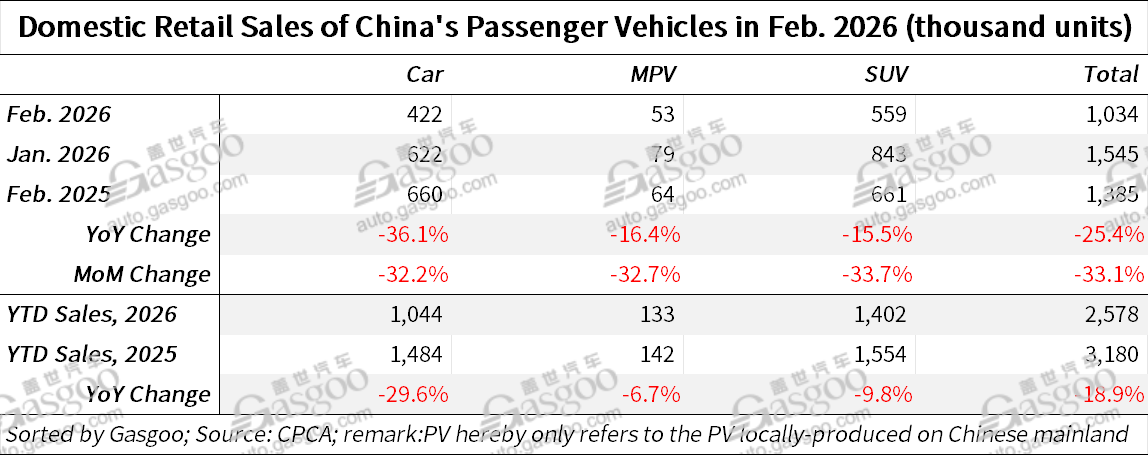

Gasgoo Munich- China's passenger vehicle retail sales totaled 1.034 million units in February, representing a year-on-year decline of 25.4% and a 33.1% drop from the previous month, according to data issued by the China Passenger Car Association ("CPCA").

Cumulative retail sales for the first two months of the year reached 2.578 million units, down 18.9% compared with the same period last year.

The CPCA note that February figures often fluctuate widely due to seasonal factors such as the timing of the Spring Festival holiday. In recent years, China's annual auto sales pattern has typically started weak and strengthened later in the year. Against that backdrop, the 25.4% year-on-year drop recorded in February 2026 falls within the historical range of volatility for the month, albeit toward the weaker end.

Another factor affecting early-year demand is the policy transition in China's new energy vehicle (NEV) market. The long-running purchase tax exemption for NEVs, first introduced in 2014, expired at the end of 2025, leaving the market in a period of adjustment. Some buyers advanced their purchases last year to take advantage of the incentive, creating a short-term pull-forward effect that weighed on sales in January and February. Analysts suggest the resulting fluctuations are largely temporary and should not be interpreted as a structural shift in demand. With the Spring Festival arriving relatively late this year, overall vehicle consumption has become more uneven, and NEV growth has been weaker than expected, prompting calls for additional policy support.

