From January to December 2025, China's passenger vehicle exports were marked by NEV leadership, strong performance from top players, and growing differences in growth among brands. In Europe, SAIC PV held the top position, while Leapmotor stood out with a 1,000.3% YoY surge. In Southeast Asia, BYD led the market with a 216.8% YoY increase, as Chery Auto, Changan Auto, and Great Wall Motor also expanded rapidly.

North America was led by NEV brands, with BYD surging 176.0% YoY. In Central and South America, BYD and Chery stayed ahead, while Great Wall Motor, Jiangling Motors, and DFSK each grew over 60%. In the Middle East, Chery Auto remained No.1 despite a 25.7% YoY decline, as BYD and Great Wall Motor doubled shipments on NEV momentum. Overall, Chinese brands continued to expand overseas, driven by stronger products and localization capabilities.

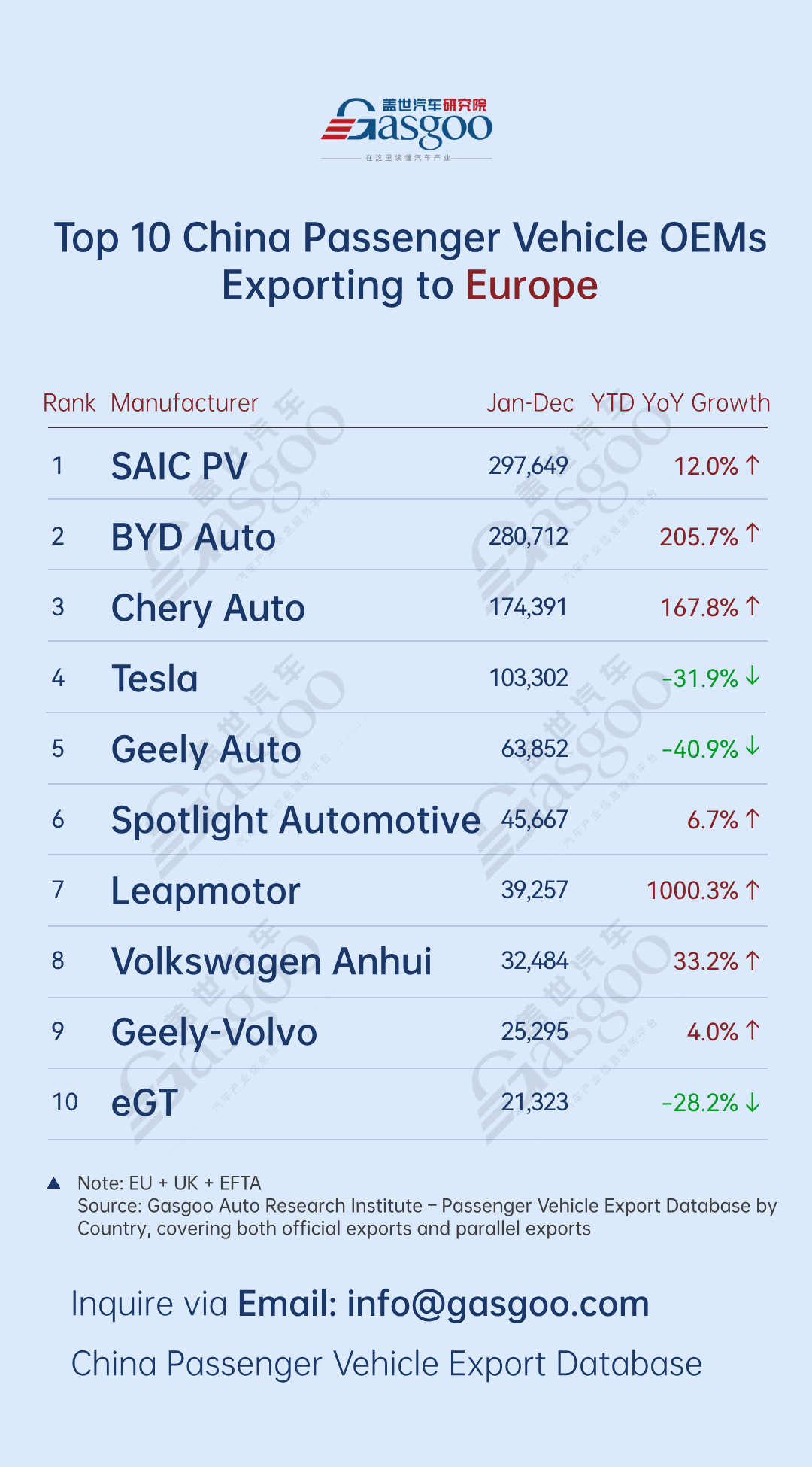

Top 10 Chinese automakers by passenger vehicle exports to Europe

SAIC PV: 297,649 units, up 12.0% year-on-year

BYD Auto: 280,712 units, up 205.7% year-on-year

Chery Auto: 174,391 units, up 167.8% year-on-year

Tesla: 103,302 units, down 31.9% year-on-year

Geely Auto: 63,852 units, down 40.9% year-on-year

Spotlight Automotive: 45,667 units, up 6.7% year-on-year

Leapmotor: 39,257 units, up 1000.3% year-on-year

Volkswagen Anhui: 32,484 units, up 33.2% year-on-year

Geely-Volvo: 25,295 units, up 4.0% year-on-year

eGT: 21,323 units, down 28.2% year-on-year

From January to December, Europe showed a highly concentrated competitive landscape. SAIC PV, BYD, and Chery formed the clear top tier, ranking first to third with exports of 297,649 units, 280,712 units, and 174,391 units, respectively, totaling over 750,000 units combined. While SAIC PV maintained its lead, BYD narrowed the gap to about 16,900 units, rapidly closing in on the top position.

Emerging players delivered particularly strong performances. Leapmotor exported 39,257 units, posting an exceptional 1000.3% YoY surge, becoming a standout example of new Chinese brands expanding in Europe. Volkswagen Anhui (+33.2% YoY) and Spotlight Automotive (+6.7% YoY) achieved steady growth on the back of established market positioning, while Geely Volvo recorded a modest 4.0% YoY increase.

At the same time, market divergence became more pronounced. Tesla's exports to Europe fell 31.9% YoY to 103,302 units, while Geely Auto declined 40.9% to 63,852 units. eGT also recorded a 28.2% YoY drop. These fluctuations likely reflect intensifying competition from a growing number of Chinese entrants, the accelerating electrification push of European domestic brands, and product cycle adjustments within the companies themselves.

