Gasgoo Munich- It would seem that the broader auto industry's profit margin slump has little to do with listed automakers.

In 2025, China’s auto sector remained trapped in a dilemma of rising volume but stagnant profits. The industry’s profit margin for the full year slumped to a low of 4.1%, well below the 5.9% average for industrial enterprises. Cui Dongshu, secretary-general of the CPCA, has repeatedly warned that the sector must guard against the erosion of long-term health by price wars to avoid falling into a vicious cycle.

Yet, a shift in focus to listed automakers that have released their 2025 financial reports reveals that top players retain formidable earning power. Even startups that have long bled red ink collectively swung to profitability in the fourth quarter. A clear trend is emerging: leading listed automakers are building their own “safe havens” backed by scale, technology, and globalization.

14 Automakers, 80% Profitable

Among the 14 mainstream automakers tracked by Gasgoo, 11 posted positive profits. But a deeper analysis shows few saw profit growth outpace revenue growth. The more common scenario was rising revenue with net profit treading water—or even retreating.

The reasons are straightforward. First, R&D spending remains high during the energy transition, with most companies seeing research costs rise faster than revenue. Second, persistent domestic price competition is squeezing vehicle gross margins. While sales volumes are expanding, per-vehicle profitability isn’t keeping pace.

BYD continued to lead with 804.0 billion yuan in revenue and 32.6 billion yuan in net profit attributable to shareholders. However, intensifying competition and heavy R&D investment of 63.4 billion yuan drove net profit down 19% year-on-year. Notably, BYD’s pure electric vehicle sales of 2.2567 million units surpassed Tesla for the first time, making it the 2025 global champion—a feat fueled by a strategy of “trading profit for scale.”

Dong Jing, an analyst at the Gasgoo Automotive Research Institute, noted that BYD has built unmatched dual advantages in cost and technology through vertical integration across batteries, electric drives, and automotive-grade chips. This gives it immense resilience against cyclical fluctuations and high certainty for growth.

Geely Auto showed similar characteristics. In 2025, revenue reached 345.2 billion yuan, up 25.1% year-on-year. Yet attributable net profit was 16.85 billion yuan, edging up just 0.24%. Soaring R&D costs, which jumped nearly 30%, were the primary factor suppressing profit growth.

Seres reported revenue of 165.05 billion yuan, a 13.7% increase, but attributable net profit of 5.96 billion yuan—roughly flat with the previous year—signaling a clear slowdown in profit growth.

Chery and Voyah emerged as “new faces” in this earnings cycle. Chery’s full-year revenue hit 300.3 billion yuan with a net profit of 19.0 billion yuan, second only to BYD. Its 13.8% gross margin sits in the upper-middle tier among traditional automakers. Voyah, meanwhile, generated 34.86 billion yuan in revenue—up over 80%—and turned a profit of 1.02 billion yuan, successfully reversing losses with a gross margin of 20.9%.

Great Wall Motor took a steadier path. Its 2025 revenue came in at 222.8 billion yuan, up 10.2%, while gross margins held firm at a high 18%. The market has recognized the stability brought by its optimized product mix.

Among state-owned automakers, SAIC Motor saw net profit reach 10.1 billion yuan—a 506.5% surge—signaling a significant improvement in operations after deep reforms. GAC Group, however, faced intense pressure with a net loss of about 8.8 billion yuan—an 11-fold plunge—as sales shrank to 1.72 million units. Still, from the second quarter onward, it achieved three consecutive quarters of sequential sales growth, suggesting its transition is gaining traction.

Structurally, the profit divergence in 2025 took on a clear “dumbbell” shape. Top-tier players leveraged cost dilution and global premiums to defend their base, while some startups turned profitable through efficiency gains. Caught in the middle, companies lacking sufficient scale or differentiation faced the squeeze.

Beyond Selling Cars: Where Else Can Growth Come From?

Dissecting 2025 revenue structures reveals a trend: the model of relying solely on domestic vehicle sales for profit is fading, while the importance of diversified income is rising sharply. This diversification is evident in three main directions.

