According to data compiled by the Gasgoo Automotive Research Institute, as of January 2026, China's new energy vehicle (NEV) electrification segments are entering a phase marked by the consolidation of leading players and intensifying competition. Across key areas such as power battery, power battery pack, and BMS, installation data shows resources increasingly concentrating among companies with strong innovation capabilities, scalable supply capacity, and full value chain coverage, while the divergence between automakers' vertical integration and third-party suppliers continues to widen, offering key insights into the industry's competitive landscape, development trends, and localization progress.

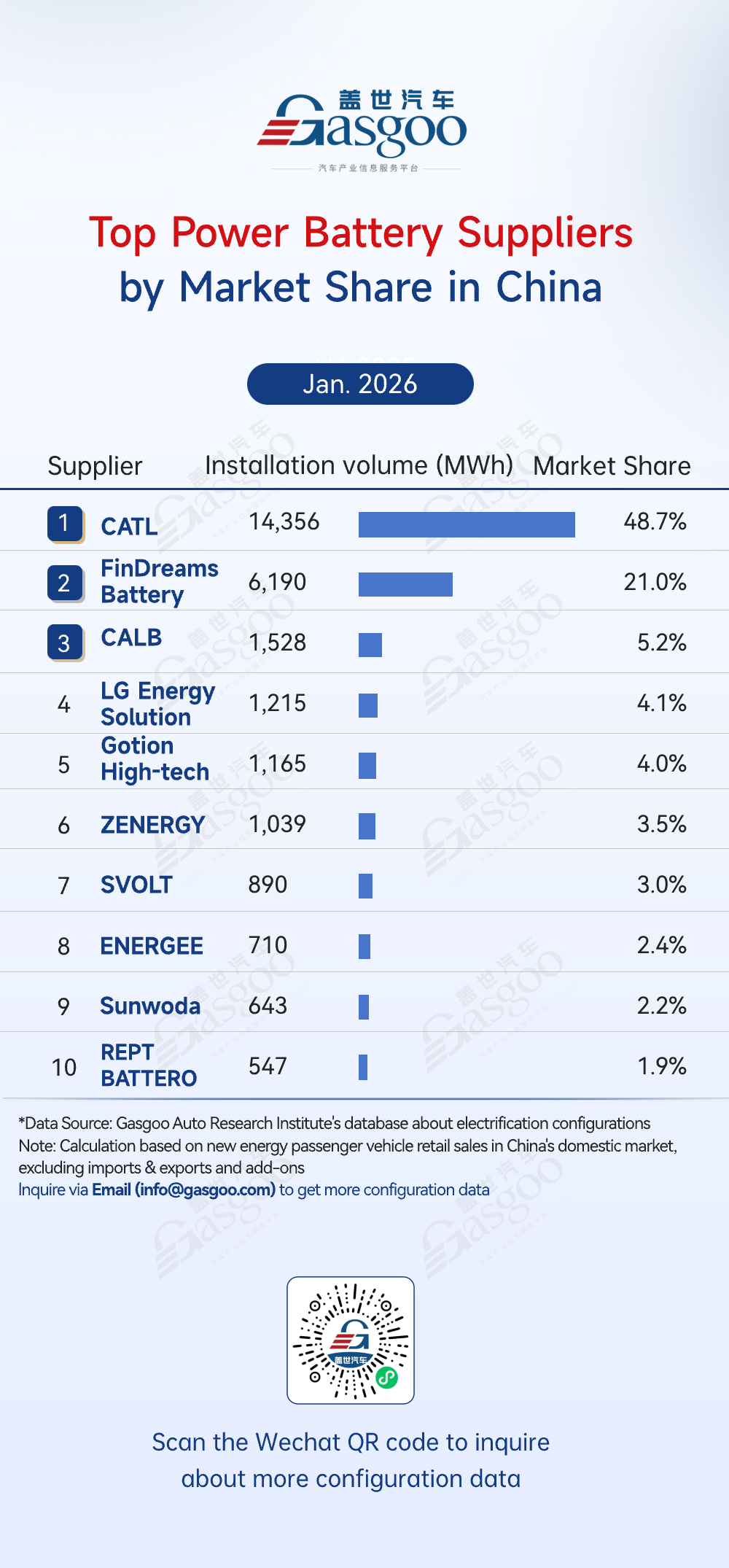

Top power battery suppliers

CATL: 14,356 MWh installed, 48.7% market share

FinDreams Battery: 6,190 MWh installed, 21.0% market share

CALB: 1,528 MWh installed, 5.2% market share

LG Energy Solution: 1,215 MWh installed, 4.1% market share

Gotion High-tech: 1,165 MWh installed, 4.0% market share

ZENERGY: 1,039 MWh installed, 3.5% market share

SVOLT: 890 MWh installed, 3.0% market share

ENERGEE: 710 MWh installed, 2.4% market share

Sunwoda: 643 MWh installed, 2.2% market share

REPT BATTERO: 547 MWh installed, 1.9% market share

Based on power battery installation data for January 2026, China's NEV passenger vehicle battery market continued to exhibit a "one dominant player with several strong competitors" pattern, with leading players further strengthening their positions. CATL ranked first with 14,356 MWh of installed capacity (48.7% share)—its highest level for the same period in the past four years—continuing to consolidate its leadership through full value chain integration, technological iteration, and scale advantages. FinDreams Battery followed with 6,190 MWh (21.0% share), maintaining steady growth driven by its deep integration with BYD and strong vertical integration capabilities.