Overall, Chinese brands continued to expand their presence in Europe throughout the year. Established leaders consolidated their positions, while emerging players carved out new growth space, collectively driving export volumes higher. At the same time, widening growth gaps among automakers signal intensifying competition ahead. Product competitiveness, supply chain resilience, and localized operations will be decisive factors for long-term success in the European market.

Top 10 Chinese automakers by passenger vehicle exports to Southeast Asia

BYD Auto: 176,132 units, up 216.8% year-on-year

Chery Auto: 88,356 units, up 131.5% year-on-year

Geely Auto: 76,565 units, up 38.0% year-on-year

Changan Auto: 35,163 units, up 77.3% year-on-year

Great Wall Motor: 24,313 units, up 68.0% year-on-year

Tesla: 19,405 units, up 42.0% year-on-year

Jiangsu Yueda Kia: 17,699 units, down 7.0% year-on-year

Jiangling Motor: 17,482 units, up 20.3% year-on-year

SAIC PV: 15,425 units, down 43.7% year-on-year

SAIC-GM-Wuling: 12,999 units, down 43.5% year-on-year

From January to December, Southeast Asia showed a highly concentrated market structure with clear growth divergence. BYD led the region with 176,132 units exported, surging 216.8% YoY, underscoring the strength of its NEV lineup and localized strategy. Chery followed with 88,356 units, up 131.5% YoY, reflecting strong product-market fit. Geely ranked third with 76,565 units, posting steady 38.0% YoY growth and demonstrating solid market execution.

At the same time, Changan, Great Wall, Tesla, and Jiangling Motor all recorded positive growth, with YoY increases ranging from 20.3% to 77.3%. Changan (+77.3%) and Great Wall (+68%) stood out, highlighting strong market expansion momentum. However, market divergence was also apparent: Jiangsu Yueda Kia fell 7.0% YoY, while SAIC PV and SAIC-GM-Wuling saw sharper declines of 43.7% and 43.5%, respectively.

Overall, Chinese brands continued to deepen their presence in Southeast Asia, with NEVs remaining the main driver of export growth. Leading players further strengthened their positions through technological advantages and established distribution networks, while declines among some companies indicate the market is shifting from "volume expansion" to more refined, localized operations. Looking ahead, precise product-market fit and deeper local integration will be key factors for success in the region.

