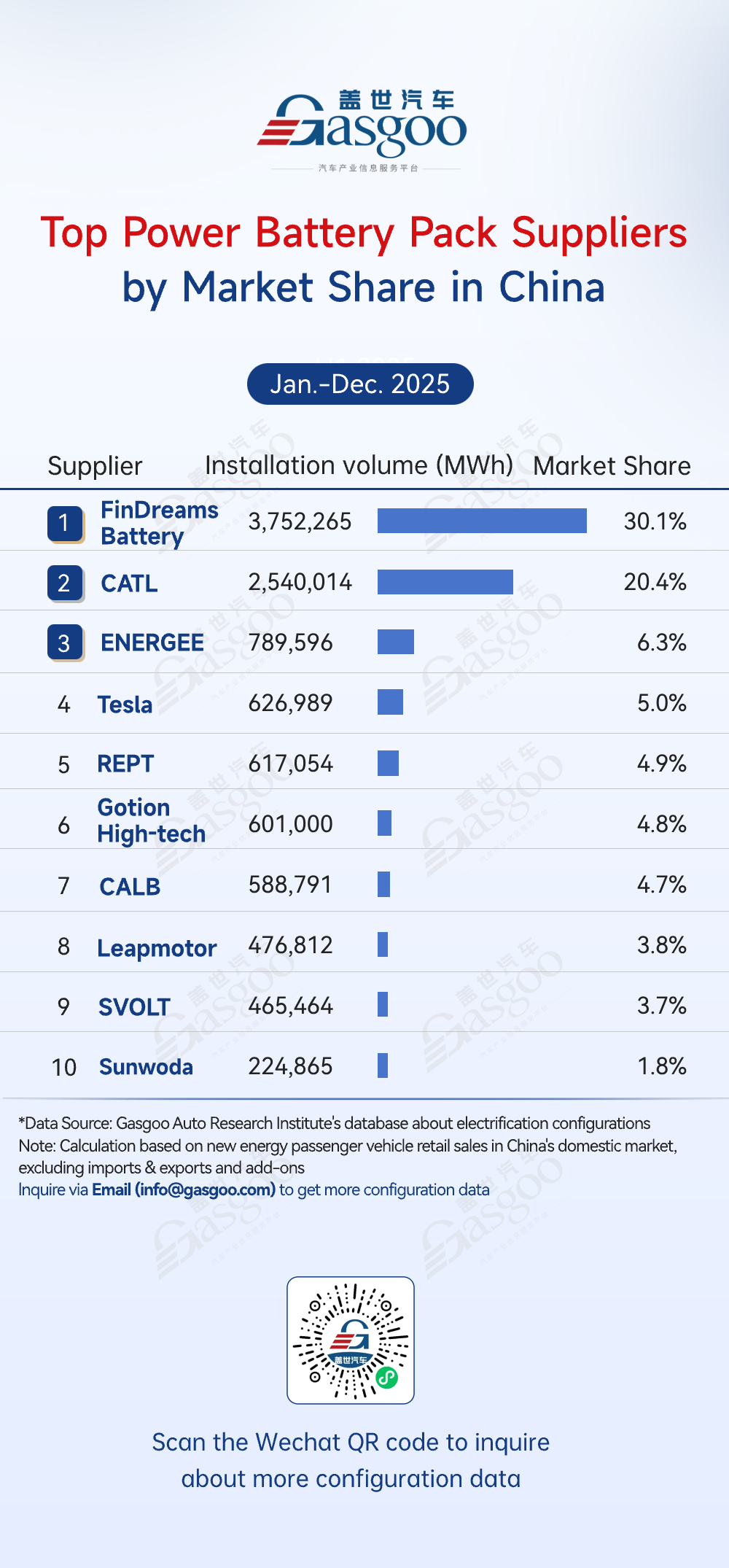

Top power battery pack suppliers

FinDreams Battery: 3,752,265 sets installed, 30.1% market share

CATL: 2,540,014 sets installed, 20.4% market share

ENERGEE: 789,596 sets installed, 6.3% market share

Tesla: 626,989 sets installed, 5.0% market share

REPT: 617,054 sets installed, 4.9% market share

Gotion High-tech: 601,000 sets installed, 4.8% market share

CALB: 588,791 sets installed, 4.7% market share

Leapmotor: 476,812 sets installed, 3.8% market share

SVOLT: 465,464 sets installed, 3.7% market share

Sunwoda: 224,865 sets installed, 1.8% market share

From January to December 2025, China's power battery pack market was dominated by automaker in-house production and concentrated top suppliers. FinDreams Battery led the pack with 3,752,265 sets installed (30.1% share), driven by BYD's vertical integration, enabling fully customized packs for its own models and a highly efficient supply chain. CATL followed with 20.3% (2,535,387 sets), providing standardized pack solutions to many mainstream automakers. Tesla, Leapmotor, and other automakers reflect the trend of leading companies accelerating vertical integration to control core technology and reduce costs. Other players like REPT and CALB steadily grew in niche segments, forming a competitive structure of "dual leaders + automaker in-house + second-tier supplements."