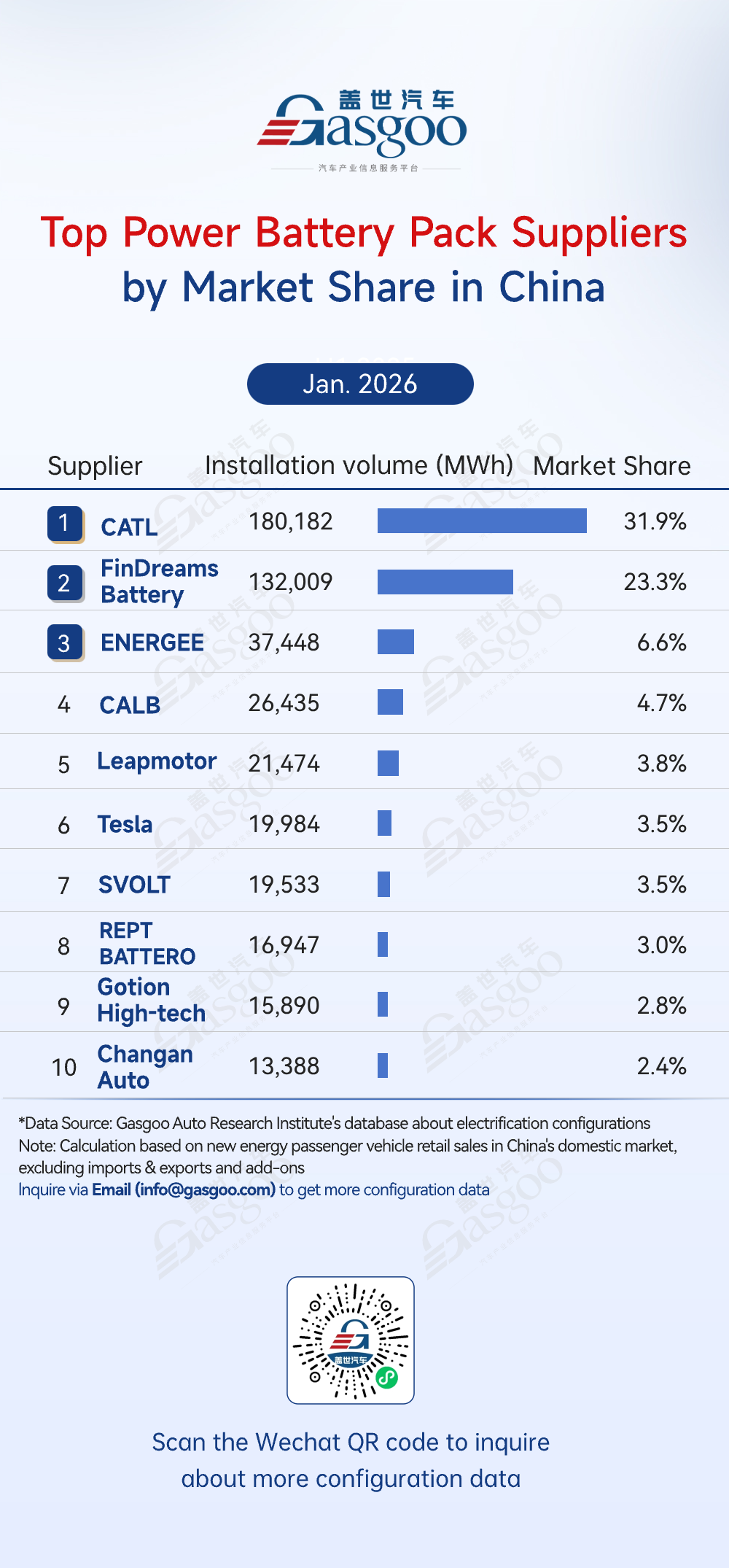

Top power battery pack suppliers

CATL: 180,182 sets installed, 31.9% market share

FinDreams Battery: 132,009 sets installed, 23.3% market share

ENERGEE: 37,448 sets installed, 6.6% market share

CALB: 26,435 sets installed, 4.7% market share

Leapmotor: 21,474 sets installed, 3.8% market share

Tesla: 19,984 sets installed, 3.5% market share

SVOLT: 19,533 sets installed, 3.5% market share

REPT BATTERO: 16,947 sets installed, 3.0% market share

Gotion High-tech: 15,890 sets installed, 2.8% market share

Changan Auto: 13,388 sets installed, 2.4% market share

Based on battery pack installation data for January 2026, China's market landscape has shifted notably, with the top two suppliers accounting for over 55% of total share, forming a "dual-leader with tiered differentiation" pattern. CATL ranked first with 180,182 sets (31.9% share), surpassing FinDreams Battery, driven by its strengths in standardized pack products, technical adaptability, and scalable supply capabilities. FinDreams Battery followed with 132,009 sets (23.3% share), supported by BYD's vertically integrated model, which ensures stable in-house demand and sustained growth momentum.