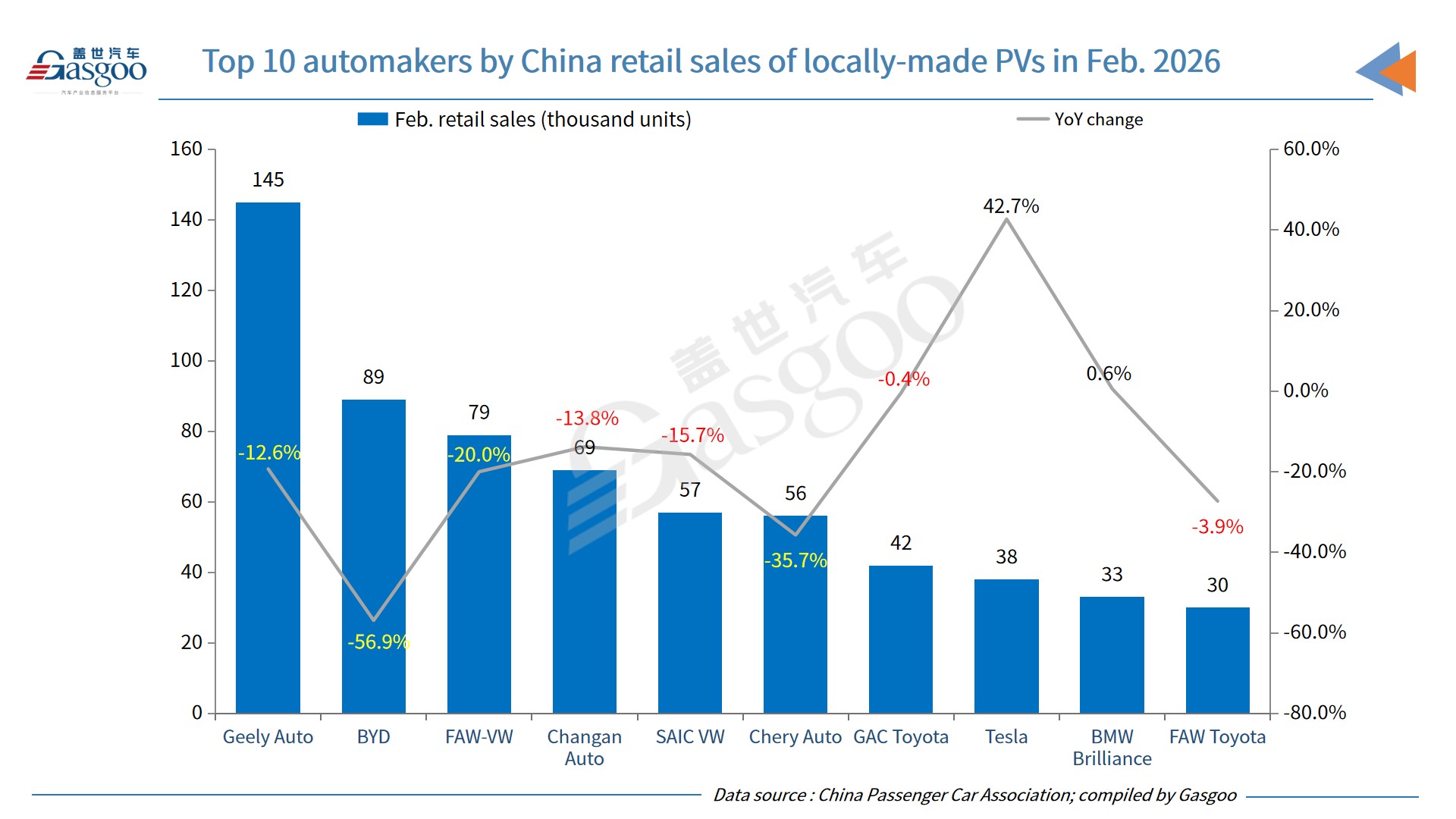

Domestic Chinese brands recorded retail sales of about 630,000 units in February, down 30% year-on-year and 29% from January. Their market share in the domestic passenger car market stood at 61.2%, a decline of 4.3 percentage points from a year earlier. Despite the temporary setback, local automakers continue to see strong growth opportunities in both the NEV segment and export markets. Several traditional manufacturers undergoing transformation—including Geely, Changan Automobile, and Great Wall Motor—have managed to expand their brand presence amid the broader market shift.

Mainstream joint-venture brands sold around 270,000 vehicles at retail in February, marking a 19% decline from a year earlier and a 43% drop from the previous month. Despite the decline in overall volumes, some foreign brand groups gained share. German brands held an 18.2% market share, up 1.2 percentage points year-on-year, while Japanese brands accounted for 12.1%, rising 1.5 percentage points. U.S. brands captured 6.8% of the market, also posting a modest year-on-year gain, and Korean brands saw a slight improvement in share as well.