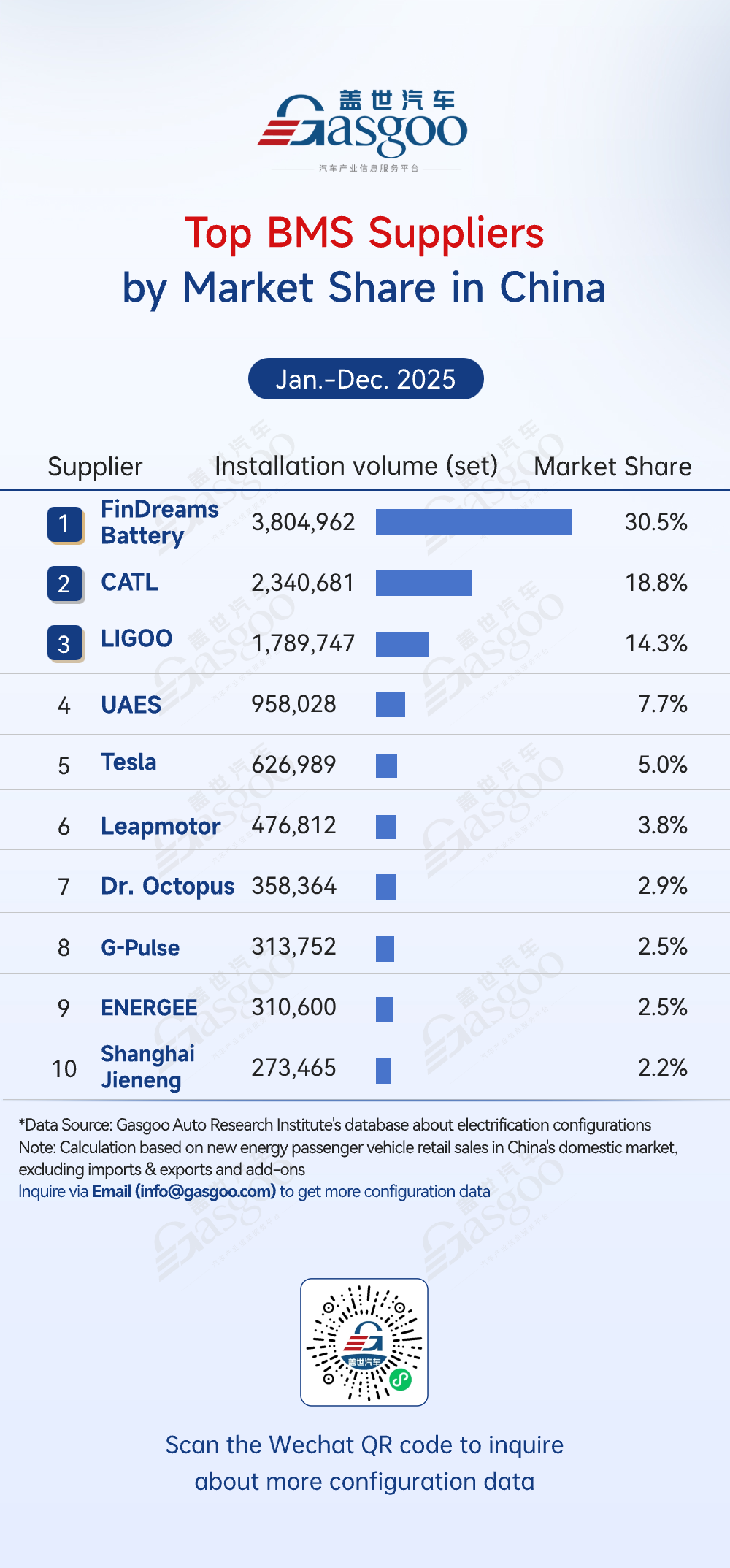

Top BMS suppliers

FinDreams Battery: 3,804,962 sets installed, 30.5% market share

CATL: 2,340,681 sets installed, 18.8% market share

LIGOO: 1,789,747 sets installed, 14.3% market share

UAES: 958,028 sets installed, 7.7% market share

Tesla: 626,989 sets installed, 5.0% market share

Leapmotor: 476,812 sets installed, 3.8% market share

Dr. Octopus: 358,364 sets installed, 2.9% market share

G-Pulse: 313,752 sets installed, 2.5% market share

ENERGEE: 310,600 sets installed, 2.5% market share

Shanghai Jieneng: 273,465 sets installed, 2.2% market share

From January to December 2025, China's BMS market was characterized by vertical integration, accelerated self-controllability, and clear concentration among top players. FinDreams Battery led the pack with 3,804,962 sets installed (30.5% share), driven by BYD's full-chain BMS deployment, enabling deep integration with its own models and efficient battery management. CATL followed with 18.7%, serving as a core supplier to many automakers with its mature solutions. LIGOO ranked third with 14.4%, reflecting its technical strength in third-party BMS. The presence of Tesla, Leapmotor, and Shanghai Jieneng on the list underscores the clear trend of automakers pursuing self-controllable BMS solutions.