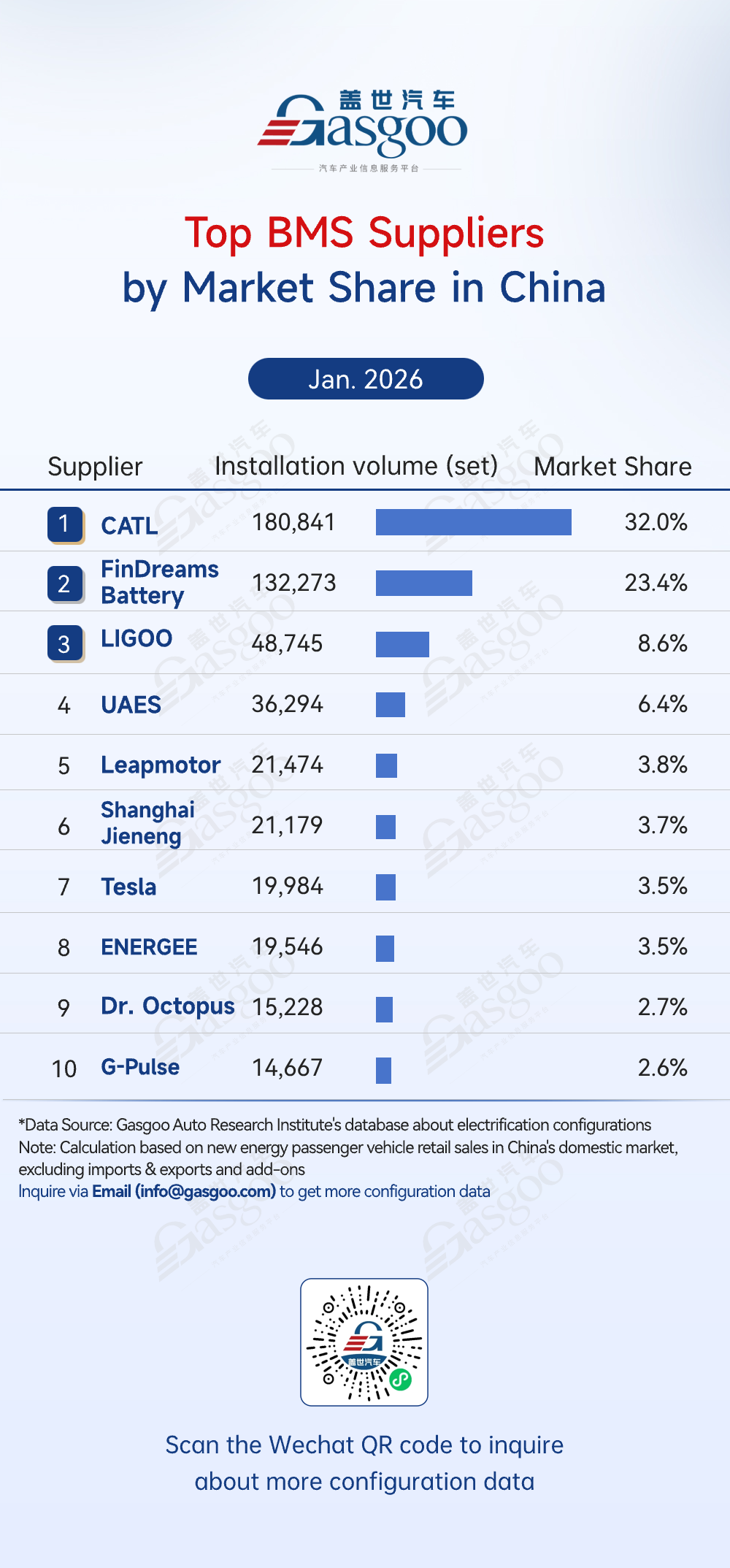

Top BMS suppliers

CATL: 180,841 sets installed, 32.0% market share

FinDreams Battery: 132,273 sets installed, 23.4% market share

LIGOO: 48,745 sets installed, 8.6% market share

UAES: 36,294 sets installed, 6.4% market share

Leapmotor: 21,474 sets installed, 3.8% market share

Shanghai Jieneng: 21,179 sets installed, 3.7% market share

Tesla: 19,984 sets installed, 3.5% market share

ENERGEE: 19,546 sets installed, 3.5% market share

Dr. Octopus: 15,228 sets installed, 2.7% market share

G-Pulse: 14,667 sets installed, 2.6% market share

In January 2026, China's BMS market showed a clear pattern of "dual leaders, tiered differentiation, and accelerating OEM in-house development" CATL ranked first with 180,841 sets (32.0% share), leveraging its strong expertise in battery management technology and full value chain integration to achieve broad coverage across major automakers. FinDreams Battery followed with 132,273 sets (23.4% share), supported by BYD's vertically integrated model, with its in-house BMS deeply integrated into its vehicle lineup, sustaining strong organic growth momentum.