Premium passenger vehicle retail sales reached about 130,000 units in February, down 12% from a year earlier and 27% from January. However, the segment's market share rose to 12.7%, an increase of two percentage points year-on-year, suggesting that demand for traditional premium brands is beginning to stabilize.

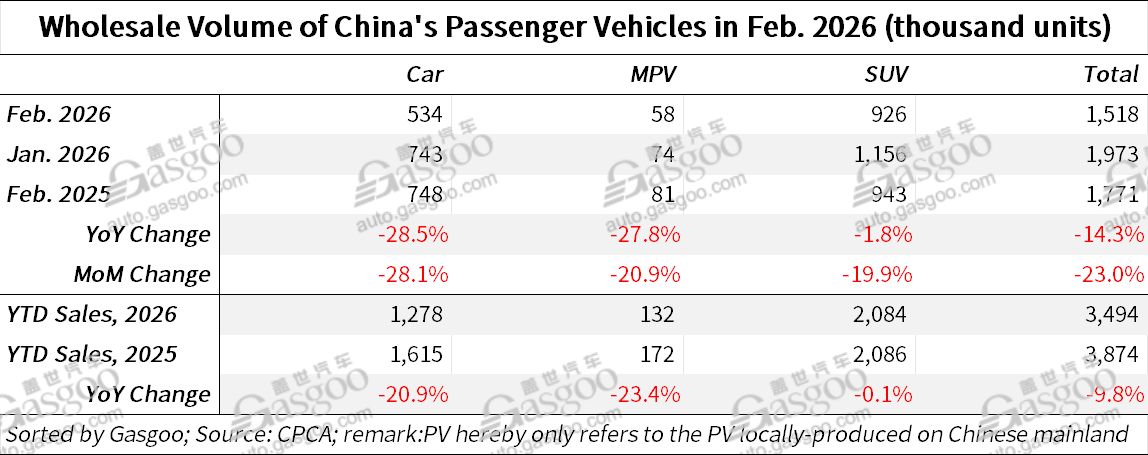

Passenger vehicle wholesale volume from automakers totaled 1.518 million units in February, representing a year-on-year decline of 14.3% and a 23% drop compared with January. Wholesale volumes contracted less sharply than retail sales, partly reflecting adjustments in dealer inventories. Domestic brands accounted for 1.074 million units of wholesale shipments, down 14% year-on-year, while joint-venture brands delivered 283,000 units, a 20% decline year-on-year and a 32% drop month-on-month. Premium vehicle brand shipments reached approximately 161,000 units, slipping just 2% from the same period last year.