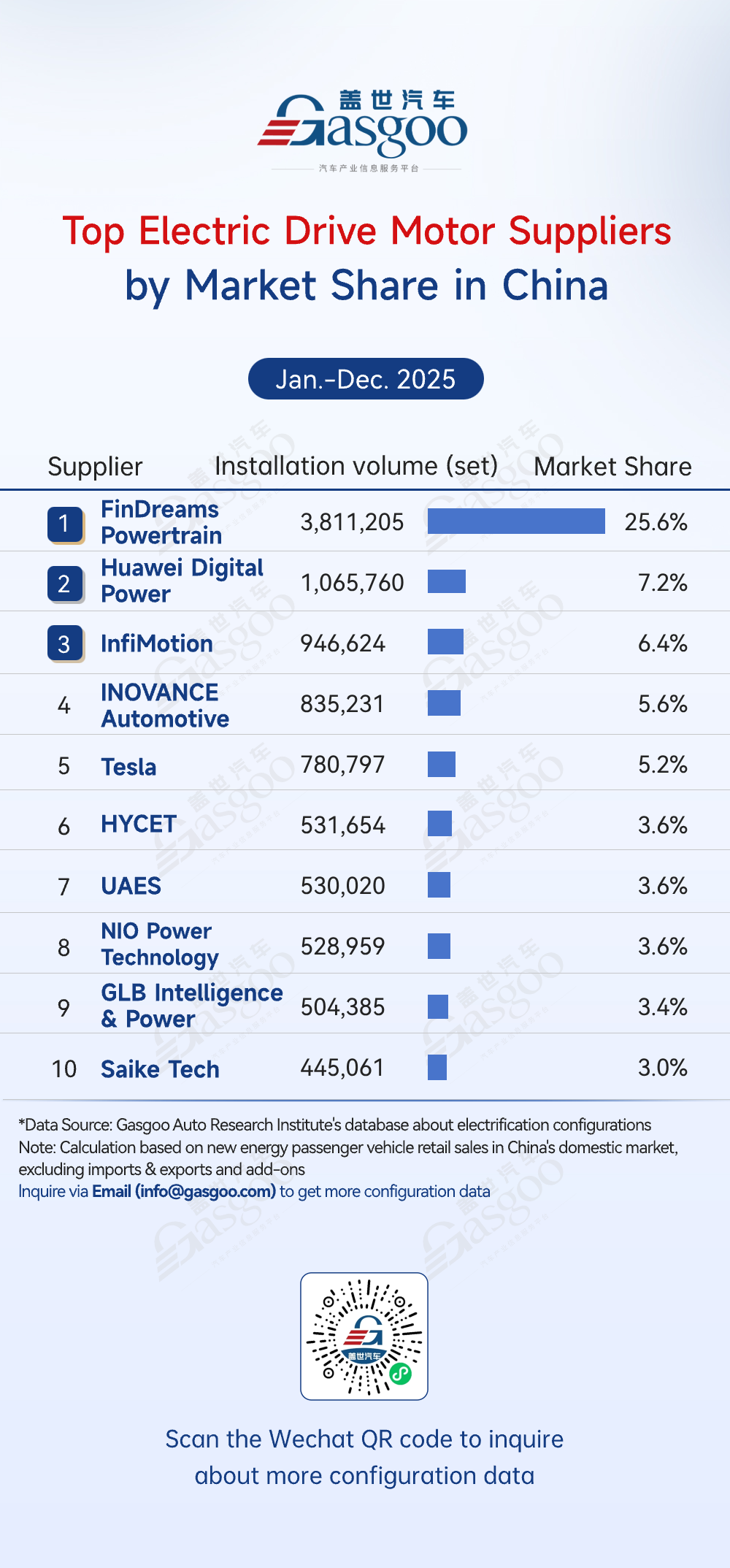

Top electric drive motor suppliers

FinDreams Powertrain: 3,811,205 sets installed, 25.6% market share

Huawei Digital Power: 1,065,760 sets installed, 7.2% market share

InfiMotion: 946,624 sets installed, 6.4% market share

INOVANCE Automotive: 835,231 sets installed, 5.6% market share

Tesla: 780,797 sets installed, 5.2% market share

HYCET: 531,654 sets installed, 3.6% market share

UAES: 530,020 sets installed, 3.6% market share

NIO Power Technology: 528,959 sets installed, 3.6% market share

GLB Intelligence & Power: 504,385 sets installed, 3.4% market share

Saike Tech: 445,061 sets installed, 3.0% market share

From January to December 2025, China's electric drive motor market was led by FinDreams Powertrain, Huawei Digital Power, and InfiMotion. FinDreams Powertrain held 25.6% (3,811,205 sets), benefiting from BYD's vertical integration and strong scale advantages. Huawei, InfiMotion, and INOVANCE Automotive expanded through motor efficiency and system integration expertise. Tesla and NIO Power Technology's in-house systems also ranked high, highlighting differentiated competition and driving industry upgrades.