Top 10 Chinese automakers by passenger vehicle exports to North America

BYD Auto: 130,452 units, up 176.0% year-on-year

SAIC-GM-Wuling: 105,864 units, up 15.4% year-on-year

SAIC PV: 45,982 units, down 14.5% year-on-year

Geely Auto: 44,280 units, up 76.6% year-on-year

SAIC-GM: 39,860 units, down 43.8% year-on-year

Changan-Ford: 37,158 units, down 19.9% year-on-year

Chery Auto: 36,989 units, up 26.3% year-on-year

Jiangsu Yueda Kia: 31,121 units, up 5.9% year-on-year

Changan Auto: 19,544 units, up 137.9% year-on-year

GAC Trumpchi: 15,640 units, up 30.2% year-on-year

From January to December, North America was led by NEVs, while traditional players saw fluctuations. BYD topped the market with 130,452 units, up 176.0% YoY, demonstrating strong NEV competitiveness. SAIC-GM-Wuling followed with 105,864 units (+15.4%), maintaining steady growth. Geely (44,280 units, +76.6%) and Changan (+137.9%) posted strong gains, while Chery, Jiangsu Yueda Kia, and GAC Trumpchi also grew, reflecting the region's diversified market dynamics.

At the same time, some traditional automakers saw notable fluctuations. SAIC PV exported 45,982 units, down 14.5% YoY; SAIC-GM-Wuling fell 43.8% to 39,860 units; and Changan-Ford declined 19.9%. These results suggest their product portfolios still have room to better align with current North American market trends.

Top 10 Chinese automakers by passenger vehicle exports to Central and South America

BYD Auto: 165,325 units, up 26.4% year-on-year

Chery Auto: 151,527 units, up 40.6% year-on-year

Great Wall Motor: 74,588 units, up 87.2% year-on-year

Jiangsu Yueda Kia: 50,683 units, up 0.0% year-on-year

Jiangling Motor: 40,713 units, up 95.5% year-on-year

Geely Auto: 31,821 units, up 33.5% year-on-year

SAIC-GM-Wuling: 28,564 units, down 6.4% year-on-year

DFSK: 25,693 units, up 60.0% year-on-year

SAIC PV: 25,677 units, up 54.0% year-on-year

Changan Auto: 25,221 units, up 24.4% year-on-year

From January to December, BYD led the Central and South American market with 165,325 units exported, up 26.4% YoY, further strengthening the appeal and brand influence of its NEV lineup. Chery followed with 151,527 units, up 40.6% YoY, leveraging affordable models and deep local distribution to steadily narrow the gap with the leader.

Several automakers became key drivers of regional export growth. Great Wall Motor, Jiangling Motor, and DFSK each achieved over 60% YoY growth, with Jiangling's 95.5% surge standing out, reflecting strong demand alignment for its commercial and passenger models. SAIC PV steadily expanded with a 54.0% YoY increase, highlighting ongoing product competitiveness, while Geely (+33.5%) and Changan (+24.4%) maintained solid growth, demonstrating market resilience. However, some companies faced pressure: Jiangsu Yueda Kia's exports remained flat, and SAIC-GM-Wuling fell 6.4% YoY, indicating a need to optimize regional strategies and product portfolios.

Top 10 Chinese automakers by passenger vehicle exports to Middle East

Chery Auto: 236,241 units, down 25.7% year-on-year

BYD Auto: 133,766 units, up 128.4% year-on-year

SAIC PV: 104,824 units, down 0.6% year-on-year

Changan Auto: 91,916 units, up 38.6% year-on-year

Jiangsu Yueda Kia: 85,203 units, up 12.4% year-on-year

Geely Auto: 78,389 units, down 4.4% year-on-year

FAW-Toyota: 68,256 units, up 46.0% year-on-year

Great Wall Motor: 53,563 units, up 127.0% year-on-year

Southeast Auto: 48,906 units, up 111.5% year-on-year

Beijing Hyundai: 42,065 units, up 26.9% year-on-year

From January to December, the Middle East market was marked by stable leadership at the top and divergent growth among players. Chery led the region with 236,241 units exported, but its volume fell 25.7% YoY due to a high prior-year base and accelerated competitor activity. BYD followed with 133,766 units, up 128.4% YoY, achieving rapid growth as its NEVs closely matched local energy transition trends and rising consumer demand, steadily narrowing the gap with the leader.

At the same time, some automakers saw growth slow: SAIC PV edged down 0.6% YoY, and Geely fell 4.4%, highlighting the need to update product portfolios and competitive strategies to match the rapidly changing market. In contrast, several companies showed strong momentum: Changan (+38.6%), Jiangsu Yueda Kia (+12.4%), FAW-Toyota (+46.0%), and Beijing Hyundai (+26.9%) all expanded steadily, while Southeast Auto and Great Wall Motor achieved over 100% growth, serving as key drivers of regional market expansion.

Overall, the Middle East has become a key strategic market for Chinese passenger vehicle exports. Success increasingly depends on NEV deployment and product differentiation. For traditional leaders, accelerating strategy adjustments to better match regional demand is crucial, while high-growth players need to strengthen local channels and core product competitiveness to build a solid foundation for sustainable long-term expansion.