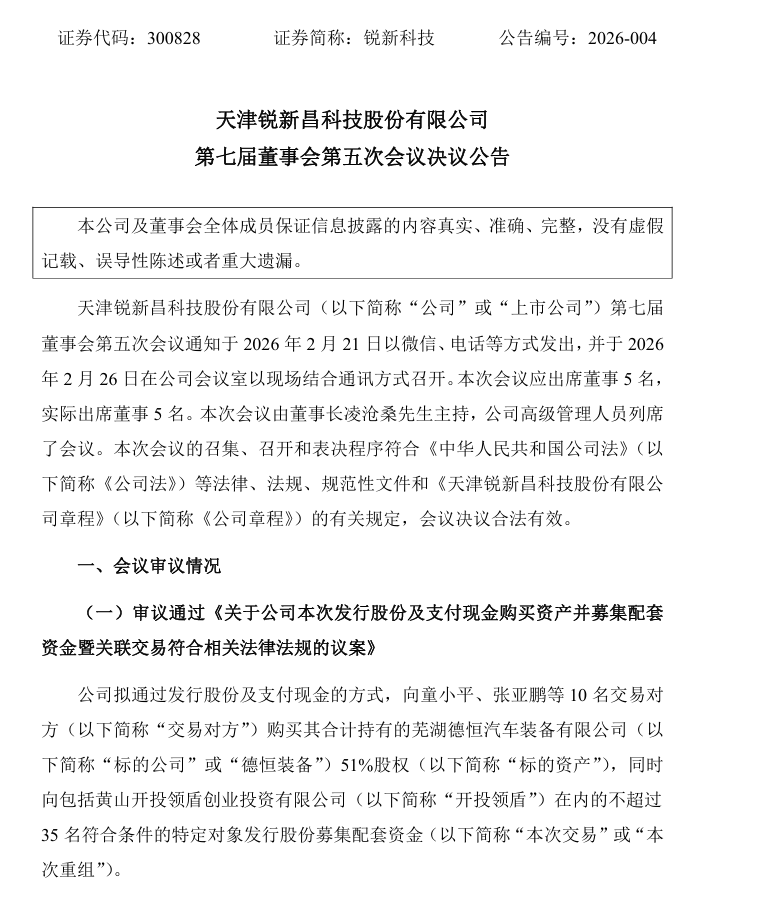

Gasgoo Munich- On February 27, Tianjin Ruixin Chang Technology Co., Ltd. (hereinafter "Ruixin Technology") announced plans to purchase a combined 51% equity stake in Wuhu Deheng Automotive Equipment Co., Ltd. (hereinafter "Deheng Equipment") from ten counterparties, including Tong Xiaoping and Zhang Yapeng. The acquisition will be financed through a mix of share issuance and cash. Concurrently, the company plans to issue shares to no more than 35 eligible specific investors—including Huangshan Kaitou Lingsdun Venture Capital Investment Co., Ltd.—to raise supporting funds for the transaction.

Image source: Screenshot of Ruixin Technology announcement

This merger represents a strategic breakout for Ruixin Technology amid mounting performance pressure, marking a critical move in its "industry + capital" dual-drive strategy. As the new energy vehicle supply chain enters a phase of deep integration, this partnership highlights a fresh wave of consolidation sweeping through the components sector.

Transaction Breakdown: A Precision Move to Strengthen and Supplement the Chain

The announcement outlines a two-part deal: acquiring assets via stock and cash, followed by a fundraising round. While the fundraising depends on the asset acquisition's success, the purchase will proceed regardless of whether the capital is fully raised. The pricing benchmark for the share issuance is set by the company's 7th board meeting resolution, with the issue price fixed at 18.08 yuan per share.

It is worth noting that as of the prospectus release, auditing and valuation of the target assets remain incomplete. The final valuation and transaction price will be negotiated based on filed assessment results. The deal is expected to constitute a major asset restructuring and a related-party transaction, though it does not involve a backdoor listing. Upon completion, Deheng Equipment will become a Ruixin Technology subsidiary, unlocking potential for multi-dimensional business synergy.

Fundamentally, this is a classic case of chain strengthening and supplementing. Ruixin Technology is a key player in high-end precision aluminum components, already supplying giants like BYD and Vitesco Technologies. However, recent years have brought sustained performance pressure, with growth bottlenecks becoming increasingly apparent due to a singular business structure.

Image source: Screenshot of Ruixin Technology website

Deheng Equipment focuses on automotive stamping, welding components, and smart equipment. Its core products—body structural assemblies—directly supply mainstream OEMs like Chery, Leapmotor, and JAC. In 2025, the company generated revenue of 922 million yuan and a net profit of 75.21 million yuan, a profitability scale far exceeding Ruixin Technology's current levels.

On the product side, Ruixin's lightweight and thermal management parts, combined with Deheng's stamping and welding assemblies, create a one-stop supply capability that aligns with automaker procurement needs. On the client side, Ruixin's existing base includes OEMs (such as BYD) and Tier 1 suppliers (like Aisin and INOVANCE). Deheng's addition strengthens direct ties to OEMs like Chery and Leapmotor, achieving complementary customer resources and channel expansion.

Industry Deep Dive: Breakout and Integration for SME Parts Makers in Full Swing

The union of Ruixin Technology and Deheng Equipment is no isolated incident; it is a microcosm of the automotive components sector's deep dive into consolidation in 2026. Domestically, the penetration rate of new energy vehicles has steadily breached 50%, shifting the supply chain from high-speed expansion to high-quality competition. With the vehicle price war transmitting pressure to the supply chain, small and medium parts makers face a triple threat: fluctuating orders, compressed margins, and the need for technological upgrades. Active breakout has become a matter of survival.