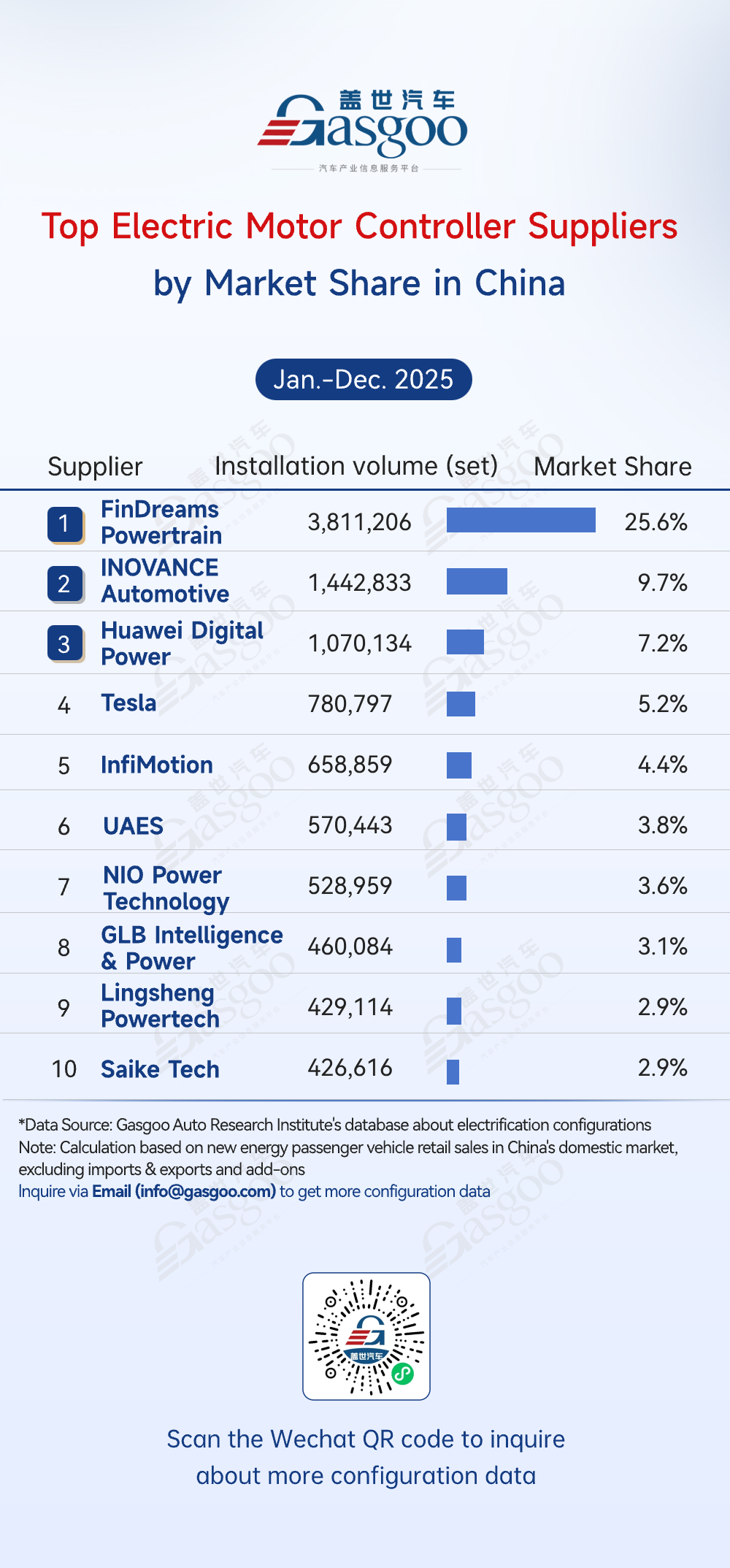

Top electric motor controller suppliers

FinDreams Powertrain: 3,811,206 sets installed, 25.6% market share

INOVANCE Automotive: 1,442,833 sets installed, 9.7% market share

Huawei Digital Power: 1,070,134 sets installed, 7.2% market share

Tesla: 780,797 sets installed, 5.2% market share

InfiMotion: 658,859 sets installed, 4.4% market share

UAES: 570,443 sets installed, 3.8% market share

NIO Power Technology: 528,959 sets installed, 3.6% market share

GLB Intelligence & Power: 460,084 sets installed, 3.1% market share

Lingsheng Powertech: 429,114 sets installed, 2.9% market share

Saike Tech: 426,616 sets installed, 2.9% market share

From January to December 2025, automaker-produced electric motor controllers accounted for a large share, reflecting the trend of OEMs strengthening self-controllability in core electronics. FinDreams Powertrain took the lead with 25.6% (3,811,206 sets), benefiting from BYD's vertical integration across vehicles, motors, and controllers, ensuring deep platform alignment and advantages in scale and cost. INOVANCE Automotive and Huawei Digital Power formed the second tier, showing strong third-party capabilities. Tesla and NIO Power Technology's in-house systems also ranked high, creating a parallel market structure and driving differentiated competition and ongoing motor controller technology iteration.