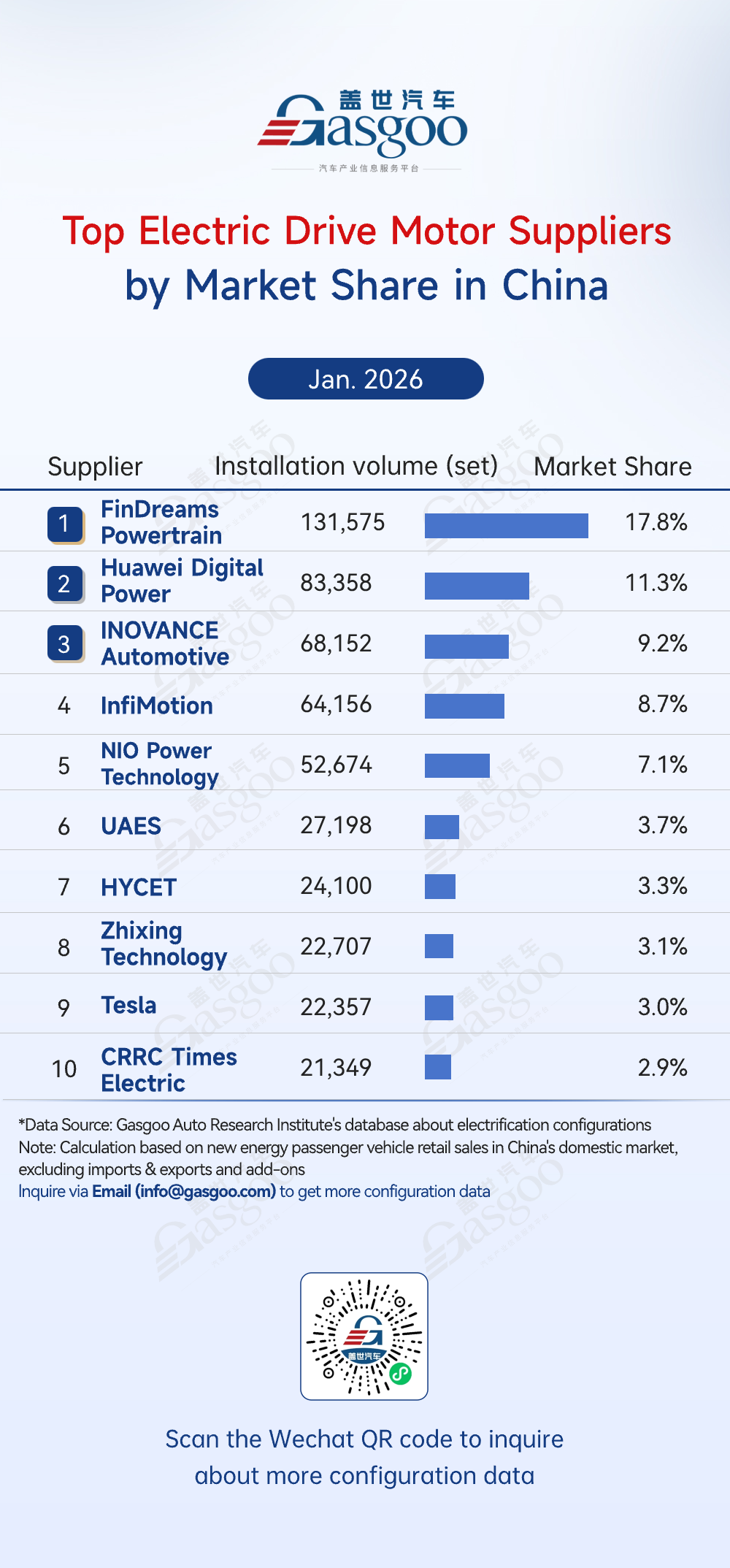

Top electric drive motor suppliers

FinDreams Powertrain: 131,575 sets installed, 17.8% market share

Huawei Digital Power: 83,358 sets installed, 11.3% market share

INOVANCE Automotive: 68,152 sets installed, 9.2% market share

InfiMotion: 64,156 sets installed, 8.7% market share

NIO Power Technology: 52,674 sets installed, 7.1% market share

UAES: 27,198 sets installed, 3.7% market share

HYCET: 24,100 sets installed, 3.3% market share

Zhixing Technology: 22,707 sets installed, 3.1% market share

Tesla: 22,357 sets installed, 3.0% market share

CRRC Times Electric: 21,349 sets installed, 2.9% market share

In January 2026, the electric drive motor market showed a pattern of "high concentration at the top, tiered differentiation, and the coexistence of OEM in-house supply and specialized suppliers." FinDreams Powertrain ranked first with 131,575 sets (17.8% share), leveraging BYD's vertically integrated model to achieve strong synergy between its motors and vehicle platforms, maintaining advantages in large-scale supply and cost control. Companies including Huawei Digital Energy, Inovance Automotive, StarDrive, and NIO Power Technology followed, forming the core competitive tier.