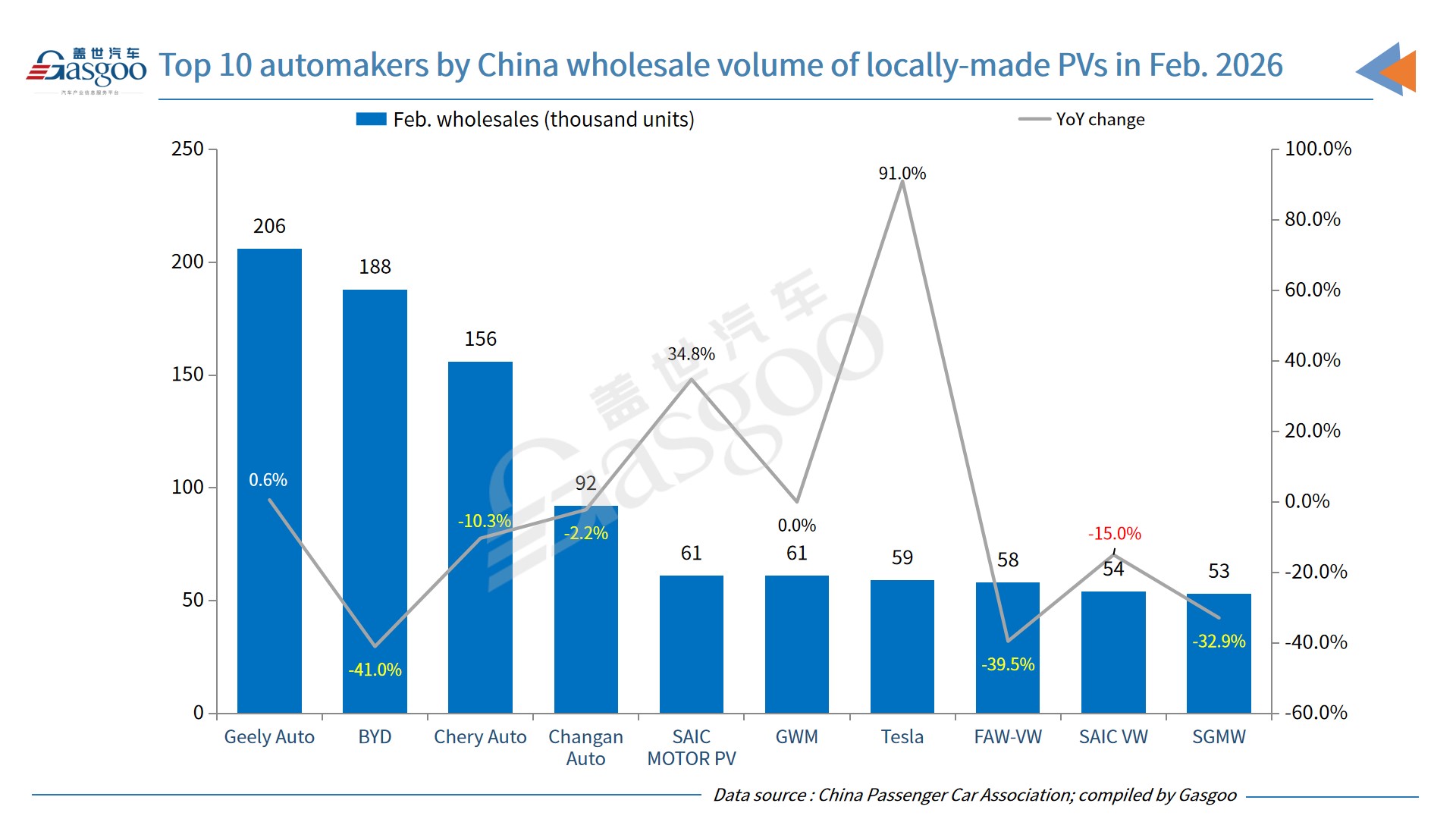

The competitive landscape among major automakers continued to shift in February. Several manufacturers—including Geely Auto, SAIC MOTOR Passenger Vehicle, Tesla, GAC Toyota, Dongfeng Motor, Leapmotor, Li Auto, GAC Trumpchi, NIO, BAIC Passenger Vehicle and Beijing Hyundai—reported year-on-year growth in wholesale volumes.

Three passenger vehicle manufacturers in China recorded monthly wholesale sales exceeding 100,000 units, accounting for about 36% of the overall market. Companies with volumes between 50,000 and 100,000 units captured roughly 29% of the market, while those selling between 10,000 and 50,000 units also held about 29%.

Eight passenger vehicle models recorded wholesale sales exceeding 20,000 units in February, compared with 17 models in January. Leading the list was the Tesla Model Y with 41,404 units, followed by the Geely Xingyuan at 37,859 units and the BYD Song with 34,071 units. Other high-volume models included the Chery Tansuo 06, Geely Boyue, Chery Tiggo 7, the Xiaomi YU7, and the BYD Seagull, each surpassing the 20,000-unit mark during the month.