Top suppliers of power semiconductor device (dedicated to e-drive)

BYD Semiconductor: 3,805,877 sets installed, 25.6% market share

CRRC Times Semiconductor: 1,859,795 sets installed, 12.5% market share

Silan Microelectronics: 1,286,511 sets installed, 8.6% market share

United Nova Technology: 1,277,020 sets installed, 8.6% market share

Infineon: 1,026,646 sets installed, 6.9% market share

STMicroelectronics: 799,922 sets installed, 5.4% market share

UAES: 783,953 sets installed, 5.3% market share

StarPower Semiconductor: 721,189 sets installed, 4.8% market share

Leadrive: 648,693 sets installed, 4.4% market share

GEENER: 222,905 sets installed, 1.5% market share

From January to December 2025, China's power semiconductor device (dedicated to e-drive) market was dominated by local players, highly concentrated, with accelerated domestic substitution. The top five suppliers accounted for 62% of installations. BYD Semiconductor led the pack with 25.6% (3,805,877 sets). Local companies such as CRRC Times Semiconductor, Silan Microelectronics, and United Nova Technology followed, leveraging advantages in technology iteration, production scale, and cost control to gain market share. Global players like Infineon (6.9%) and STMicroelectronics (5.4%) remained important but faced shrinking space, highlighting the rise of China's local power devices in automotive-grade applications.