One direction is the expanding contribution of overseas markets. Compared to the fierce price competition at home, foreign markets still offer room in pricing and brand premiums. BYD is a case in point: its overseas business gross margin hit 19.5%, nearly 3 percentage points higher than domestic operations, with export sales accounting for 23% of the total.

Other automakers are seeing their global strategies pay off. Great Wall’s overseas sales made up about 38% of the total, effectively offsetting the erosion from domestic price wars. SAIC generated 152.1 billion yuan in overseas revenue, or roughly 23%, while Geely’s foreign income reached 73.92 billion yuan, accounting for 21%.

Chery stands out for its globalization. In 2025, overseas revenue hit 157.42 billion yuan—52% of total revenue—meaning foreign sales have surpassed domestic ones to become the dominant income source.

A second direction comes from non-vehicle businesses. BYD’s mobile components, assembly, and other products generated 150.2 billion yuan in revenue, nearly 20% of the total. This not only dilutes vehicle R&D costs but also creates synergies in areas like energy storage.

Technology licensing is also showing financial value. XPENG’s service and other income reached 8.34 billion yuan, or 11% of total revenue. Notably, its technical partnership with Volkswagen brought in direct cash flow with a profit margin of 68.2%—far above the 12.8% margin on vehicle sales—becoming a key variable in improving overall profitability. XPENG has preliminarily validated the feasibility of the “technology supplier” business model.

As a major shareholder in Huawei’s Yinwang, Seres stands to gain sustained investment returns and priority access to intelligent driving technologies as the scale of Qiankun-equipped models expands.

The significance of diversifying goes beyond padding current profits. With the industry consensus that selling cars is becoming less profitable, high-margin, high-growth non-automotive businesses have become crucial tools for automakers to smooth cyclical volatility and improve their earnings structure.

This explains why more automakers are actively moving into robotics and the low-altitude economy. Seres, for instance, mentioned intelligent robotics repeatedly in its annual report. Li Auto is developing its own Mach 100 chip and expanding into embodied intelligence, while XPENG holds stakes in low-altitude economy and humanoid robot ventures. These moves are natural extensions of technical capability and help win favor in capital markets.

A Turning Point for Startup Profitability

2025 marked a pivotal moment for startups. NIO and XPENG, the two leaders, both turned profitable in the fourth quarter, significantly narrowing their annual losses. Leapmotor went even further, achieving full-year profitability. Though their paths and performance vary, the signal is clear: the sector has collectively swung into the black.

Among the four startups, Leapmotor shone brightest. Revenue surged 101% year-on-year to 64.7 billion yuan, with attributable net profit of 538 million yuan—making it only the second startup after Li Auto to achieve a full-year profit. This corresponded with 597,000 deliveries, up 103.1%, securing its position as the sales leader among new players.

Leapmotor’s success stems from an extreme value-for-money strategy. By positioning its B and C series in the 80,000 to 200,000 yuan price bracket, it lifted its comprehensive gross margin to 15%. With cash on hand reaching 37.9 billion yuan, the company has generated positive operating cash flow for two straight years.

Dong Jing commented that Leapmotor’s “full-domain self-research” advantage has created industry-leading cost control. With a 2026 sales target of 1.05 million vehicles and a technology licensing model opening a second growth curve, the company is poised for a dual breakthrough in sales volume and profitability.

XPENG posted a net profit of 380 million yuan in the fourth quarter with a comprehensive gross margin of 21.3%. Full-year revenue reached 76.72 billion yuan, up 87.7%, while net losses narrowed to 1.14 billion yuan—an 80.3% reduction from 2024’s 5.79 billion yuan. The budget-friendly MONA M03 contributed over 40% of sales volume, while rapid growth in technical service revenue drove a dual improvement in both sales and profitability structure.

NIO fulfilled founder William Li’s promise of a “fourth-quarter profit,” delivering a net profit of 122 million yuan and pushing automotive gross margins to 18%. Full-year revenue hit 87.49 billion yuan, a 33% increase, with net losses narrowing to 15.57 billion yuan. This was driven by unleashed economies of scale and an optimized product mix—specifically, a surge in ES8 sales during the fourth quarter lifted the average selling price.