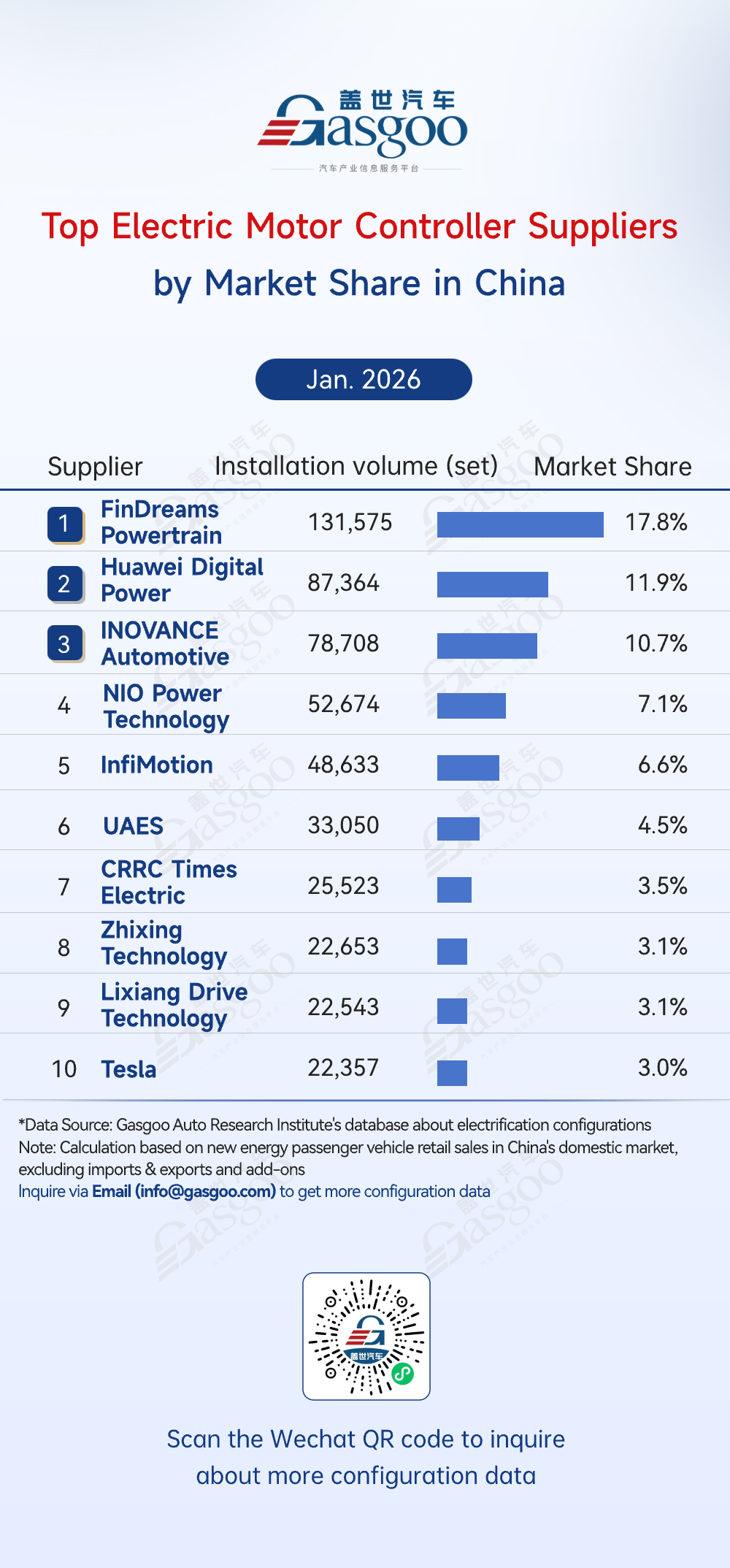

Top electric motor controller suppliers

FinDreams Powertrain: 131,575 sets installed, 17.8% market share

Huawei Digital Power: 87,364 sets installed, 11.9% market share

INOVANCE Automotive: 78,708 sets installed, 10.7% market share

NIO Power Technology: 52,674 sets installed, 7.1% market share

InfiMotion: 48,633 sets installed, 6.6% market share

UAES: 33,050 sets installed, 4.5% market share

CRRC Times Electric: 25,523 sets installed, 3.5% market share

Zhixing Technology: 22,653 sets installed, 3.1% market share

Lixiang Drive Technology: 22,543 sets installed, 3.1% market share

Tesla: 22,357 sets installed, 3.0% market share

Based on motor controller installation data for January 2026, the market is led by OEM in-house suppliers, followed by strong third-party players, with in-house penetration continuing to accelerate and a clear concentration among leading players. FinDreams Powertrain ranked first with 131,575 sets (17.8% share), maintaining its advantage through deep integration with BYD's vehicle platforms. Leveraging full value chain vertical integration, it continues to strengthen its competitiveness in large-scale supply and cost control, further reinforcing its leadership in OEM in-house motor control systems.