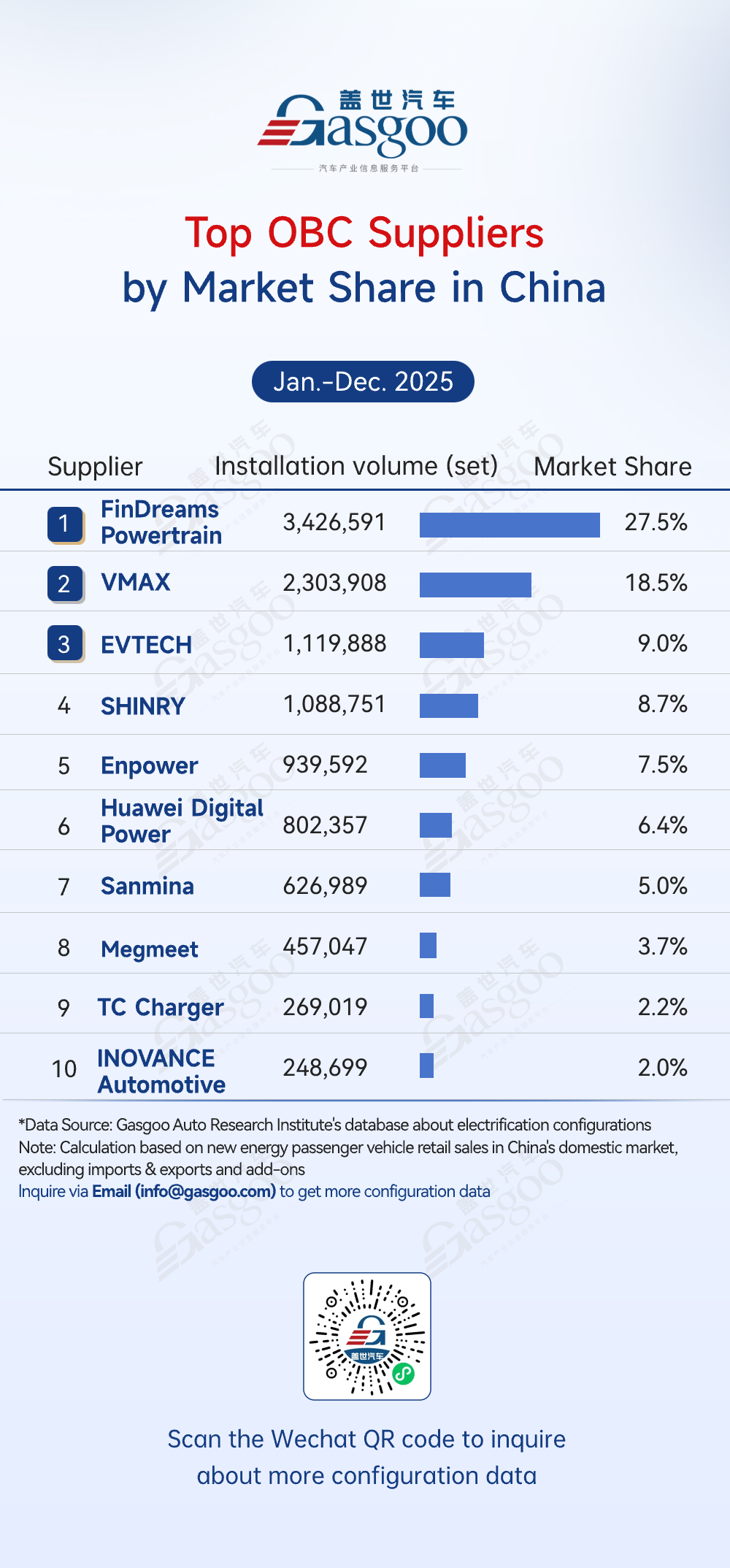

Top OBC suppliers

FinDreams Powertrain: 3,426,591 sets installed, 27.5% market share

VMAX: 2,303,908 sets installed, 18.5% market share

EVTECH: 1,119,888 sets installed, 9.0% market share

SHINRY: 1,088,751 sets installed, 8.7% market share

Enpower: 939,592 sets installed, 7.5% market share

Huawei Digital Power: 802,357 sets installed, 6.4% market share

Sanmina: 626,989 sets installed, 5.0% market share

Megmeet: 457,047 sets installed, 3.7% market share

TC Charger: 269,019 sets installed, 2.2% market share

INOVANCE Automotive: 248,699 sets installed, 2.0% market share

From January to December 2025, China's OBC market was highly concentrated, led by local players with clear technological differentiation. FinDreams Powertrain ranked first with 27.5% (3,426,591 sets), benefiting from BYD's vertically integrated supply chain and deep model-specific adaptation. VMAX followed with 18.5%, providing mature third-party solutions to multiple mainstream automakers. The top 5 suppliers together accounted for over 70%, reflecting accelerating market concentration, while companies like EVTECH and SHINRY Technology steadily grew in niche segments, demonstrating local supply chain strengths in technology and capacity.