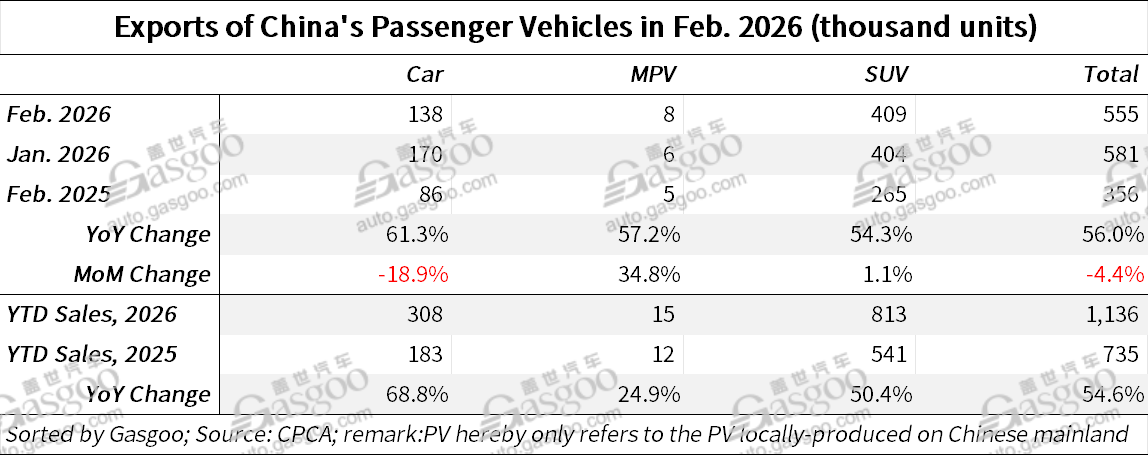

Passenger vehicle exports—including fully built vehicles and CKD shipments—reached 555,000 units in February, marking a 56% year-on-year increase, although the figure slipped 4.4% compared with January.

NEVs accounted for 48.5% of total exports during the month, representing a rise of 15 percentage points from a year earlier and highlighting the growing role of electrified models in China's overseas expansion. Domestic Chinese brands dominated outbound shipments, exporting 478,000 vehicles, up 52% year-on-year. Meanwhile, joint-venture and luxury brands together exported around 77,000 units, registering a faster growth rate of 85%.

Passenger vehicle production totaled 1.373 million units in February, reflecting a year-on-year decline of 21% and a 31.5% drop from the previous month, largely influenced by seasonal factors and softer demand. Output declined across all major brand categories. Premium vehicle production fell 9% from a year earlier and 40% from January, while joint-venture brand production decreased 22% year-on-year and 32% month-on-month. Domestic Chinese brands recorded a similar trend, with output down 22% year-on-year and 30% from the previous month.

Retail sales of new energy passenger vehicles reached 464,000 units in February, representing a 32% decline from a year earlier. For the January–February period, NEV retail sales totaled 1.06 million units, down 25.7% year-on-year.

Despite the drop in volume, NEVs continued to account for a significant share of the market. NEVs made up 44.9% of domestic passenger car retail sales in February, although this was four percentage points lower than the level recorded a year earlier.

Wholesale shipments of new energy passenger vehicles reached 723,000 units in February, down 13.1% from the same period last year. Cumulative wholesale volume for the first two months of 2026 totaled 1.589 million units, representing a 7.9% decline year-on-year.

Even with the contraction, the penetration rate of NEVs in manufacturers' wholesale volume rose slightly to 47.6%, about one percentage point higher than a year earlier. The adoption rate varied significantly by brand category. Domestic Chinese brands recorded the highest electrification level, with NEVs accounting for 58.9% of their shipments. Premium brands posted a penetration rate of 48.2%, while mainstream joint-venture brands remained far behind, with NEVs making up only 4.6% of their wholesale volumes.

Exports of new energy passenger vehicles continued to expand rapidly. Automakers shipped about 269,000 NEVs overseas in February, a year-on-year increase of 124.7%, though the figure was 7% lower than January. For the first two months of the year, NEV exports reached 559,000 units, more than doubling from the same period in 2025 with growth of 114.7%.

By comparison, exports of conventional internal combustion engine passenger vehicles totaled around 290,000 units in February, posting a more modest year-on-year increase of 21%, underscoring the accelerating shift toward electrified models in China's export mix.