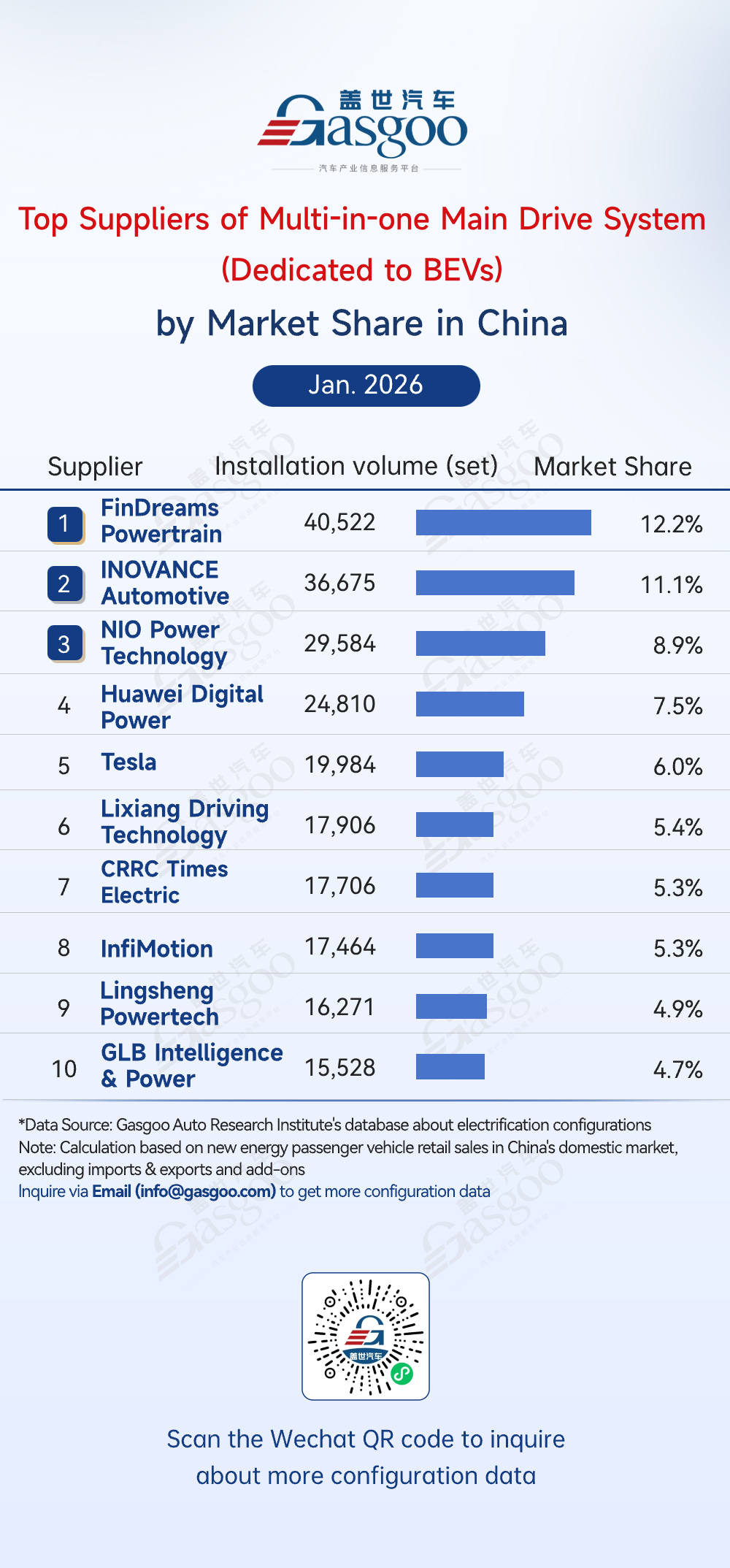

Top suppliers of power semiconductor device (dedicated to e-drive)

FinDreams Powertrain: 40,522 sets installed, 12.2% market share

INOVANCE Automotive: 36,675 sets installed, 11.1% market share

NIO Power Technology: 29,584 sets installed, 8.9% market share

Huawei Digital Power: 24,810 sets installed, 7.5% market share

Tesla: 19,984 sets installed, 6.0% market share

Lixiang Driving Technology: 17,906 sets installed, 5.4% market share

CRRC Times Electric: 17,706 sets installed, 5.3% market share

InfiMotion: 17,464 sets installed, 5.3% market share

Lingsheng Powertech: 16,271 sets installed, 4.9% market share

GLB Intelligence & Power: 15,528 sets installed, 4.7% market share

In January 2026, the power semiconductor device (dedicated to e-drive) market shows a pattern of "leading players, fragmented structure, and coexistence of OEM in-house supply and specialized suppliers." FinDreams Powertrain ranked first with 40,522 sets installed (12.2% share), leveraging BYD's vertical integration in e-drive systems to maintain core advantages in system integration, cost efficiency, and large-scale application, supporting in-house vehicle demand. INOVANCE Automotive followed with 36,675 sets (11.1% share), together forming the top tier with a combined share exceeding 23%, leading the market.

![[Gasgoo Express] Ford and Geely Reach Agreement; Antolin Secures US Court Bankruptcy Protection](https://gascloud.gasgoo.com/production/2026/07/a3c8220e-382e-456f-a768-77cad93f17f1-1784991559.png)