Li Auto stands in contrast to the other three. Revenue fell 22.2% year-on-year to 112.31 billion yuan, while attributable net profit plummeted 85.8% to 1.12 billion yuan. Although it remained profitable in the fourth quarter, this was largely supported by non-operating income like interest.

Li Auto’s profit decline stemmed from a stalled pure-electric strategy: deliveries of the i6 and i8 missed expectations, and the MEGA faced a massive recall due to safety issues, damaging brand credibility and incurring huge costs. At the same time, competition in the extended-range segment intensified, driving deliveries down 19% to 406,000 units and shrinking gross margins by 2 percentage points to 18.7%. Even so, Li Auto remains the most profitable startup.

Taken together, the turnaround for NIO, XPENG, and Leapmotor wasn’t merely a result of climbing sales volumes. It was the combined effect of unleashed economies of scale, a product mix shift toward higher-margin models, and tighter control over R&D and marketing expenses.

However, it must be noted that when core product lines stumble, accumulated scale and profit foundations can contract rapidly. For startups, the margin for error in product iteration is shrinking. Shifting from expansion-first to efficiency-first is becoming the central challenge of this stage.

2026: Three Types of Automakers to Watch

A quarter of 2026 has already passed. Market judgment on automakers has shifted from a single focus on sales scale to a comprehensive assessment of profitability, growth quality, and structural stability. Several brokerages and research firms are currently bullish on three types of automakers.

Image Source: BYD Auto

The first category includes companies with scale and cost control. Analysts at Kaiyuan Securities note that while BYD faces short-term pressure from domestic competition and rising raw material costs, its continued overseas expansion and accelerated rollout of new technologies could see attributable net profit grow to 40.7 billion yuan in 2026.

Haitong International favors Geely Auto, citing the “sports + luxury” dual flagship strategy formed by the ZEEKR 8X and 9X, which promises a breakthrough in the high-end market, alongside sustained export growth. It expects Geely’s 2026 deliveries to reach 3.49 million units, with new energy penetration rising to 64%.

Dong Jing also believes Geely’s Haohan intelligent architecture and Leishon electrification technology now cover all vehicle categories, with its multi-brand matrix precisely targeting various segments. Backed by global resources from Volvo and smart, its export growth is leading the industry. Geely’s 2026 export target is 640,000 units, an increase of over 50%.

Large-scale production helps these firms dilute fixed costs, while robust supply chain systems give them greater initiative in price competition.

The second category comprises companies with clear competitive advantages in niche segments. Great Wall Motor is a prime example. China Merchants Securities is bullish on the per-vehicle profit boost from its Tank brand and new WEY models, forecasting a 19% increase in net profit to 11.8 billion yuan in 2026.

Leapmotor, with its full matrix coverage in mainstream price ranges, is seen by institutions as one of the most explosive players. Its goal of sprinting to 1 million sales in 2026 is aggressive, but if its D-platform successfully impacts the high-end market and its overseas expansion strategy takes off, it could make a critical leap from “dark horse” to “giant.”

The third category involves growth companies nearing a profitability inflection point. As the industry enters an efficiency-first phase, market tolerance for long-term losses is waning.

PYB International notes that NIO will launch three new large vehicles in 2026, targeting 40% to 50% delivery growth, which could lead to full-year profitability. XPENG, meanwhile, may see a valuation boost due to technical competitiveness in areas like VLA2.0, “dual-energy” models, and physical AI. Its first quarterly profit has already validated the path of “scaling up plus monetizing technology.”