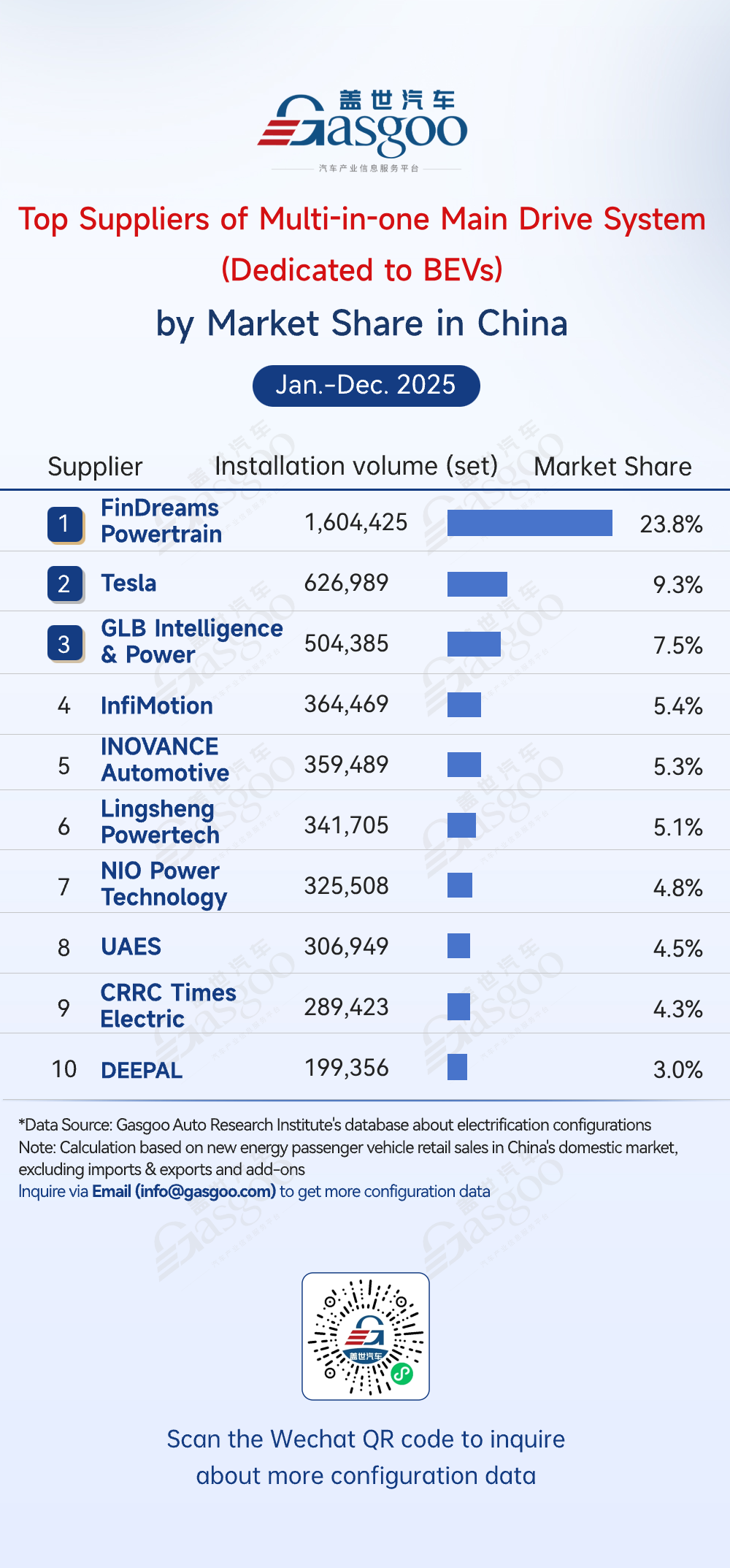

Top suppliers of multi-in-one main drive system (dedicated to BEVs)

FinDreams Powertrain: 1,604,425 sets installed, 23.8% market share

Tesla: 626,989 sets installed, 9.3% market share

GLB Intelligence & Power: 504,385 sets installed, 7.5% market share

InfiMotion: 364,469 sets installed, 5.4% market share

INOVANCE Automotive: 359,489 sets installed, 5.3% market share

Lingsheng Powertech: 341,705 sets installed, 5.1% market share

NIO Power Technology: 325,508 sets installed, 4.8% market share

UAES: 306,949 sets installed, 4.5% market share

CRRC Times Electric: 289,423 sets installed, 4.3% market share

DEEPAL: 199,356 sets installed, 3.0% market share

In 2025, China's multi-in-one main drive system (dedicated to BEVs) market was dominated by automakers' in-house solutions, with high concentration among top suppliers. FinDreams Powertrain led with 23.8% (1,604,425 sets), leveraging BYD's vertical integration for advantages in system integration, cost efficiency, and large-scale deployment. Tesla followed with 9.3%, maintaining strong competitiveness through continuous iteration of its self-developed electric drive system. Meanwhile, specialized suppliers such as GLB Intelligence & Power, InfiMotion, and INOVANCE Automotive entered the top tier, gaining market share through differentiated strengths in customized development.

Top electrical compressor suppliers

FinDreams Technology: 3,238,799 sets installed, 26.0% market share

Sanden Hasco: 2,226,532 sets installed, 17.9% market share

Aotecar: 1,628,581 sets installed, 13.1% market share

Welling: 1,084,465 sets installed, 8.7% market share

Highly: 961,261 sets installed, 7.7% market share

ZonCen New Energy: 913,415 sets installed, 7.3% market share

Chongqing Chaoli High-Tech: 318,367 sets installed, 2.6% market share

SANDEN: 313,495 sets installed, 2.5% market share

Hanon Systems: 282,475 sets installed, 2.3% market share

DENSO: 228,263 sets installed, 1.8% market share

From January to December 2025, China's electrical compressor market was highly concentrated, dominated by local players with clear technological differentiation. FinDreams Technology led the pack with 26.0% (3,238,799 sets), benefiting from BYD's vertically integrated supply chain. Sanden Hasco, Aotecar, and other China's local companies followed, with the top five suppliers accounting for 73%, reflecting accelerating market concentration. Welling and Highly steadily grew in niche segments, showcasing local strengths in technology and capacity, while international giant DENSO ranked tenth with just 1.8%, highlighting the competitive edge of Chinese players in cost control and responsiveness.