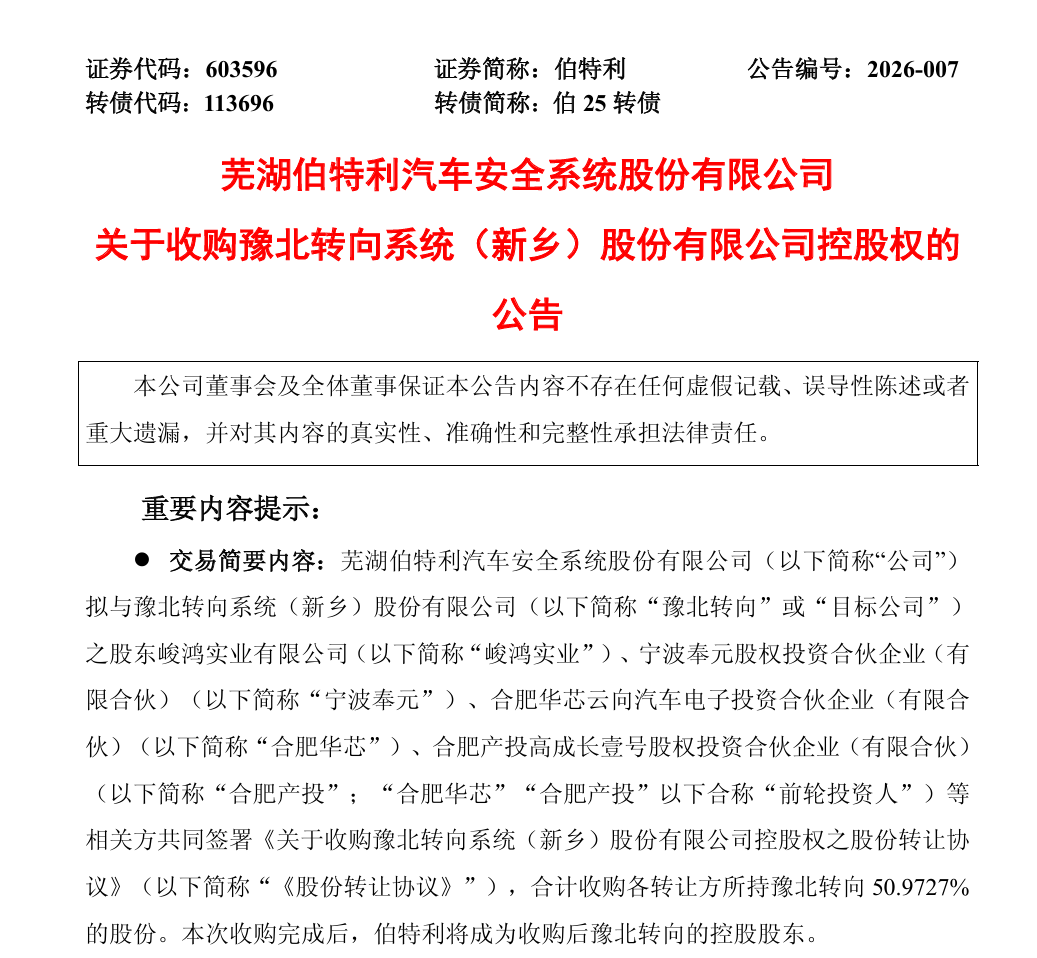

Looking at recent cases, such as Bethel Automotive Safety Systems' planned acquisition of a controlling stake in Yubei Steering System, two features emerge in recent M&A activity. First, the logic has shifted from "scale expansion" to "lean synergy." Companies are no longer chasing revenue volume but focusing on product complementarity and cost optimization—Ruixin's deal is a prime example of lightweight materials merging with body structural components. Second, targets are concentrating on core "new four modernizations" sectors. Assets related to stamping, welding, thermal management, and smart equipment—tied to electrification and intelligence—are hotly contested, while traditional internal combustion engine parts are increasingly marginalized.

Image source: Screenshot of Bethel Automotive Safety Systems announcement

The positive impact of such M&A on the industry is significant. On one hand, it accelerates resource concentration among dominant firms, driving the sector from fragmentation to consolidation, improving overall supply quality and bargaining power, and easing homogeneous competition. On the other hand, it helps listed companies enter high-growth tracks and improve profit structures. By acquiring stable, profitable assets and direct OEM channels, Ruixin Technology is poised to release new earnings potential.

Meanwhile, the relationship between OEMs and parts suppliers is being reshaped. Large component groups with system-level delivery capabilities are increasingly favored by automakers. Single-product, small-scale suppliers face pressure to transform or be integrated as industry barriers continue to rise.

However, post-merger integration risks cannot be ignored. Cultural fusion, management stability, and the alignment of technology systems and supply chains will determine the deal's success. Only if Deheng Equipment maintains operational efficiency and Ruixin Technology provides effective empowerment and control can "synergy on paper" translate into real performance. Additionally, external risks—intensifying competition, high customer concentration, and rapid tech iteration—will continue to test the new, integrated platform.

Overall, Ruixin Technology's bid for a 51% stake in Deheng Equipment is a well-timed and logically clear initiative. It serves as both a strategic breakout for the listed company and a snapshot of the Chinese auto parts industry's move toward centralization and high-end development. As the deal lands and integration progresses, the combined entity is poised to secure a more critical position in the new energy vehicle supply chain, potentially offering a growth path for other parts makers navigating transition.