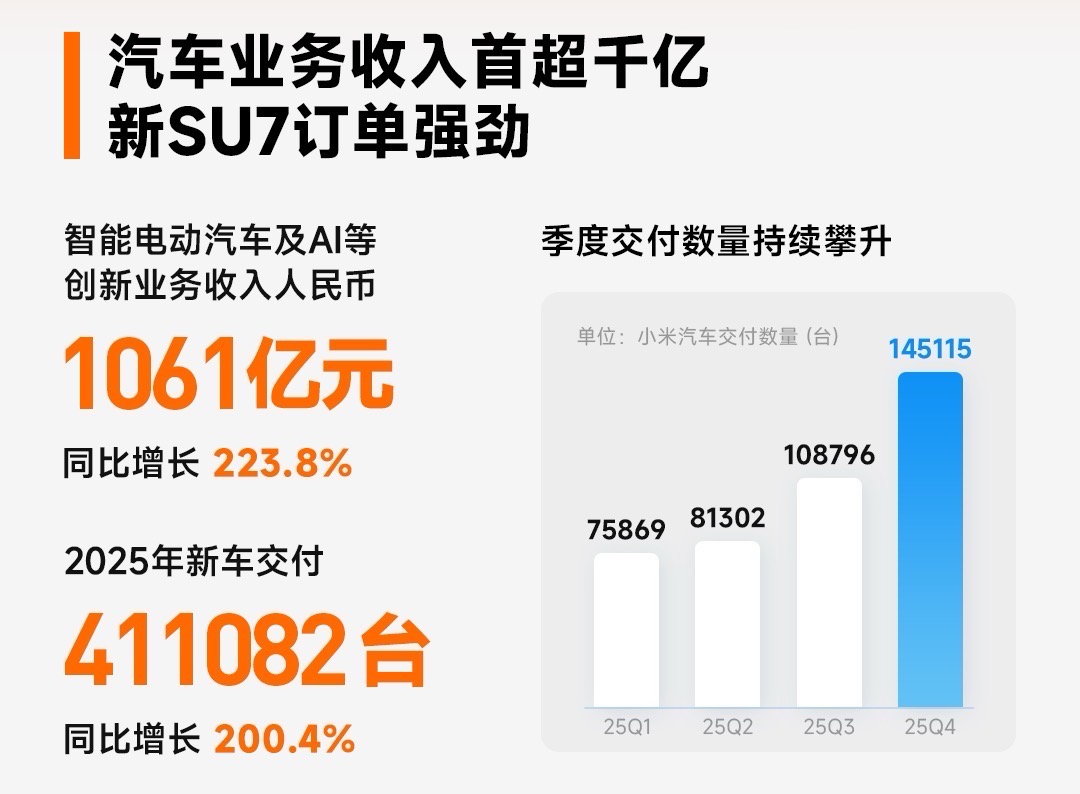

Image Source: Xiaomi

Dong Jing is also paying close attention to two cross-sector players. Xiaomi Auto, for one, has built unique advantages through its “human-car-home” ecosystem, a user base of hundreds of millions from its phones and smart home devices, and the seamless cross-device flow of HyperOS. With new models like SUVs launching in 2026, supply chain control and economies of scale are set to improve. Together, these factors will drive sustained growth in brand premium and market share.

Harmony Intelligent Mobility Alliance (HIMA) relies on Huawei’s full-stack smart automotive solutions, with its ADS advanced driving system and HarmonyOS cockpits leading the industry. In 2026, the matrix of partner automakers will expand further, while the AITO, Luxeed, Stelato, Zunjie, and Shangjie series cover all price segments. Driven by these factors, HIMA’s product strength and market share are set for a rapid ascent.

Overall, however, institutional sentiment toward the 2026 industry is cautious. While the penetration rate of new energy vehicles will continue to rise, driving some volume growth, price competition is unlikely to ease significantly in the short term, keeping pressure on corporate profitability. The market expects 2026 to be a process of “slow repair” rather than a quick rebound, with divergence among automakers intensifying further.

Conclusion

The 2025 financials sent a clear signal: profitability divergence among automakers is accelerating. Industry profit margins remain pinned at a low 4.1%, and the extreme competition warned of by Cui Dongshu has never really left.

Even top players like BYD and Geely are hardly sleeping easy. Price wars continue to devour margins, R&D spending stays high, and overseas markets face the dual risks of tariff barriers and geopolitics. If sales growth slows or technological iteration stalls, economies of scale could instantly turn into a burden of costs.

For non-leading automakers, the situation is even more perilous. Without the cushion of scale or core technological moats, relying on one or two hit products is not enough to survive the long elimination race.

In 2026, divergence will only deepen. Those who survive will rely not on stories, but on gross margins, free cash flow, and the confidence to keep betting through the winter.